Bank of America 2012 Annual Report Download - page 213

Download and view the complete annual report

Please find page 213 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

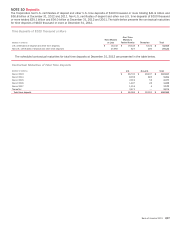

Bank of America 2012 211

party securitization sponsors, and $295 million submitted by

monolines. During 2012, $6.6 billion in claims were resolved,

primarily with the GSEs and through the Syncora Settlement. Of

the resolved claims, $4.6 billion were resolved through rescissions

and $2.0 billion were resolved through mortgage repurchases and

make-whole payments.

The notional amount of unresolved GSE repurchase claims

totaled $13.5 billion at December 31, 2012 compared to $6.2

billion at December 31, 2011. As a result of the FNMA Settlement,

$12.2 billion of GSE repurchase claims outstanding at

December 31, 2012 were resolved in January 2013. For further

discussion of the Corporation’s experience with the GSEs, see

Government-sponsored Enterprises Experience in this Note.

The notional amount of unresolved monoline repurchase

claims totaled $2.4 billion at December 31, 2012 compared to

$3.1 billion at December 31, 2011. The decrease in unresolved

repurchase claims was driven by resolution of claims through the

Syncora Settlement. The Corporation has had limited loan-level

repurchase claims experience with monoline insurers due to

ongoing litigation. The Corporation has reviewed and declined to

repurchase substantially all of the unresolved repurchase claims

at December 31, 2012 based on an assessment of whether a

breach exists that materially and adversely affected the insurer’s

interest in the mortgage loan. Further, in the Corporation’s

experience, the monolines have been generally unwilling to

withdraw repurchase claims, regardless of whether and what

evidence was offered to refute a claim. Substantially all of the

unresolved monoline claims pertain to second-lien loans and are

currently the subject of litigation. For further discussion of the

Corporation’s practices regarding litigation accruals and range of

possible loss for litigation and regulatory matters, which includes

the status of its monoline litigation, see Estimated Range of

Possible Loss in this Note.

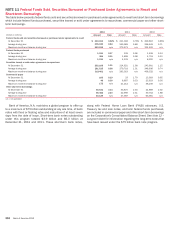

The notional amount of unresolved repurchase claims from

private-label securitization trustees, third-party securitization

sponsors, whole-loan investors and others increased to $12.3

billion at December 31, 2012 compared to $3.3 billion at

December 31, 2011. The increase in the notional amount of

unresolved repurchase claims is primarily due to increases in the

submission of claims by private-label securitization trustees and

a third-party securitization sponsor; the level of detail, support and

analysis which impacts overall claim quality and, therefore, claims

resolution; and the lack of an established process to resolve

disputes related to these claims. The Corporation anticipated an

increase in aggregate non-GSE claims at the time of the BNY Mellon

Settlement in June 2011, and such increase in aggregate non-

GSE claims was taken into consideration in developing the

increase in the Corporation’s representations and warranties

liability at that time. The Corporation expects unresolved

repurchase claims related to private-label securitizations to

continue to increase as claims continue to be submitted by private-

label securitization trustees and third-party securitization

sponsors, and there is not an established process for the ultimate

resolution of claims on which there is a disagreement. For further

discussion of the Corporation’s experience with whole loans and

private-label securitizations, see Whole Loan Sales and Private-

label Securitizations Experience in this Note.

In addition to the total unresolved repurchase claims, the

Corporation has received repurchase demands from private-label

securitization investors and a master servicer where it believes

the claimants have not satisfied the contractual thresholds to

direct the securitization trustee to take action and/or that these

demands are otherwise procedurally or substantively invalid. The

total amounts outstanding of such demands were $1.6 billion and

$1.7 billion at December 31, 2012 and 2011. At December 31,

2011, the $1.7 billion of demands outstanding were related to

Covered Trusts in the BNY Mellon Settlement of which $1.4 billion

were subsequently resolved through the July 2012 dismissal of a

lawsuit brought by Walnut Place (11 entities with the common

name Walnut Place, including Walnut Place LLC, and Walnut Place

II LLC through Walnut Place XI LLC). Additional demands totaling

$1.3 billion were received during 2012. The Corporation does not

believe that the $1.6 billion in demands outstanding at

December 31, 2012 are valid repurchase claims, and therefore it

is not possible to predict the resolution with respect to such

demands.

Mortgage Insurance Rescission Notices

In addition to repurchase claims, the Corporation receives notices

from mortgage insurance companies of claim denials,

cancellations or coverage rescission (collectively, MI rescission

notices) and the number of such notices has remained elevated.

By way of background, MI compensates lenders or investors for

certain losses resulting from borrower default on a mortgage loan.

When there is disagreement with the mortgage insurer as to the

resolution of a MI rescission notice, meaningful dialogue and

negotiation between the mortgage insurance company and the

Corporation are generally necessary to reach a resolution on an

individual notice. The level of engagement of the mortgage

insurance companies varies and ongoing litigation involving some

of the mortgage insurance companies over individual and bulk

rescissions or claims for rescission limits the ability of the

Corporation to engage in constructive dialogue leading to

resolution.

For loans sold to GSEs or private-label securitization trusts

(including those wrapped by the monoline bond insurers), when

the Corporation receives a MI rescission notice from a mortgage

insurance company, it may give rise to a claim for breach of the

applicable representations and warranties from the GSEs or

private-label securitization trusts, depending on the governing

sales contracts. In those cases where the governing contract

contains MI-related representations and warranties, which upon

rescission requires the Corporation to repurchase the affected

loan or indemnify the investor for the related loss, the Corporation

realizes the loss without the benefit of MI. See below for a

discussion of the impact of the FNMA Settlement. In addition,

mortgage insurance companies have in some cases asserted the

ability to curtail MI payments as a result of alleged foreclosure

delays, which if successful, would reduce the MI proceeds available

to reduce the loss on the loan.

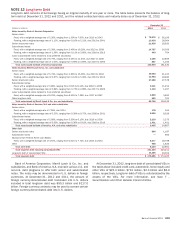

At December 31, 2012, the Corporation had approximately

110,000 open MI rescission notices compared to 90,000 at

December 31, 2011, including 49,000 pertaining principally to

first-lien mortgages serviced for others, 11,000 pertaining to loans

held-for-investment, and 50,000 pertaining to ongoing litigation

for second-lien mortgages. Approximately 27,000 of the open MI

rescission notices pertaining to first-lien mortgages serviced for

others are related to loans sold to FNMA. As of December 31,

2012, 32 percent of the MI rescission notices received have been

resolved. Of those resolved, 20 percent were resolved through the

Corporation’s acceptance of the MI rescission, 58 percent were

resolved through reinstatement of coverage or payment of the

claim by the mortgage insurance company, and 22 percent were

resolved on an aggregate basis through settlement, policy