Bank of America 2012 Annual Report Download - page 267

Download and view the complete annual report

Please find page 267 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 265

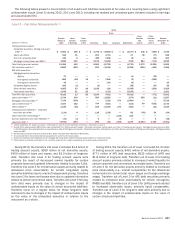

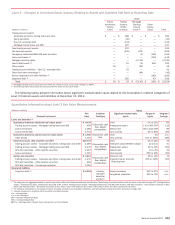

and interest rate correlations are measured between curves and

across the various tenors on the same curve, the range of potential

values can include both negative and positive values. For the

correlation (IR/IR) range, the exposure represents the valuation

of interest rate correlations on less liquid pairings and is

concentrated at the upper end of the range. For the correlation

(FX/IR) range, the exposure is the sensitivity to a broad mix of

interest rate and foreign exchange correlations and is distributed

evenly throughout the range. For long-dated inflation rates and

volatilities as well as long-dated volatilities (FX), the inputs are

concentrated in the middle of the range.

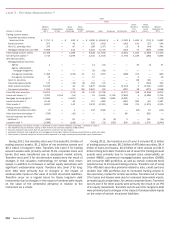

Sensitivity of Fair Value Measurements to Changes in

Unobservable Inputs

Loans and Securities

For instruments backed by residential real estate assets,

commercial real estate assets, and commercial loans, debt

securities and other, a significant increase in market yields, default

rates or loss severities would result in a significantly lower fair

value for long positions. Short positions would be impacted in a

directionally opposite way. The impact of changes in prepayment

speeds would have differing impacts depending on the seniority

of the instrument and, in the case of CLOs, whether prepayments

can be reinvested.

For closed-end ARS, a significant increase in discount rates

would result in a significantly lower fair value. For student loan and

municipal ARS, a significant increase in projected tender price/

refinancing levels would result in a significantly higher fair value.

Structured Liabilities and Derivatives

For credit derivatives, a significant increase in market yield,

including spreads to indices, upfront points (i.e., a single upfront

payment made by a protection buyer at inception), credit spreads,

default rates or loss severities would result in a significantly lower

fair value for protection sellers and higher fair value for protection

buyers. The impact of changes in prepayment speeds would have

differing impacts depending on the seniority of the instrument and,

in the case of CLOs, whether prepayments can be reinvested.

Structured credit derivatives, which include tranched portfolio

CDS and derivatives with derivative product company (DPC) and

monoline counterparties, are impacted by credit correlation,

including default and wrong-way correlation. Default correlation is

a parameter that describes the degree of dependence among

credit default rates within a credit portfolio that underlies a credit

derivative instrument. The sensitivity of this input on the fair value

varies depending on the level of subordination of the tranche. For

senior tranches that are net purchases of protection, a significant

increase in default correlation would result in a significantly higher

fair value. Net short protection positions would be impacted in a

directionally opposite way. Wrong-way correlation is a parameter

that describes the probability that as exposure to a counterparty

increases, the credit quality of the counterparty decreases. A

significantly higher degree of wrong-way correlation between a DPC

counterparty and underlying derivative exposure would result in a

significantly lower fair value.

For equity derivatives, equity-linked long-term debt (structured

liabilities) and interest rate derivatives, a significant change in

long-dated rates and volatilities and correlation inputs (e.g., the

degree of correlation between an equity security and an index,

between two different interest rates, or between interest rates and

foreign exchange rates) would result in a significant impact to the

fair value; however, the magnitude and direction of the impact

depends on whether the Corporation is long or short the exposure.

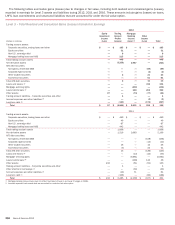

Nonrecurring Fair Value

The Corporation holds certain assets that are measured at fair

value, but only in certain situations (for example, impairment) and

these measurements are referred to herein as nonrecurring. These

assets primarily include LHFS, certain loans and leases, and

foreclosed properties. The amounts below represent only balances

measured at fair value during 2012, 2011 and 2010, and still held

as of the reporting date.

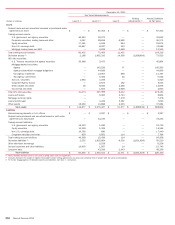

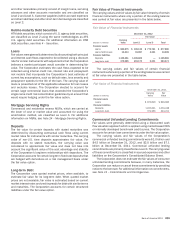

Assets Measured at Fair Value on a Nonrecurring Basis

December 31

2012 2011

(Dollars in millions) Level 2 Level 3 Level 2 Level 3

Assets

Loans held-for-sale $ 5,692 $ 1,136 $ 2,662 $ 1,008

Loans and leases 21 9,184 9 10,629

Foreclosed properties (1) 33 1,918 — 2,531

Other assets 36 12 44 885

Gains (Losses)

(Dollars in millions) 2012 2011 2010

Assets

Loans held-for-sale $ (8) $ (181) $ 174

Loans and leases (2) (3,116) (4,813) (6,074)

Foreclosed properties (188) (333) (240)

Other assets (16) — (50)

(1) Amounts are included in other assets on the Corporation’s Consolidated Balance Sheet and

represent fair value and related losses on foreclosed properties that were written down

subsequent to their initial classification as foreclosed properties.

(2) Losses represent charge-offs on real estate-secured loans.