Bank of America 2012 Annual Report Download - page 198

Download and view the complete annual report

Please find page 198 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

196 Bank of America 2012

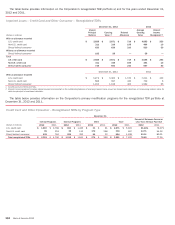

interest rates are rare. Instead, the interest rates are typically

increased, although the increased rate may not represent a market

rate of interest. Infrequently, concessions may also include

principal forgiveness in connection with foreclosure, short sale or

other settlement agreements leading to termination or sale of the

loan.

At the time of restructuring, the loans are remeasured to reflect

the impact, if any, on projected cash flows resulting from the

modified terms. If there was no forgiveness of principal and the

interest rate was not decreased, the modification may have little

or no impact on the allowance established for the loan. If a portion

of the loan is deemed to be uncollectible, a charge-off may be

recorded at the time of restructuring. Alternatively, a charge-off

may have already been recorded in a previous period such that no

charge-off is required at the time of modification. For information

concerning modifications for the U.S. small business commercial

portfolio, see Credit Card and Other Consumer in this Note.

At December 31, 2012 and 2011, remaining commitments to

lend additional funds to debtors whose terms have been modified

in a commercial loan TDR were immaterial. Commercial foreclosed

properties totaled $250 million and $612 million at December 31,

2012 and 2011.

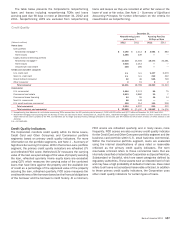

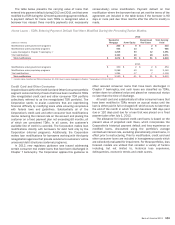

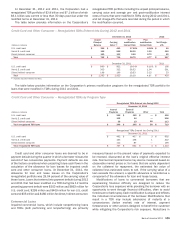

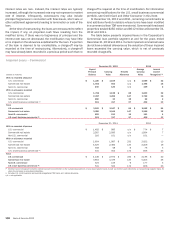

The table below presents impaired loans in the Corporation’s

Commercial loan portfolio segment at and for the years ended

December 31, 2012 and 2011. Certain impaired commercial loans

do not have a related allowance as the valuation of these impaired

loans exceeded the carrying value, which is net of previously

recorded charge-offs.

Impaired Loans – Commercial

December 31, 2012 2012

(Dollars in millions)

Unpaid

Principal

Balance

Carrying

Value

Related

Allowance

Average

Carrying

Value

Interest

Income

Recognized (1)

With no recorded allowance

U.S. commercial $ 1,220 $ 1,109 n/a $ 1,089 $ 32

Commercial real estate 1,003 902 n/a 1,496 16

Non-U.S. commercial 240 120 n/a 129 2

With an allowance recorded

U.S. commercial 1,782 1,138 $ 68 1,603 32

Commercial real estate 2,287 1,262 147 1,749 16

Non-U.S. commercial 280 33 18 52 2

U.S. small business commercial (2) 361 317 97 409 13

Total

U.S. commercial $ 3,002 $ 2,247 $ 68 $ 2,692 $ 64

Commercial real estate 3,290 2,164 147 3,245 32

Non-U.S. commercial 520 153 18 181 4

U.S. small business commercial (2) 361 317 97 409 13

December 31, 2011 2011

With no recorded allowance

U.S. commercial $ 1,482 $ 985 n/a $ 774 $ 7

Commercial real estate 2,587 2,095 n/a 1,994 7

Non-U.S. commercial 216 101 n/a 101 —

With an allowance recorded

U.S. commercial 2,654 1,987 $ 232 2,422 13

Commercial real estate 3,329 2,384 135 3,309 19

Non-U.S. commercial 308 58 6 76 3

U.S. small business commercial (2) 531 503 172 666 23

Total

U.S. commercial $ 4,136 $ 2,972 $ 232 $ 3,196 $ 20

Commercial real estate 5,916 4,479 135 5,303 26

Non-U.S. commercial 524 159 6 177 3

U.S. small business commercial (2) 531 503 172 666 23

(1) Interest income recognized includes interest accrued and collected on the outstanding balances of accruing impaired loans as well as interest cash collections on nonaccruing impaired loans for

which the principal is considered collectible.

(2) Includes U.S. small business commercial renegotiated TDR loans and related allowance.

n/a = not applicable