Bank of America 2012 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

40 Bank of America 2012

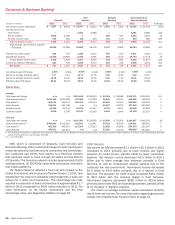

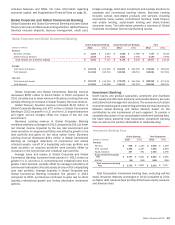

The table below summarizes the components of mortgage

banking income (loss).

Mortgage Banking Income (Loss)

(Dollars in millions) 2012 2011

Production income (loss):

Core production revenue $ 3,730 $ 2,797

Representations and warranties provision (3,939) (15,591)

Total production loss (209) (12,794)

Servicing income:

Servicing fees 4,734 6,035

Impact of customer payments (1) (1,484) (2,621)

Fair value changes of MSRs, net of risk management

activities used to hedge certain market risks (2) 1,845 655

Other servicing-related revenue 645 532

Total net servicing income 5,740 4,601

Total CRES mortgage banking income (loss) 5,531 (8,193)

Eliminations (3) (781) (637)

Total consolidated mortgage banking income (loss) $ 4,750 $ (8,830)

(1) Represents the change in the market value of the MSR asset due to the impact of customer

payments received during the year.

(2) Includes gains (losses) on sales of MSRs.

(3) Includes the effect of transfers of mortgage loans from CRES to the ALM portfolio in All Other.

CRES first mortgage loan originations declined $80.8 billion,

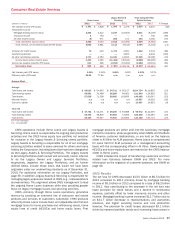

or 58 percent, primarily as a result of our exit from the

correspondent lending channel in 2011. CRES retail first mortgage

loan originations were $58.5 billion in 2012 compared to $67.8

billion in 2011, excluding correspondent lending, reflecting a drop

in estimated retail market share as the overall market for

mortgages increased. Our decline in market share was primarily

due to our decision to price loan products in order to manage our

fulfillment capacity. Core production revenue increased $933

million to $3.7 billion as the impact of our exit from the

correspondent lending channel and the decline in retail

originations were more than offset by higher retail margins. On an

industry-wide basis margins increased as historically low mortgage

rates drove strong consumer demand for refinance transactions

at a time when most lenders had capacity constraints which,

combined with our pricing strategy, contributed to higher retail

margins. In addition, a higher proportion of refinance transactions,

particularly Home Affordable Refinance Programs (HARP),

contributed to higher margins. During 2012, 84 percent of our first

mortgage production volume was for refinance originations and

16 percent was for purchase originations compared to 60 percent

and 40 percent in 2011.

The representations and warranties provision decreased $11.7

billion to $3.9 billion as described earlier in this section.

Net servicing income increased $1.1 billion to $5.7 billion

primarily due to $1.2 billion in improved MSR results, net of

hedges, and $1.1 billion in reduced impact of customer payments

driven by a lower MSR asset, partially offset by a $1.3 billion

decrease in servicing fees primarily due to a reduction in the size

of the servicing portfolio. For additional information, see Note 24

– Mortgage Servicing Rights to the Consolidated Financial

Statements.

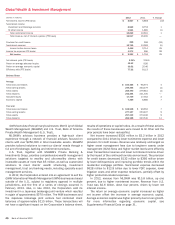

Key Statistics

(Dollars in millions, except as noted) 2012 2011

Loan production

Total Corporation (1):

First mortgage $ 75,074 $ 151,756

First mortgage (excluding

correspondent lending) 75,074 80,300

Home equity 3,585 4,388

CRES:

First mortgage $ 58,518 $ 139,273

First mortgage (excluding

correspondent lending) 58,518 67,817

Home equity 2,832 3,694

Year end

Mortgage serviced portfolio (in billions) (2, 3) $ 1,332 $ 1,763

Mortgage loans serviced for investors

(in billions) 1,045 1,379

Mortgage servicing rights:

Balance 5,716 7,378

Capitalized mortgage servicing rights

(% of loans serviced for investors) 55 bps 54 bps

(1) In addition to loan production in CRES, the remaining first mortgage and home equity loan

production is primarily in GWIM.

(2) Servicing of residential mortgage loans, HELOCs, home equity loans and discontinued real

estate mortgage loans.

(3) The mortgage serviced portfolio at December 31, 2010 was $2,057 billion.

Retail first mortgage loan originations for the total Corporation

were $75.1 billion for 2012 compared to $80.3 billion for 2011,

excluding correspondent lending. The decrease was primarily

driven by our decision to price loan products in order to manage

our fulfillment capacity.

Home equity production was $3.6 billion for 2012 compared

to $4.4 billion for 2011 primarily due to our decision to exit the

reverse mortgage business.