Bank of America 2012 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 111

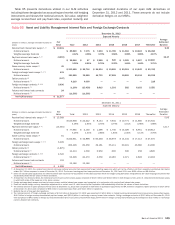

The histogram below is a graphic depiction of trading volatility

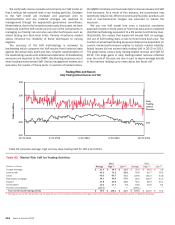

and illustrates the daily level of trading-related revenue for 2012

and 2011. During 2012, positive trading-related revenue was

recorded for 98 percent, or 243 of the 249 trading days of which

80 percent (199 days) were daily trading gains of over $25 million,

less than one percent (1 day) of the trading days had losses greater

than $25 million and the largest loss was $50 million. This is

compared to 2011, where positive trading-related revenue was

recorded for 86 percent, or 214 of the 250 trading days of which

66 percent (165 days) were daily trading gains of over $25 million,

five percent (12 days) of the trading days had losses greater than

$25 million and the largest loss was $119 million.

To evaluate risk in our trading activities, we focus on the actual

and potential volatility of individual positions as well as portfolios.

VaR is a key statistic used to measure market risk. In order to

manage day-to-day risks, VaR is subject to trading limits both for

our overall trading portfolio and within individual businesses. All

trading limit excesses are communicated to management for

review.

A VaR model simulates the value of a portfolio under a range

of hypothetical scenarios in order to generate a distribution of

potential gains and losses. VaR represents the loss the portfolio

is expected to experience within a given confidence level based

on historical data. With any VaR model, there are significant and

numerous assumptions that will differ from company to company.

In addition, the accuracy of a VaR model depends on the availability

and quality of historical data for each of the positions in the

portfolio. A VaR model may require additional modeling

assumptions for new products that do not have extensive historical

price data or for illiquid positions for which accurate daily prices

are not consistently available.

A VaR model is an effective tool in estimating ranges of potential

gains and losses on our trading portfolios. There are, however,

many limitations inherent in a VaR model as it utilizes historical

results over a defined time period to estimate future performance.

Historical results may not always be indicative of future results

and changes in market conditions or in the composition of the

underlying portfolio could have a material impact on the accuracy

of the VaR model. In order for the VaR model to reflect current

market conditions, we update the historical data underlying our

VaR model on a bi-weekly basis and regularly review the

assumptions underlying the model. Our VaR model utilizes three

years of historical data. This time period was chosen to ensure

that VaR reflects both a broad range of market movements as well

as being sensitive to recent changes in market volatility. In

addition, certain types of risks associated with positions that are

illiquid and/or unobservable are not included in VaR. If these risks

are determined to be material, the VaR model results will be

supplemented.