Bank of America 2012 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 113

The $92 million decrease in average VaR during 2012 was

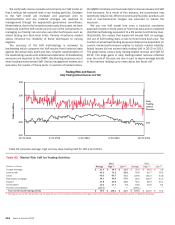

driven by reduced risk across most asset classes, with the largest

reductions coming from the credit, real estate/mortgage and

equities asset classes. In addition, volatile market data from 2008,

which was a material contribution to the 2011 average, was no

longer included in the three-year historical dataset for the 2012

average.

Counterparty credit risk is an adjustment to the mark-to-market

value of our derivative exposures to reflect the impact of the credit

quality of counterparties on our derivative assets. Since

counterparty credit exposure is not included in the VaR component

of the regulatory capital allocation, we do not include it in our

trading VaR, and it is therefore not included in the daily trading-

related revenue illustrated in our histogram or used for

backtesting.

Trading Portfolio Stress Testing

Because the very nature of a VaR model suggests results can

exceed our estimates and it is dependent on a limited lookback

window, we also stress test our portfolio. Stress testing estimates

the value change in our trading portfolio that may result from

abnormal market movements. Various scenarios, categorized as

either historical or hypothetical, are regularly run and reported for

the overall trading portfolio and individual businesses. Historical

scenarios simulate the impact of price changes that occurred

during a set of extended historical market events. Generally, a 10-

business-day window or longer, representing the most severe point

during a crisis, is selected for each historical scenario.

Hypothetical scenarios provide simulations of anticipated shocks

from pre-defined market stress events. These stress events

include shocks to underlying market risk variables which may be

well beyond the shocks found in the historical data used to

calculate VaR. As with the historical scenarios, the hypothetical

scenarios are designed to represent a short-term market

disruption. Scenarios are reviewed and updated as necessary in

light of changing positions and new economic or political

information. For example, we currently include stress tests that

contemplate a full or partial break-up of the Eurozone. In addition

to the value afforded by the results themselves, this information

provides senior management with a clear picture of the trend of

risk being taken given the relatively static nature of the shocks

applied. Stress testing for the trading portfolio is also integrated

with enterprise-wide stress testing and incorporated into the limits

framework. A process is in place to promote consistency between

the scenarios used for the trading portfolio and those used for

enterprise-wide stress testing. The scenarios used for enterprise-

wide stress testing purposes differ from the typical trading portfolio

scenarios in that they have a longer time horizon and the results

are forecasted over multiple periods for use in consolidated capital

and liquidity planning. For additional information on enterprise-

wide stress testing, see page 64.

Interest Rate Risk Management for Nontrading

Activities

The following discussion presents net interest income excluding

the impact of trading-related activities.

Interest rate risk represents the most significant market risk

exposure to our nontrading balance sheet. Interest rate risk is

measured as the potential volatility in net interest income caused

by changes in market interest rates. Client-facing activities,

primarily lending and deposit-taking, create interest rate sensitive

positions on our balance sheet.

We prepare forward-looking forecasts of net interest income.

The baseline forecast takes into consideration expected future

business growth, ALM positioning and the direction of interest rate

movements as implied by the market-based forward curve. We

then measure and evaluate the impact that alternative interest

rate scenarios have on the baseline forecast in order to assess

interest rate sensitivity under varied conditions. The net interest

income forecast is frequently updated for changing assumptions

and differing outlooks based on economic trends, market

conditions and business strategies. Thus, we continually monitor

our balance sheet position in an effort to maintain an acceptable

level of exposure to interest rate changes.

The interest rate scenarios that we analyze incorporate balance

sheet assumptions such as loan and deposit growth and pricing,

changes in funding mix, product repricing and maturity

characteristics, but do not include the impact of hedge

ineffectiveness. Our overall goal is to manage interest rate risk so

that movements in interest rates do not significantly adversely

affect core net interest income and capital.

The spot and 12-month forward rates used in our baseline

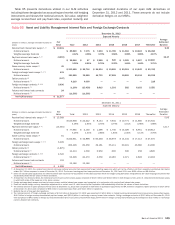

forecast at December 31, 2012 and 2011 are presented in Table

63.

Table 63 Forward Rates

December 31, 2012

Federal

Funds

Three-

Month

LIBOR

10-Year

Swap

Spot rates 0.25% 0.31% 1.84%

12-month forward rates 0.25 0.37 2.10

December 31, 2011

Spot rates 0.25% 0.58% 2.03%

12-month forward rates 0.25 0.75 2.29