Bank of America 2012 Annual Report Download - page 188

Download and view the complete annual report

Please find page 188 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

186 Bank of America 2012

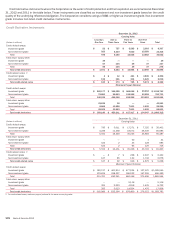

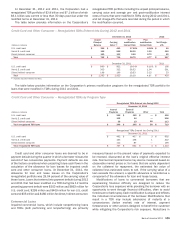

The Corporation mitigates a portion of its credit risk on the

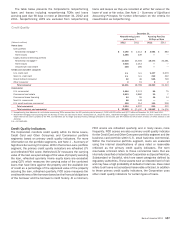

residential mortgage portfolio through the use of synthetic

securitization vehicles. These vehicles issue long-term notes to

investors, the proceeds of which are held as cash collateral. The

Corporation pays a premium to the vehicles to purchase mezzanine

loss protection on a portfolio of residential mortgage loans owned

by the Corporation. Cash held in the vehicles is used to reimburse

the Corporation in the event that losses on the mortgage portfolio

exceed 10 basis points (bps) of the original pool balance, up to

the remaining amount of purchased loss protection of $500 million

and $783 million at December 31, 2012 and 2011. The vehicles

from which the Corporation purchases credit protection are VIEs.

The Corporation does not have a variable interest in these vehicles,

and accordingly, these vehicles are not consolidated by the

Corporation. Amounts due from the vehicles are recorded in other

income (loss) when the Corporation recognizes a reimbursable

loss, as described above. Amounts are collected when

reimbursable losses are realized through the sale of the underlying

collateral. At December 31, 2012 and 2011, the Corporation had

a receivable of $305 million and $359 million from these vehicles

for reimbursement of losses, and principal of $17.6 billion and

$23.9 billion of residential mortgage loans was referenced under

these agreements. The Corporation records an allowance for credit

losses on these loans without regard to the existence of the

purchased loss protection as the protection does not represent a

guarantee of individual loans.

In addition, the Corporation has entered into long-term credit

protection agreements with FNMA and FHLMC on loans totaling

$24.3 billion and $24.4 billion at December 31, 2012 and 2011,

providing full protection on residential mortgage loans that become

severely delinquent. All of these loans are individually insured and

therefore the Corporation does not record an allowance for credit

losses related to these loans. For additional information, see Note

8 – Representations and Warranties Obligations and Corporate

Guarantees.

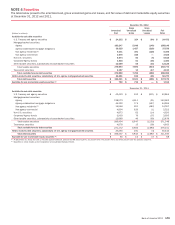

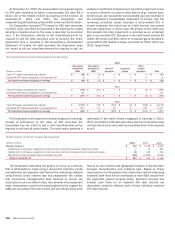

Nonperforming Loans and Leases

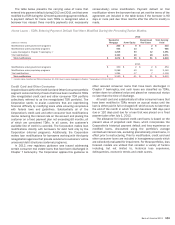

In 2012, the bank regulatory agencies jointly issued interagency

supervisory guidance on nonaccrual status for junior-lien

consumer real estate loans. In accordance with this regulatory

interagency guidance, the Corporation classifies junior-lien home

equity loans as nonperforming when the first-lien loan becomes

90 days past due even if the junior-lien loan is performing, and as

a result, an incremental $1.5 billion was included in nonperforming

loans at December 31, 2012. The regulatory interagency guidance

had no impact on the Corporation’s allowance for loan and lease

losses or provision for credit losses as the delinquency status of

the underlying first-lien loans was already considered in the

Corporation’s reserving process.

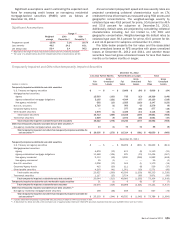

In 2012, new regulatory guidance was issued addressing

certain consumer real estate loans that have been discharged in

Chapter 7 bankruptcy. In accordance with this new guidance, the

Corporation classifies consumer real estate and other secured

consumer loans that have been discharged in Chapter 7

bankruptcy and not reaffirmed by the borrower as TDRs,

irrespective of payment history or delinquency status, even if the

repayment terms for the loan have not been otherwise modified.

The Corporation continues to have a lien on the underlying

collateral. Previously, such loans were classified as TDRs only if

there had been a change in contractual payment terms that

represented a concession to the borrower. The net impact upon

implementation to the consumer loan portfolio of adopting this

new regulatory guidance was $1.2 billion in net new nonperforming

loans, and $1.1 billion of such loans were included in

nonperforming loans at December 31, 2012. Of the $1.1 billion,

$1.0 billion, or 92 percent, were current on their contractual

payments. Of these contractually current nonperforming loans,

more than 70 percent were discharged in Chapter 7 bankruptcy

more than 12 months ago, and more than 40 percent were

discharged 24 months or more ago. As subsequent cash payments

are received, the interest component of the payments is generally

recorded as interest income on a cash basis and the principal

component is generally recorded as a reduction in the carrying

value of the loan.