Bank of America 2012 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

112 Bank of America 2012

We continually review, evaluate and enhance our VaR model so

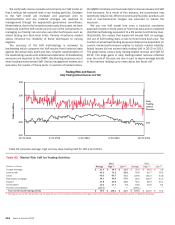

that it reflects the material risks in our trading portfolio. Changes

to the VaR model are reviewed and approved prior to

implementation and any material changes are reported to

management through the appropriate governance committees.

Nevertheless, due to the limitations previously discussed, we have

historically used the VaR model as only one of the components in

managing our trading risk and also use other techniques such as

stress testing and desk level limits. Periods of extreme market

stress influence the reliability of these techniques to varying

degrees.

The accuracy of the VaR methodology is reviewed by

backtesting which compares the VaR results from historical data

against the actual daily profit and loss. Graphic representation of

the backtesting results with additional explanation of backtesting

excesses are reported to the GMRC. Backtesting excesses occur

when trading losses exceed VaR. Senior management reviews and

evaluates the results of these tests. In periods of market stress,

the GMRC members communicate daily to discuss losses and VaR

limit excesses. As a result of this process, the businesses may

selectively reduce risk. Where economically feasible, positions are

sold or macroeconomic hedges are executed to reduce the

exposure.

We use one VaR model that uses a historical simulation

approach based on three years of historical data and an expected

shortfall methodology equivalent to a 99 percent confidence level.

Statistically, this means that losses will exceed VaR, on average,

one out of 100 trading days, or two to three times each year. The

number of actual backtesting excesses observed is dependent on

current market performance relative to historic market volatility.

Actual losses did not exceed daily trading VaR in 2012 or 2011.

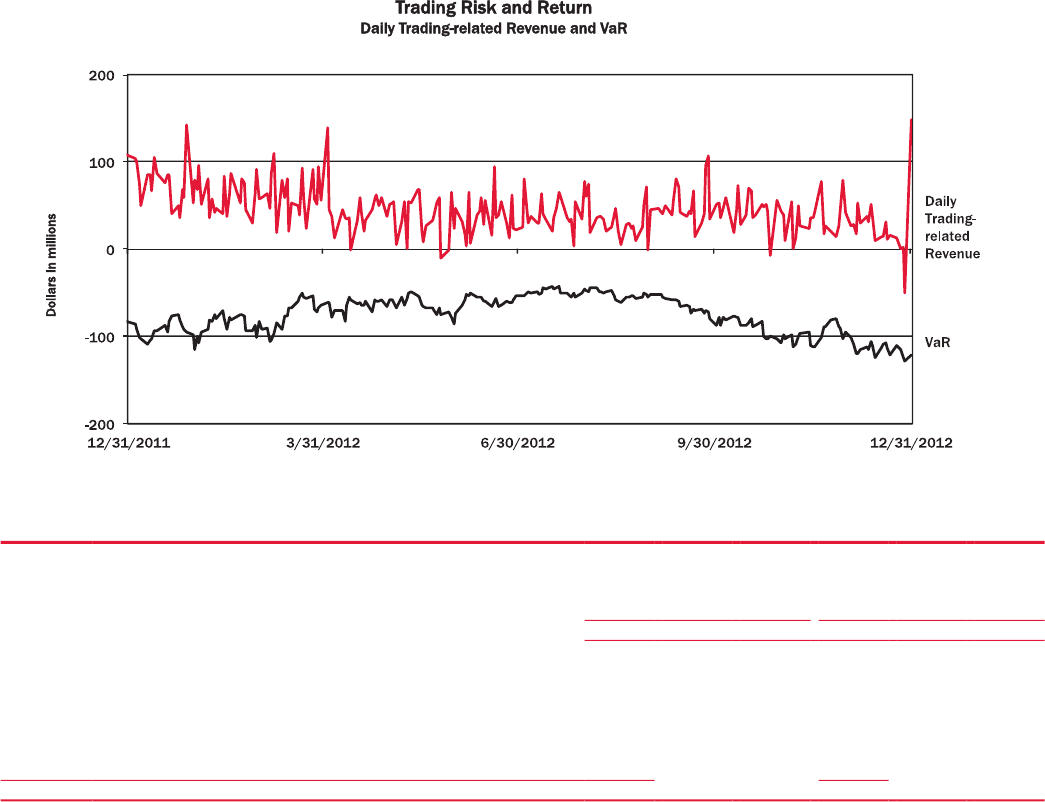

The graph below shows daily trading-related revenue and VaR for

2012. The large gains in daily trading-related revenue reflected

near the end of the year, are due in part to above average activity

in the markets leading up to news about the fiscal cliff.

Table 62 presents average, high and low daily trading VaR for 2012 and 2011.

Table 62 Market Risk VaR for Trading Activities

2012 2011

(Dollars in millions) Average High (1) Low (1) Average High (1) Low (1)

Foreign exchange $21.4 $34.3 $11.5 $ 20.0 $ 48.6 $ 5.6

Interest rate 46.3 75.3 29.8 50.6 82.7 29.2

Credit 49.5 80.7 31.1 109.9 155.3 54.8

Real estate/mortgage 34.1 45.0 27.6 80.0 139.5 31.5

Equities 27.8 54.8 14.6 50.5 88.9 25.1

Commodities 13.0 17.7 7.2 18.9 33.8 8.4

Portfolio diversification (117.1)— —

(163.1) — —

Total market-based trading portfolio $ 75.0 $ 128.1 $ 41.9 $ 166.8 $ 318.6 $ 75.0

(1) The high and low for the total portfolio may not equal the sum of the individual components as the highs or lows of the individual portfolios may have occurred on different trading days.