Bank of America 2012 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

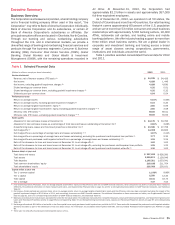

28 Bank of America 2012

Business Segment Results

The following discussion provides an overview of the results of our business segments and All Other for 2012 compared to 2011. For

additional information on these results, see Business Segment Operations on page 33.

Table 6 Business Segment Results

Total Revenue (1)

Provision for Credit

Losses Noninterest Expense Net Income (Loss)

(Dollars in millions) 2012 2011 2012 2011 2012 2011 2012 2011

Consumer & Business Banking $ 29,023 $ 32,880 $ 3,941 $ 3,490 $ 16,793 $ 17,719 $ 5,321 $ 7,447

Consumer Real Estate Services 8,759 (3,154) 1,442 4,524 17,306 21,791 (6,507)(19,465)

Global Banking 17,207 17,312 (103) (1,118) 8,308 8,884 5,725 6,046

Global Markets 13,519 14,798 3(56) 10,839 12,244 1,054 988

Global Wealth & Investment Management 16,517 16,495 266 398 12,755 13,383 2,223 1,718

All Other (790) 16,095 2,620 6,172 6,092 6,253 (3,628)4,712

Total FTE basis 84,235 94,426 8,169 13,410 72,093 80,274 4,188 1,446

FTE adjustment (901) (972) ——————

Total Consolidated $ 83,334 $ 93,454 $ 8,169 $ 13,410 $ 72,093 $ 80,274 $ 4,188 $ 1,446

(1) Total revenue is net of interest expense and is on a FTE basis which for consolidated revenue is a non-GAAP financial measure. For more information on this measure, see Supplemental Financial

Data on page 31, and for a corresponding reconciliation to a GAAP financial measure, see Statistical Table XVI.

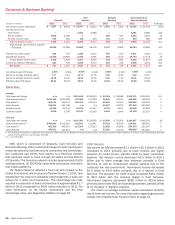

CBB net income decreased compared to the prior year. Revenue

decreased driven by lower average loan balances, the continued

low rate environment, the full-year impact of the Durbin

Amendment, lower gains on sales of portfolios and the impact of

charges related to our consumer protection products. The

provision for credit losses increased as portfolio trends stabilized

during 2012. Noninterest expense declined due to lower Federal

Deposit Insurance Corporation (FDIC) and operating expenses,

partially offset by an increase in litigation expense.

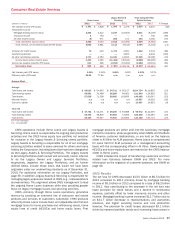

CRES net loss decreased compared to the prior year. Revenue

increased due to a significantly lower representations and

warranties provision, an increase in servicing income and core

production income, partially offset by a decrease in insurance

income. The provision for credit losses decreased due to improved

portfolio trends and increasing home prices in both the non-PCI

and PCI home equity loan portfolios. Noninterest expense

decreased due to a decline in litigation expense, the absence of

a goodwill impairment charge and lower mortgage-related

assessments, waivers and similar costs related to foreclosure

delays, partially offset by higher default-related servicing costs and

a provision for the 2013 IFR Acceleration Agreement.

Global Banking net income decreased compared to the prior

year. Revenue decreased primarily driven by lower investment

banking fees, lower net interest income as a result of spread

compression and the benefit in the prior year from higher accretion

on acquired portfolios, partially offset by the impact of higher

average loan and deposit balances and gains from certain legacy

portfolios. The provision for credit losses increased as a result of

stabilization of asset quality, core commercial loan growth and the

impact of a higher volume of loan resolutions in the commercial

real estate portfolio in the prior year. Noninterest expense

decreased primarily due to lower personnel and operating

expenses.

Global Markets net income increased compared to the prior

year. Sales and trading revenue decreased due to net DVA losses

compared to net DVA gains in the prior year. Excluding net DVA,

sales and trading revenue increased primarily driven by our fixed

income, currencies and commodities (FICC) business as a result

of improved performance in our rates and currencies, and credit-

related businesses due to an improved global economic climate,

and a gain on the sale of an equity investment. Noninterest

expense decreased largely due to a reduction in personnel-related

expenses.

GWIM net income increased compared to the prior year.

Revenue was relatively unchanged as higher asset management

fees were offset by lower transactional revenue and lower net

interest income driven by the impact of the continued low rate

environment. The provision for credit losses decreased driven by

lower delinquencies and improving portfolio trends within the

residential mortgage portfolio. Noninterest expense decreased

due to lower FDIC expense, lower litigation costs and other expense

reductions, partially offset by higher production-related expenses.

All Other decreased to a net loss compared to net income in

the prior year. The change was primarily due to negative fair value

adjustments on structured liabilities compared to positive fair

value adjustments in the prior year, a decrease in equity investment

income and lower gains on sales of debt securities. Partially

offsetting these items were a reduction in the provision for credit

losses, net gains resulting from the repurchase of certain debt

and trust preferred securities and a net income tax benefit related

to the recognition of certain foreign tax credits.