Bank of America 2012 Annual Report Download - page 255

Download and view the complete annual report

Please find page 255 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 253

Management concluded that no valuation allowance is

necessary to reduce the U.K. NOL carryforwards and U.S. NOL and

general business credit carryforwards since estimated future

taxable income will be sufficient to utilize these assets prior to

their expiration. The majority of the Corporation’s U.K. net deferred

tax assets, which consist primarily of NOLs, are realizable by

certain subsidiaries that have a recent history of cumulative

losses. For the deferred tax assets of those subsidiaries, the

cessation of certain business activities, changes to capital and

funding, forecasts of business volumes and the indefinite period

to carry forward NOLs represent significant positive evidence

supporting management’s conclusion. However, significant

changes to those estimates, such as changes that would be

caused by a substantial and prolonged worsening of the condition

of Europe’s capital markets, could lead management to reassess

its U.K. valuation allowance conclusions.

At December 31, 2012, U.S. federal income taxes had not been

provided on $17.2 billion of undistributed earnings of non-U.S.

subsidiaries that management has determined have been

reinvested for an indefinite period of time. If the Corporation were

to record a deferred tax liability associated with these

undistributed earnings, the amount would be approximately $4.3

billion at December 31, 2012.

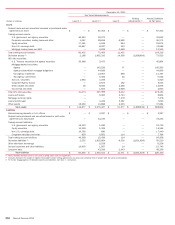

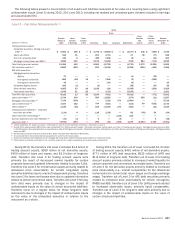

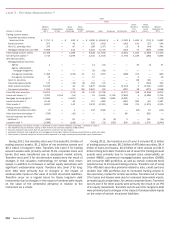

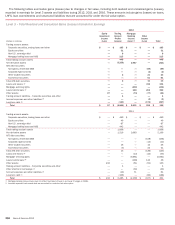

NOTE 21 Fair Value Measurements

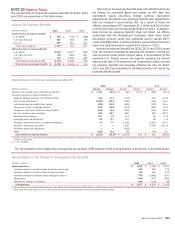

Under applicable accounting guidance, fair value is defined as the

exchange price that would be received for an asset or paid to

transfer a liability (an exit price) in the principal or most

advantageous market for the asset or liability in an orderly

transaction between market participants on the measurement

date. The Corporation determines the fair values of its financial

instruments based on the fair value hierarchy established under

applicable accounting guidance which requires an entity to

maximize the use of observable inputs and minimize the use of

unobservable inputs when measuring fair value. There are three

levels of inputs used to measure fair value. The Corporation

conducts a review of its fair value hierarchy classifications on a

quarterly basis. Transfers into or out of fair value hierarchy

classifications are made if the significant inputs used in the

financial models measuring the fair values of the assets and

liabilities became unobservable or observable, respectively, in the

current marketplace. These transfers are considered to be

effective as of the beginning of the quarter in which they occur.

For more information regarding the fair value hierarchy and how

the Corporation measures fair value, see Note 1 – Summary of

Significant Accounting Principles. The Corporation accounts for

certain financial instruments under the fair value option. For more

information, see Note 22 – Fair Value Option.

Valuation Processes and Techniques

The Corporation has various processes and controls in place to

ensure that fair value is reasonably estimated. A model validation

policy governs the use and control of valuation models used to

estimate fair value. This policy requires review and approval of

models by personnel who are independent of the front office, and

periodic re-assessments of models to ensure that they are

continuing to perform as designed. In addition, detailed reviews

of trading gains and losses are conducted on a daily basis by

personnel who are independent of the front office. A price

verification group, which is also independent of the front office,

utilizes available market information including executed trades,

market prices and market-observable valuation model inputs to

ensure that fair values are reasonably estimated. The Corporation

performs due diligence procedures over third-party pricing service

providers in order to support their use in the valuation process.

Where market information is not available to support internal

valuations, independent reviews of the valuations are performed

and any material exposures are escalated through a management

review process.

While the Corporation believes its valuation methods are

appropriate and consistent with other market participants, the use

of different methodologies or assumptions to determine the fair

value of certain financial instruments could result in a different

estimate of fair value at the reporting date.

During 2012, there were no changes to the valuation

techniques that had, or are expected to have, a material impact

on its consolidated financial position or results of operations.

Level 1, 2 and 3 Valuation Techniques

Financial instruments are considered Level 1 when the valuation

is based on quoted prices in active markets for identical assets

or liabilities. Level 2 financial instruments are valued using quoted

prices for similar assets or liabilities, quoted prices in markets

that are not active, or models using inputs that are observable or

can be corroborated by observable market data for substantially

the full term of the assets or liabilities. Financial instruments are

considered Level 3 when their values are determined using pricing

models, discounted cash flow methodologies or similar

techniques, and at least one significant model assumption or input

is unobservable and when determination of the fair value requires

significant management judgment or estimation.

Trading Account Assets and Liabilities and Available-for-

sale Debt Securities

The fair values of trading account assets and liabilities are primarily

based on actively traded markets where prices are based on either

direct market quotes or observed transactions. The fair values of

AFS debt securities are generally based on quoted market prices

or market prices for similar assets. Liquidity is a significant factor

in the determination of the fair values of trading account assets

and liabilities and AFS debt securities. Market price quotes may

not be readily available for some positions, or positions within a

market sector where trading activity has slowed significantly or

ceased. Some of these instruments are valued using a discounted

cash flow model, which estimates the fair value of the securities

using internal credit risk, interest rate and prepayment risk models

that incorporate management’s best estimate of current key

assumptions such as default rates, loss severity and prepayment

rates. Principal and interest cash flows are discounted using an

observable discount rate for similar instruments with adjustments

that management believes a market participant would consider in

determining fair value for the specific security. Other instruments

are valued using a net asset value approach which considers the

value of the underlying securities. Underlying assets are valued

using external pricing services, where available, or matrix pricing

based on the vintages and ratings. Situations of illiquidity generally

are triggered by the market’s perception of credit uncertainty

regarding a single company or a specific market sector. In these

instances, fair value is determined based on limited available

market information and other factors, principally from reviewing

the issuer’s financial statements and changes in credit ratings

made by one or more rating agencies.