Bank of America 2012 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

70 Bank of America 2012

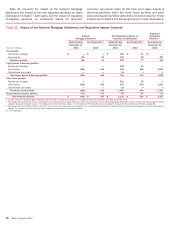

Bank of America, N.A. and FIA Card Services, N.A. Regulatory Capital

Table 16 presents regulatory capital information for BANA and FIA at December 31, 2012 and 2011.

Table 16 Bank of America, N.A. and FIA Card Services, N.A. Regulatory Capital

December 31

2012 2011

(Dollars in millions) Ratio Amount Ratio Amount

Tier 1

Bank of America, N.A. 12.44% $ 118,431 11.74% $ 119,881

FIA Card Services, N.A. 17.34 22,061 17.63 24,660

Total

Bank of America, N.A. 14.76 140,434 15.17 154,885

FIA Card Services, N.A. 18.64 23,707 19.01 26,594

Tier 1 leverage

Bank of America, N.A. 8.59 118,431 8.65 119,881

FIA Card Services, N.A. 13.67 22,061 14.22 24,660

BANA’s Tier 1 capital ratio increased 70 bps to 12.44 percent

and the Total capital ratio decreased 41 bps to 14.76 percent at

December 31, 2012 compared to December 31, 2011. The Tier

1 leverage ratio decreased six bps to 8.59 percent at

December 31, 2012 compared to December 31, 2011. The

increase in the Tier 1 capital ratio was driven by earnings eligible

to be included in capital of $12.3 billion and a decrease in risk-

weighted assets of $69.1 billion compared to the prior year, largely

offset by dividends paid to the Corporation of $14.1 billion during

2012. The decrease in the Total capital ratio was driven by a $12.0

billion decrease in qualifying subordinated debt, partially offset by

the net impact of earnings eligible to be included in capital and a

decrease in risk-weighted assets. The decrease in the Tier 1

leverage ratio was driven by a decrease in Tier 1 capital, partially

offset by a decrease in adjusted quarterly average total assets.

FIA’s Tier 1 capital ratio decreased 29 bps to 17.34 percent

and the Total capital ratio decreased 37 bps to 18.64 percent at

December 31, 2012 compared to December 31, 2011. The Tier

1 leverage ratio decreased 55 bps to 13.67 percent at

December 31, 2012 compared to December 31, 2011. The

decrease in the Tier 1 capital and Total capital ratios was driven

by returns of capital of $6.6 billion to the Corporation during 2012,

partially offset by earnings eligible to be included in capital of $4.2

billion and a decrease in risk-weighted assets primarily due to a

decrease in loans. The decrease in the Tier 1 leverage ratio was

driven by the decrease in Tier 1 capital, partially offset by a

decrease in adjusted quarterly average total assets of $12.0

billion.

Broker/Dealer Regulatory Capital

The Corporation’s principal U.S. broker/dealer subsidiaries are

Merrill Lynch, Pierce, Fenner & Smith (MLPF&S) and Merrill Lynch

Professional Clearing Corp (MLPCC). MLPCC is a fully-guaranteed

subsidiary of MLPF&S and provides clearing and settlement

services. Both entities are subject to the net capital requirements

of SEC Rule 15c3-1. Both entities are also registered as futures

commission merchants and are subject to the CFTC Regulation

1.17.

MLPF&S has elected to compute the minimum capital

requirement in accordance with the Alternative Net Capital

Requirement as permitted by SEC Rule 15c3-1. At December 31,

2012, MLPF&S’s regulatory net capital as defined by Rule 15c3-1

was $10.3 billion and exceeded the minimum requirement of $683

million by $9.7 billion. MLPCC’s net capital of $2.1 billion exceeded

the minimum requirement of $236 million by $1.8 billion.

In accordance with the Alternative Net Capital Requirements,

MLPF&S is required to maintain tentative net capital in excess of

$1.0 billion, net capital in excess of $500 million and notify the

SEC in the event its tentative net capital is less than $5.0 billion.

At December 31, 2012, MLPF&S had tentative net capital and net

capital in excess of the minimum and notification requirements.

Economic Capital

Our economic capital measurement process provides a risk-based

measurement of the capital required for unexpected credit, market

and operational losses over a one-year time horizon at a

99.97 percent confidence level. Economic capital is allocated to

each business unit and is used for capital adequacy, performance

measurement and risk management purposes. The strategic

planning process utilizes economic capital with the goal of

allocating risk appropriately and measuring returns consistently

across all businesses and activities. Economic capital allocation

plans are incorporated into the Corporation’s financial plan which

is approved by the Board on an annual basis.

Credit Risk Capital

Economic capital for credit risk captures two types of risks: default

risk, which represents the loss of principal due to outright default

or the borrower’s inability to repay an obligation in full, and

migration risk, which represents potential loss in market value due

to credit deterioration over a one-year capital time horizon. Credit

risk is assessed and modeled for all on- and off-balance sheet

credit exposures within sub-categories for commercial, retail,

counterparty and investment securities. The economic capital

methodology captures dimensions such as concentration and

country risk and originated securitizations. The economic capital

methodology is based on the probability of default, loss given

default (LGD), exposure at default (EAD) and maturity for each

credit exposure, and the portfolio correlations across exposures.

See page 75 for more information on Credit Risk Management.