Bank of America 2012 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

106 Bank of America 2012

During 2012, the factors that impacted the allowance for loan

and lease losses included significant overall improvements in the

credit quality of the portfolios driven by improvements in the U.S.

economy and labor markets, proactive credit risk management

initiatives and the impact of recent higher credit quality

originations. Additionally, the resolution of uncertainties through

current recognition of net charge-offs, specifically in the home

loans portfolios, has impacted the amount of reserve needed in

that portfolio. Evidencing the improvements in the U.S. economy

and labor markets are modest growth in consumer spending,

improvements in unemployment levels, a decrease in the absolute

level and our share of national consumer bankruptcy filings, a rise

in both residential building activity and overall home prices. In

addition to these improvements, paydowns, charge-offs and

returns to performing status and upgrades out of criticized

continued to outpace new nonaccrual consumer loans and

reservable criticized commercial loans, but such loans remained

elevated relative to levels experienced prior to the financial crisis.

We monitor differences between estimated and actual incurred

loan and lease losses. This monitoring process includes periodic

assessments by senior management of loan and lease portfolios

and the models used to estimate incurred losses in those

portfolios.

Additions to, or reductions of, the allowance for loan and lease

losses generally are recorded through charges or credits to the

provision for credit losses. Credit exposures deemed to be

uncollectible are charged against the allowance for loan and lease

losses. Recoveries of previously charged off amounts are credited

to the allowance for loan and lease losses.

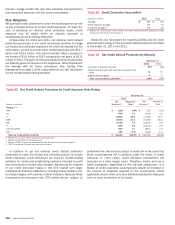

The allowance for loan and lease losses for the consumer

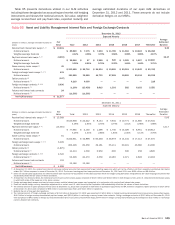

portfolio, as presented in Table 61, was $21.1 billion at

December 31, 2012, a decrease of $8.6 billion from

December 31, 2011. The decrease in the home equity and

residential mortgage allowance was primarily driven by improved

delinquencies and home prices as evidenced by improving LTV

statistics as presented in Tables 25 and 27. In addition, the home

equity allowance declined due to reduced exposures to current

junior-lien loans that we estimate had a first-lien loan that was 90

days or more past due. Also, the home equity allowance related

to the PCI portfolio declined $2.7 billion primarily due to the

forgiveness of fully reserved home equity loans in connection with

the National Mortgage Settlement.

The decrease in the allowance related to the U.S. credit card

and unsecured consumer lending portfolios in CBB was primarily

due to improvement in delinquencies and bankruptcies. For

example, in the U.S. credit card portfolio, accruing loans 30 days

or more past due decreased to $2.7 billion at December 31, 2012

from $3.8 billion (to 2.90 percent from 3.74 percent of outstanding

U.S. credit card loans) at December 31, 2011, and accruing loans

90 days or more past due decreased to $1.4 billion at

December 31, 2012 from $2.1 billion (to 1.52 percent from 2.02

percent of outstanding U.S. credit card loans) over the same

period. See Tables 22, 23, 25, 27, 33 and 35 for additional details

on key consumer credit statistics.

The allowance for loan and lease losses for the commercial

portfolio as presented in Table 61 was $3.1 billion at

December 31, 2012, a decrease of $1.0 billion from

December 31, 2011. The decrease was driven by continued

improvement in the credit quality of the core commercial portfolio.

For example, the commercial utilized reservable criticized exposure

decreased to $15.9 billion at December 31, 2012 from $27.2

billion (to 4.10 percent from 7.41 percent of total commercial

utilized reservable exposure) at December 31, 2011. Similarly,

nonperforming commercial loans declined to $3.2 billion at

December 31, 2012 from $6.3 billion (to 0.93 percent from 2.04

percent of outstanding commercial loans) at December 31, 2011.

See Tables 39, 40 and 42 for additional details on key commercial

credit statistics.

The allowance for loan and lease losses as a percentage of

total loans and leases outstanding was 2.69 percent at

December 31, 2012 compared to 3.68 percent at December 31,

2011. The decrease in the ratio was largely due to improved credit

quality driven by improved economic conditions and the home

equity PCI loans that were forgiven which led to the reduction in

the allowance for credit losses discussed above. The December

31, 2012 and 2011 ratios above include the PCI loan portfolio.

Excluding the PCI loan portfolio, the allowance for loan and lease

losses as a percentage of total loans and leases outstanding was

2.14 percent at December 31, 2012 compared to 2.86 percent

at December 31, 2011.