Bank of America 2012 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

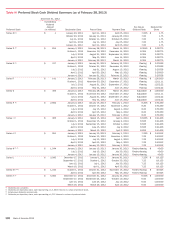

124 Bank of America 2012

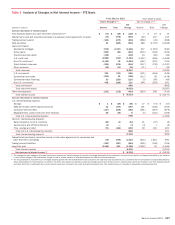

2011 Compared to 2010

The following discussion and analysis provides a comparison of

our results of operations for 2011 and 2010. This discussion

should be read in conjunction with the Consolidated Financial

Statements and related Notes. Tables 7 and 8 contain financial

data to supplement this discussion.

Overview

Net Income (Loss)

Net income was $1.4 billion in 2011 compared to a net loss of

$2.2 billion in 2010. Including preferred stock dividends, the net

income applicable to common shareholders was $85 million, or

$0.01 per diluted share. Those results compared to a net loss

applicable to common shareholders of $3.6 billion, or $0.37 per

diluted share for 2010.

Net Interest Income

Net interest income on a FTE basis was $45.6 billion for 2011, a

decrease of $7.1 billion compared to 2010. The decline was

primarily due to lower consumer loan balances and yields and

decreased investment security yields, including the acceleration

of purchase premium amortization from an increase in modeled

prepayment expectations, and increased hedge ineffectiveness.

Lower trading-related net interest income also negatively impacted

2011 results. These decreases were partially offset by ongoing

reductions in our debt footprint and lower interest rates paid on

deposits. The net interest yield on a FTE basis was 2.48 percent

for 2011, a decrease of 30 bps compared to 2010 as the yield

continued to be under pressure due to the aforementioned items

and the low rate environment.

Noninterest Income

Noninterest income was $48.8 billion in 2011, a decrease of $9.9

billion compared to 2010.

Card income decreased $924 million primarily due to the

implementation of new interchange fee rules under the Durbin

Amendment, which became effective on October 1, 2011 and

the Credit Card Accountability Responsibility and Disclosure Act

of 2009 (CARD Act) provisions that were implemented during

2010.

Service charges decreased $1.3 billion largely due to the impact

of overdraft policy changes in conjunction with Regulation E,

which became effective in the third quarter of 2010.

Equity investment income increased $2.1 billion. The results for

2011 included $6.5 billion of gains on the sale of CCB shares,

partially offset by $1.1 billion of impairment charges on our

merchant services joint venture. The prior year included $2.5

billion of net gains which included the sales of certain strategic

investments, $2.3 billion of gains in our GPI portfolio and $535

million of CCB dividends.

Trading account profits decreased $3.4 billion primarily due to

adverse market conditions and extreme volatility in the credit

markets compared to the prior year. Net DVA gains on derivatives

were $1.0 billion in 2011 compared to $262 million in 2010 as

a result of a widening of our credit spreads. Proprietary trading

revenue was $434 million for the six months ended June 30,

2011 compared to $1.4 billion for 2010 due to Global Markets

exiting its stand-alone proprietary trading business as of June

30, 2011.

Mortgage banking income decreased $11.6 billion primarily due

to an $8.8 billion increase in the representations and warranties

provision which was largely related to the BNY Mellon

Settlement. Also contributing to the decline was lower

production income due to a reduction in new loan origination

volumes partially offset by an increase in servicing income.

Other income increased $4.5 billion primarily due to positive

fair value adjustments of $3.3 billion related to widening of our

own credit spreads on structured liabilities compared to $18

million in 2010. In addition, 2011 included a $771 million gain

on the sale of Balboa as well as $1.2 billion of gains on the

exchange of certain trust preferred securities for common stock

and debt.

Provision for Credit Losses

The provision for credit losses was $13.4 billion for 2011, a

decrease of $15.0 billion compared to 2010. The provision for

credit losses was $7.4 billion lower than net charge-offs for 2011,

resulting in a reduction in the allowance for credit losses primarily

driven by lower delinquencies, improved collection rates and fewer

bankruptcy filings across the U.S. credit card and unsecured

consumer lending portfolios, and improvement in overall credit

quality in the commercial real estate portfolio partially offset by

additions to consumer PCI loan portfolio reserves. This compared

to a $5.9 billion reduction in the allowance for credit losses in

2010.

Net charge-offs totaled $20.8 billion, or 2.24 percent of

average loans and leases for 2011 compared to $34.3 billion, or

3.60 percent for 2010. The decrease in net charge-offs was

primarily driven by improvements in general economic conditions

that resulted in lower delinquencies, improved collection rates and

fewer bankruptcy filings across the U.S. credit card and unsecured

consumer lending portfolios, as well as lower losses in the home

equity portfolio primarily driven by fewer delinquent loans.

Noninterest Expense

Noninterest expense was $80.3 billion for 2011, a decrease of

$2.8 billion compared to 2010. Goodwill impairment charges were

$3.2 billion for 2011 compared to $12.4 billion in the prior year.

Personnel expense increased $1.8 billion for 2011 attributable to

personnel costs related to the continued build-out of certain

businesses, technology costs as well as increases in default-

related servicing. Additionally, professional fees increased $686

million related to consulting fees for regulatory initiatives as well

as higher legal expenses. Other general operating expenses

increased $4.9 billion largely as a result of a $3.0 billion increase

in litigation expense, primarily mortgage-related, and an increase

of $1.6 billion in mortgage-related assessments and waivers

costs. Merger and restructuring expenses decreased $1.2 billion

in 2011.

Income Tax Expense

The income tax benefit was $1.7 billion on the pre-tax loss of $230

million for 2011 compared to income tax expense of $915 million

on the pre-tax loss of $1.3 billion for 2010. These amounts are

before FTE adjustments. The income tax benefit for 2011 was

driven by recurring tax preference items, a $1.0 billion benefit from

the release of the remaining valuation allowance applicable to the

Merrill Lynch capital loss carryover deferred tax asset, and a

benefit of $823 million for planned realization of previously

unrecognized deferred tax assets related to the tax basis in certain