Bank of America 2012 Annual Report Download - page 216

Download and view the complete annual report

Please find page 216 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

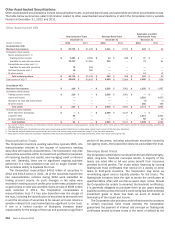

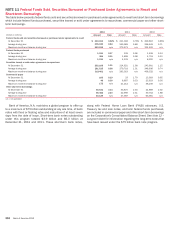

214 Bank of America 2012

over accruals at December 31, 2012 compared to up to $5 billion

over accruals at December 31, 2011 for only non-GSE

representations and warranties exposures. The range of possible

loss at December 31, 2012 reflects the impact of the FNMA

Settlement and, as a result, addresses principally non-GSE

exposures. The reduction in the range of possible loss from

December 31, 2011 is the net impact of, among other changes,

updated assumptions and other developments. The estimated

range of possible loss related to these representations and

warranties exposures does not represent a probable loss, and is

based on currently available information, significant judgment and

a number of assumptions, including those set forth below, that

are subject to change.

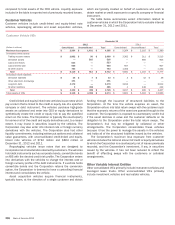

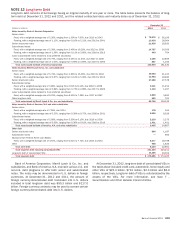

Future provisions and/or ranges of possible loss for

representations and warranties may be significantly impacted if

actual experiences are different from the Corporation’s

assumptions in its predictive models, including, without limitation,

ultimate resolution of the BNY Mellon Settlement, estimated

repurchase rates, economic conditions, estimated home prices,

consumer and counterparty behavior, and a variety of other

judgmental factors. Adverse developments with respect to one or

more of the assumptions underlying the liability for representations

and warranties and the corresponding estimated range of possible

loss could result in significant increases to future provisions and/

or the estimated range of possible loss. For example, if courts, in

the context of claims brought by private-label securitization

trustees, were to disagree with the Corporation’s interpretation

that the underlying agreements require a claimant to prove that

the representations and warranties breach was the cause of the

loss, it could significantly impact the estimated range of possible

loss. Additionally, if recent court rulings related to monoline

litigation, including one related to the Corporation, that have

allowed sampling of loan files instead of requiring a loan-by-loan

review to determine if a representations and warranties breach

has occurred, are followed generally by the courts in future

monoline litigation, private-label securitization counterparties may

view litigation as a more attractive alternative compared to a loan-

by-loan review. Finally, although the Corporation believes that the

representations and warranties typically given in non-GSE

transactions are less rigorous and actionable than those given in

GSE transactions, the Corporation does not have significant

experience resolving loan-level claims in non-GSE transactions to

measure the impact of these differences on the probability that a

loan will be required to be repurchased.

The liability for obligations and representations and warranties

exposures and the corresponding estimated range of possible loss

do not consider any losses related to litigation matters, including

litigation brought by monoline insurers, nor do they include any

separate foreclosure costs and related costs, assessments and

compensatory fees or any other possible losses related to

potential claims for breaches of performance of servicing

obligations (except as such losses are included as potential costs

of the BNY Mellon Settlement), potential securities law or fraud

claims or potential indemnity or other claims against the

Corporation, including claims related to loans insured by the FHA.

The Corporation is not able to reasonably estimate the amount of

any possible loss with respect to any such servicing, securities

law, fraud or other claims against the Corporation, except to the

extent reflected in the aggregate range of possible loss for litigation

and regulatory matters disclosed in Note 13 – Commitments and

Contingencies; however, such loss could be material.

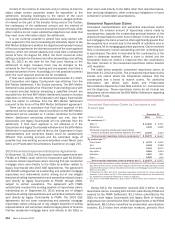

Government-sponsored Enterprises Experience

Generally, the Corporation first becomes aware that a GSE is

evaluating a particular loan for repurchase when the Corporation

receives a request from a GSE to review the underlying loan file

(file request). Upon completing its review, the GSE may submit a

repurchase claim to the Corporation. As soon as practicable after

receiving a repurchase claim from a GSE, the Corporation

evaluates the claim and takes appropriate action. Claim disputes

are generally handled through loan-level negotiations with the

GSEs and the Corporation seeks to resolve the repurchase claim

within 90 to 120 days of the receipt of the claim although claims

remain open beyond this timeframe. Disputes include

reasonableness of stated income, occupancy, undisclosed

liabilities, and the validity of MI claim rescissions in the vintages

with the highest default rates.

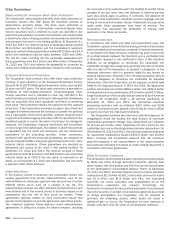

The Corporation and its subsidiaries have an established

history of working with the GSEs on repurchase claims. In 2012,

the Corporation continued to experience elevated levels of claims

from FNMA, including claims on loans on which borrowers have

made a significant number of payments (e.g., at least 25

payments) and, to a lesser extent, loans that defaulted more than

18 months prior to the repurchase request. The FNMA Settlement

resolved substantially all of the claims with respect to loans

originated and sold to FNMA between January 1, 2000 and

December 31, 2008, as well as substantially all future

representations and warranties repurchase claims associated with

these loans.

Monoline Insurers Experience

The Corporation has had limited representations and warranties

repurchase claims experience with the monoline insurers, due to

ongoing litigation against legacy Countrywide and/or Bank of

America. To the extent the Corporation received repurchase claims

from the monolines that are properly presented, it generally reviews

them on a loan-by-loan basis. Where a breach of representations

and warranties given by the Corporation or subsidiaries or legacy

companies is confirmed on a given loan, settlement is generally

reached as to that loan within 60 to 90 days.

For the monolines that have instituted litigation against legacy

Countrywide and/or Bank of America, when claims from these

counterparties are denied, the Corporation does not indicate its

reason for denial as it is not contractually obligated to do so. In

the Corporation’s experience, the monolines have been generally

unwilling to withdraw repurchase claims, regardless of whether

and what evidence was offered to refute a claim. When a claim

has been denied and there has not been communication with the

counterparty for six months, the Corporation views these claims

as inactive; however, they remain in the outstanding claims balance

until resolution.

To the extent there are repurchase claims based on valid

identified loan defects and the Corporation has determined that

there is a breach of a representation and warranty and that any

other requirements for repurchase have been met, a liability for

representations and warranties is established. Outside of the

standard quality control process that is an integral part of the

Corporation’s loan origination process, the Corporation does not

generally review loan files until a repurchase claim is received,

including with respect to monoline exposures. In view of the

inherent difficulty of predicting the outcome of those repurchase

claims where a valid defect has not been identified or in predicting

future claim requests and the related outcome in the case of