Bank of America 2012 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

92 Bank of America 2012

We account for certain large corporate loans and loan

commitments, including issued but unfunded letters of credit

which are considered utilized for credit risk management purposes,

that exceed our single name credit risk concentration guidelines

under the fair value option. Lending commitments, both funded

and unfunded, are actively managed and monitored, and as

appropriate, credit risk for these lending relationships may be

mitigated through the use of credit derivatives, with the

Corporation’s credit view and market perspectives determining the

size and timing of the hedging activity. In addition, we purchase

credit protection to cover the funded portion as well as the

unfunded portion of certain other credit exposures. To lessen the

cost of obtaining our desired credit protection levels, credit

exposure may be added within an industry, borrower or

counterparty group by selling protection. These credit derivatives

do not meet the requirements for treatment as accounting hedges.

They are carried at fair value with changes in fair value recorded

in other income (loss).

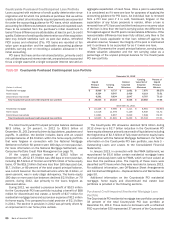

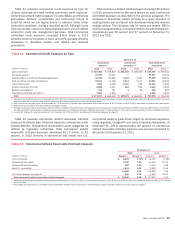

Commercial Credit Portfolio

Table 39 presents our commercial loans and leases, and related

credit quality information at December 31, 2012 and 2011.

Table 39 Commercial Loans and Leases

December 31

Outstandings Nonperforming

Accruing Past Due

90 Days or More

(Dollars in millions) 2012 2011 2012 2011 2012 2011

U.S. commercial $ 197,126 $179,948 $ 1,484 $ 2,174 $65 $ 75

Commercial real estate (1) 38,637 39,596 1,513 3,880 29 7

Commercial lease financing 23,843 21,989 44 26 15 14

Non-U.S. commercial 74,184 55,418 68 143 ——

333,790 296,951 3,109 6,223 109 96

U.S. small business commercial (2) 12,593 13,251 115 114 120 216

Commercial loans excluding loans accounted for under the fair value option 346,383 310,202 3,224 6,337 229 312

Loans accounted for under the fair value option (3) 7,997 6,614 11 73 ——

Total commercial loans and leases $ 354,380 $316,816 $ 3,235 $ 6,410 $229 $ 312

(1) Includes U.S. commercial real estate loans of $37.2 billion and $37.8 billion and non-U.S. commercial real estate loans of $1.5 billion and $1.8 billion at December 31, 2012 and 2011.

(2) Includes card-related products.

(3) Commercial loans accounted for under the fair value option include U.S. commercial loans of $2.3 billion and $2.2 billion, and non-U.S. commercial loans of $5.7 billion and $4.4 billion at December

31, 2012 and 2011. See Note 22 – Fair Value Option to the Consolidated Financial Statements for additional information on the fair value option.

Outstanding commercial loans and leases increased $37.6

billion in 2012, primarily in non-U.S. commercial and U.S.

commercial. During 2012, credit quality in the commercial loan

portfolio continued to show improvement relative to the prior year.

Reservable criticized balances and nonperforming loans, leases

and foreclosed property balances in the commercial credit portfolio

declined during 2012 and the declines were primarily in the

commercial real estate and U.S. commercial portfolios.

Commercial real estate continued to show improvement in both

the residential and non-residential portfolios. The reduction in

reservable criticized U.S. commercial loans was driven by broad-

based improvements in terms of clients, industries and

businesses. Most other credit indicators across the remaining

commercial portfolios also improved in 2012. The allowance for

loan and lease losses declined $1.0 billion from December 31,

2011 to $3.1 billion at December 31, 2012 due to improvements

in the core commercial portfolio (total commercial products

excluding U.S. small business). For more information, see

Allowance for Credit Losses on page 105.

Nonperforming commercial loans and leases as a percentage

of outstanding commercial loans and leases was 0.91 percent

and 2.02 percent (0.93 percent and 2.04 percent excluding loans

accounted for under the fair value option) at December 31, 2012

and 2011. Accruing commercial loans and leases past due 90

days or more as a percentage of outstanding commercial loans

and leases was 0.06 percent and 0.10 percent at December 31,

2012 and 2011.

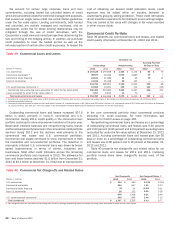

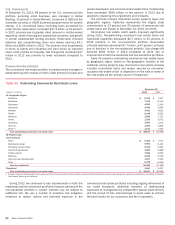

Table 40 presents net charge-offs and related ratios for our

commercial loans and leases for 2012 and 2011. Improving

portfolio trends drove lower charge-offs across most of the

portfolio.

Table 40 Commercial Net Charge-offs and Related Ratios

Net Charge-offs Net Charge-off Ratios (1)

(Dollars in millions) 2012 2011 2012 2011

U.S. commercial $242 $ 195 0.13%0.11%

Commercial real estate 384 947 1.01 2.13

Commercial lease financing (6) 24 (0.03) 0.11

Non-U.S. commercial 28 152 0.05 0.36

648 1,318 0.21 0.46

U.S. small business commercial 699 995 5.46 7.12

Total commercial $ 1,347 $ 2,313 0.43 0.77

(1) Net charge-off ratios are calculated as net charge-offs divided by average outstanding loans and leases excluding loans accounted for under the fair value option.