Bank of America 2012 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

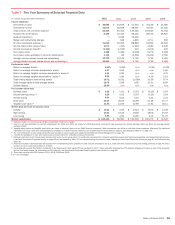

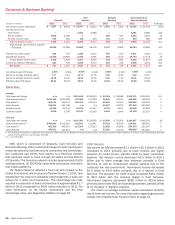

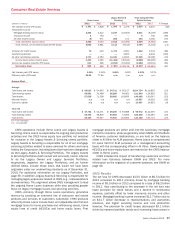

36 Bank of America 2012

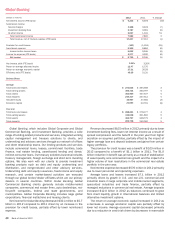

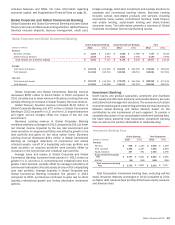

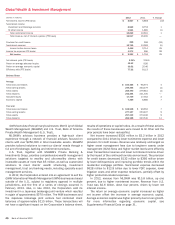

Business Banking

Business Banking provides a wide range of lending-related

products and services, integrated working capital management

and treasury solutions to clients through our network of offices

and client relationship teams along with various product partners.

Our clients include U.S.-based companies generally with annual

sales of $1 million to $50 million. Our lending products and

services include commercial loans, lines of credit and real estate

lending. Our capital management and treasury solutions include

treasury management, foreign exchange and short-term investing

options. Business Banking also includes the results of our

merchant services joint venture.

Net income for Business Banking decreased $76 million to

$343 million in 2012 primarily driven by lower revenue and an

increase in the provision for credit losses, largely offset by lower

noninterest expense. Net interest income decreased $183 million

to $1.2 billion driven by lower average loan balances. Noninterest

income decreased $172 million to $492 million primarily due to

the transfer of certain processing activities to our merchant

services joint venture in 2012. The provision for credit losses

increased $36 million to $281 million primarily driven by a slower

pace of improvement in credit quality than in the prior year.

Noninterest expense decreased $270 million to $888 million

driven by lower FDIC and merchant processing expenses.

Average loans decreased $3.1 billion to $23.8 billion in 2012

primarily driven by the net transfer of certain loans to other

businesses, higher prepayments and continued run-off of non-core

portfolios. Average deposits increased $2.2 billion to $42.8 billion

in 2012 due to the current client preference for liquidity and the

net transfer of certain deposits from other businesses.