Bank of America 2012 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 89

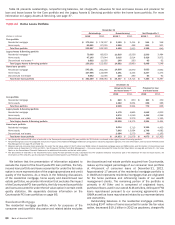

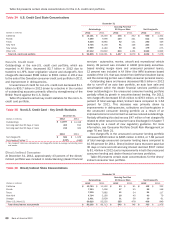

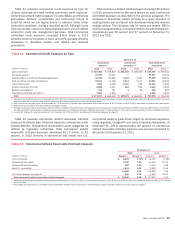

Other Consumer

At December 31, 2012, approximately 87 percent of the $1.6

billion other consumer portfolio was associated with certain

consumer finance businesses that we previously exited and non-

U.S. consumer loan portfolios that are included in All Other. The

remainder is primarily deposit overdrafts included in CBB.

Consumer Loans Accounted for Under the Fair Value

Option

Outstanding consumer loans accounted for under the fair value

option were $1.0 billion at December 31, 2012 and included $858

million of discontinued real estate loans and $147 million of

residential mortgage loans in consolidated variable interest

entities (VIEs). During 2012, we recorded gains of $57 million

resulting from changes in the fair value of the loan portfolio. These

were offset by losses recorded on the related long-term debt.

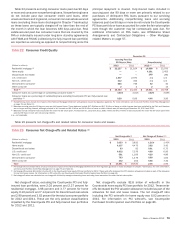

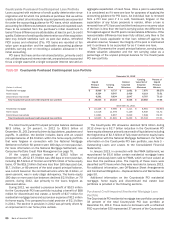

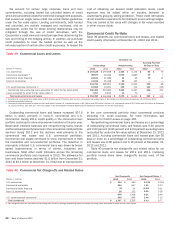

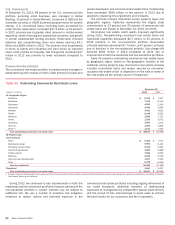

Nonperforming Consumer Loans and Foreclosed

Properties Activity

Table 37 presents nonperforming consumer loans and foreclosed

properties activity during 2012 and 2011. Nonperforming LHFS

are excluded from nonperforming loans as they are recorded at

either fair value or the lower of cost or fair value. Nonperforming

loans do not include past due consumer credit card loans, other

unsecured loans and in general, consumer non-real estate-secured

loans (excluding those loans discharged in Chapter 7 bankruptcy),

as these loans are typically charged off no later than the end of

the month in which the loan becomes 180 days past due. The

fully-insured loan portfolio is not reported as nonperforming as

principal repayment is insured. Additionally, nonperforming loans

do not include the Countrywide PCI loan portfolio or loans

accounted for under the fair value option. For further information

on nonperforming loans, see Note 1 – Summary of Significant

Accounting Principles to the Consolidated Financial Statements.

Nonperforming loans increased $663 million in 2012 to $19.4

billion. During 2012, we reclassified to nonperforming $1.9 billion

of junior-lien loans less than 90 days past due that have a senior-

lien loan that is 90 days or more past due and $1.2 billion of loans

less than 60 days past due that were discharged in Chapter 7

bankruptcy upon implementation of new regulatory guidance.

These additions to nonperforming loans were partially offset by

$435 million of nonperforming loans forgiven in connection with

the National Mortgage Settlement. Excluding the impact of these

items, nonperforming loans declined in 2012 as outflows outpaced

new inflows which continued to improve due to favorable

delinquency trends. For more information on the impacts related

to the National Mortgage Settlement and guidance issued by

regulatory agencies, see Consumer Portfolio Credit Risk

Management on page 76 and Table 21.

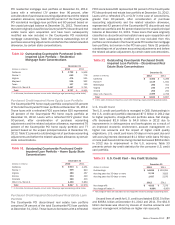

The outstanding balance of a real estate-secured loan that is

in excess of the estimated property value, after reducing the

estimated property value for estimated costs to sell, is charged

off no later than the end of the month in which the loan becomes

180 days past due unless repayment of the loan is fully insured.

At December 31, 2012, $10.7 billion, or 54 percent, of

nonperforming consumer real estate loans and foreclosed

properties had been written down to their estimated property value

less estimated costs to sell, including $10.1 billion of

nonperforming loans 180 days or more past due and $650 million

of foreclosed properties.

Foreclosed properties decreased $1.3 billion in 2012 as

liquidations outpaced additions. PCI loans are excluded from

nonperforming loans as these loans were written down to fair value

at the acquisition date; however, once the underlying real estate

is acquired by the Corporation upon foreclosure of the delinquent

PCI loan, it is included in foreclosed properties. Countrywide PCI

related foreclosed properties decreased $322 million in 2012.

Not included in foreclosed properties at December 31, 2012 was

$2.5 billion of real estate that was acquired upon foreclosure of

delinquent FHA-insured loans. We hold this real estate on our

balance sheet until we convey these properties to the FHA. We

exclude these amounts from our nonperforming loans and

foreclosed properties activity as we will be reimbursed once the

property is conveyed to the FHA for principal and, up to certain

limits, costs incurred during the foreclosure process and interest

incurred during the holding period. For additional information on

the review of our foreclosure processes, see Off-Balance Sheet

Arrangements and Contractual Obligations – Other Mortgage-

related Matters on page 57.