Bank of America 2012 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 79

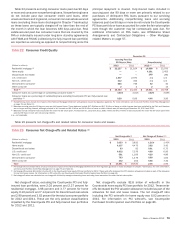

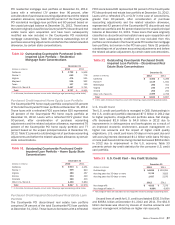

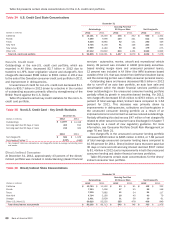

Table 22 presents accruing consumer loans past due 90 days

or more and consumer nonperforming loans. Nonperforming loans

do not include past due consumer credit card loans, other

unsecured loans and in general, consumer non-real estate-secured

loans (excluding those loans discharged in Chapter 7 bankruptcy)

as these loans are typically charged off no later than the end of

the month in which the loan becomes 180 days past due. Real

estate-secured past due consumer loans that are insured by the

FHA or individually insured under long-term stand-by agreements

with FNMA and FHLMC (collectively, the fully-insured loan portfolio)

are reported as accruing as opposed to nonperforming since the

principal repayment is insured. Fully-insured loans included in

accruing past due 90 days or more are primarily related to our

purchases of delinquent FHA loans pursuant to our servicing

agreements. Additionally, nonperforming loans and accruing

balances past due 90 days or more do not include the Countrywide

PCI loan portfolio or loans accounted for under the fair value option

even though the customer may be contractually past due. For

additional information on FHA loans, see Off-Balance Sheet

Arrangements and Contractual Obligations – Other Mortgage-

related Matters on page 57.

Table 22 Consumer Credit Quality

December 31

Accruing Past Due

90 Days or More Nonperforming

(Dollars in millions) 2012 2011 2012 (1) 2011

Residential mortgage (2) $ 22,157 $ 21,164 $14,808 $ 15,970

Home equity ——4,281 2,453

Discontinued real estate ——248 290

U.S. credit card 1,437 2,070 n/a n/a

Non-U.S. credit card 212 342 n/a n/a

Direct/Indirect consumer 545 746 92 40

Other consumer 22215

Total (3) $ 24,353 $ 24,324 $19,431 $ 18,768

Consumer loans as a percentage of outstanding consumer loans (3) 4.41%4.01% 3.52%3.09%

Consumer loans as a percentage of outstanding loans excluding Countrywide PCI and fully-insured loan

portfolios (3) 0.50 0.66 4.46 3.90

(1) Nonperforming loans include the impacts of the National Mortgage Settlement and guidance issued by regulatory agencies. For more information, see Consumer Portfolio Credit Risk Management

on page 76 and Table 21.

(2) Balances accruing past due 90 days or more are fully-insured loans. These balances include $17.8 billion and $17.0 billion of loans on which interest has been curtailed by the FHA, and therefore

are no longer accruing interest, although principal is still insured and $4.4 billion and $4.2 billion of loans on which interest was still accruing at December 31, 2012 and 2011.

(3) Balances exclude consumer loans accounted for under the fair value option. At December 31, 2012 and 2011, $391 million and $713 million of loans accounted for under the fair value option were

past due 90 days or more and not accruing interest.

n/a = not applicable

Table 23 presents net charge-offs and related ratios for consumer loans and leases.

Table 23 Consumer Net Charge-offs and Related Ratios (1)

Net Charge-offs (2) Net Charge-off Ratios (2, 3)

(Dollars in millions) 2012 2011 2012 2011

Residential mortgage $ 3,053 $ 3,832 1.21%1.45%

Home equity 4,237 4,473 3.62 3.42

Discontinued real estate 63 92 0.61 0.75

U.S. credit card 4,632 7,276 4.88 6.90

Non-U.S. credit card 581 1,169 4.29 4.86

Direct/Indirect consumer 763 1,476 0.90 1.64

Other consumer 232 202 9.85 7.32

Total $ 13,561 $ 18,520 2.36 2.94

(1) Net charge-offs and related ratios for 2012 include the impacts of the National Mortgage Settlement and new regulatory guidance on loans discharged in Chapter 7 bankruptcy. For more information,

see Consumer Portfolio Credit Risk Management on page 76 and Table 21.

(2) Net charge-offs exclude $2.8 billion of write-offs in the Countrywide home equity PCI loan portfolio for 2012. These write-offs decreased the PCI valuation allowance included as part of the allowance

for loan and lease losses. For information on PCI write-offs, see Countrywide Purchased Credit-impaired Loan Portfolio on page 86.

(3) Net charge-off ratios are calculated as net charge-offs divided by average outstanding loans excluding loans accounted for under the fair value option.

Net charge-off ratios, excluding the Countrywide PCI and fully-

insured loan portfolios, were 2.02 percent and 2.27 percent for

residential mortgage, 3.98 percent and 3.77 percent for home

equity, 6.10 percent and 7.14 percent for discontinued real estate

and 2.99 percent and 3.62 percent for the total consumer portfolio

for 2012 and 2011. These are the only product classifications

impacted by the Countrywide PCI and fully-insured loan portfolios

for 2012 and 2011.

Net charge-offs exclude $2.8 billion of write-offs in the

Countrywide home equity PCI loan portfolio for 2012. These write-

offs decreased the PCI valuation allowance included as part of the

allowance for loan and lease losses. The net charge-off ratio

including the PCI write-offs for home equity was 6.02 percent in

2012. For information on PCI write-offs, see Countrywide

Purchased Credit-impaired Loan Portfolio on page 86.