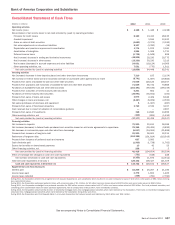

Bank of America 2012 Annual Report Download - page 168

Download and view the complete annual report

Please find page 168 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

166 Bank of America 2012

The Corporation primarily uses VIEs for its securitization

activities, in which the Corporation transfers whole loans or debt

securities into a trust or other vehicle such that the assets are

legally isolated from the creditors of the Corporation. Assets held

in a trust can only be used to settle obligations of the trust. The

creditors of these trusts typically have no recourse to the

Corporation except in accordance with the Corporation’s

obligations under standard representations and warranties.

When the Corporation is the servicer of whole loans held in a

securitization trust, including non-agency residential mortgages,

home equity loans, credit cards, automobile loans and student

loans, the Corporation has the power to direct the most significant

activities of the trust. The Corporation does not have the power

to direct the most significant activities of a residential mortgage

agency trust unless the Corporation holds substantially all of the

issued securities and has the unilateral right to liquidate the trust.

The power to direct the most significant activities of a commercial

mortgage securitization trust is typically held by the special

servicer or by the party holding specific subordinate securities

which embody certain controlling rights. The Corporation

consolidates a whole-loan securitization trust if it has the power

to direct the most significant activities and also holds securities

issued by the trust or has other contractual arrangements, other

than standard representations and warranties, that could

potentially be significant to the trust.

The Corporation may also transfer trading account securities

and AFS securities into municipal bond or resecuritization trusts.

The Corporation consolidates a municipal bond or resecuritization

trust if it has control over the ongoing activities of the trust such

as the remarketing of the trust’s liabilities or, if there are no ongoing

activities, sole discretion over the design of the trust, including

the identification of securities to be transferred in and the structure

of securities to be issued, and also retains securities or has

liquidity or other commitments that could potentially be significant

to the trust. The Corporation does not consolidate a municipal

bond or resecuritization trust if one or a limited number of third-

party investors share responsibility for the design of the trust or

have control over the significant activities of the trust through

liquidation or other substantive rights.

Other VIEs used by the Corporation include collateralized debt

obligations (CDOs), investment vehicles created on behalf of

customers and other investment vehicles. The Corporation does

not routinely serve as collateral manager for CDOs and, therefore,

does not typically have the power to direct the activities that most

significantly impact the economic performance of a CDO. However,

following an event of default, if the Corporation is a majority holder

of senior securities issued by a CDO and acquires the power to

manage the assets of the CDO, the Corporation consolidates the

CDO.

The Corporation consolidates a customer or other investment

vehicle if it has control over the initial design of the vehicle or

manages the assets in the vehicle and also absorbs potentially

significant gains or losses through an investment in the vehicle,

derivative contracts or other arrangements. The Corporation does

not consolidate an investment vehicle if a single investor controlled

the initial design of the vehicle or manages the assets in the

vehicles or if the Corporation does not have a variable interest

that could potentially be significant to the vehicle.

Retained interests in securitized assets are initially recorded

at fair value. In addition, the Corporation may invest in debt

securities issued by unconsolidated VIEs. Fair values of these debt

securities, which are AFS debt securities or trading account assets,

are based primarily on quoted market prices. Generally, quoted

market prices for retained residual interests are not available;

therefore, the Corporation estimates fair values based on the

present value of the associated expected future cash flows. This

may require management to estimate credit losses, prepayment

speeds, forward interest yield curves, discount rates and other

factors that impact the value of retained interests. Retained

residual interests in unconsolidated securitization trusts are

classified in trading account assets or other assets with changes

in fair value recorded in income. The Corporation may also enter

into derivatives with unconsolidated VIEs, which are carried at fair

value with changes in fair value recorded in income.

Fair Value

The Corporation measures the fair values of its financial

instruments in accordance with accounting guidance that requires

an entity to base fair value on exit price. A three-level hierarchy for

inputs is utilized in measuring fair value which maximizes the use

of observable inputs and minimizes the use of unobservable inputs

by requiring that observable inputs be used to determine the exit

price when available. Under applicable accounting guidance, the

Corporation categorizes its financial instruments, based on the

priority of inputs to the valuation technique, into this three-level

hierarchy, as described below. Trading account assets and

liabilities, derivative assets and liabilities, AFS debt and equity

securities, MSRs and certain other assets are carried at fair value

in accordance with applicable accounting guidance. The

Corporation has also elected to account for certain assets and

liabilities under the fair value option, including certain commercial

and consumer loans and loan commitments, LHFS, other short-

term borrowings, securities financing agreements, asset-backed

secured financings, long-term deposits and long-term debt. The

following describes the three-level hierarchy.

Level 1 Unadjusted quoted prices in active markets for identical

assets or liabilities. Level 1 assets and liabilities include

debt and equity securities and derivative contracts that

are traded in an active exchange market, as well as

certain U.S. Treasury securities that are highly liquid and

are actively traded in over-the-counter (OTC) markets.

Level 2 Observable inputs other than Level 1 prices, such as

quoted prices for similar assets or liabilities, quoted

prices in markets that are not active, or other inputs that

are observable or can be corroborated by observable

market data for substantially the full term of the assets

or liabilities. Level 2 assets and liabilities include debt

securities with quoted prices that are traded less

frequently than exchange-traded instruments and

derivative contracts where fair value is determined using

a pricing model with inputs that are observable in the

market or can be derived principally from or corroborated

by observable market data. This category generally

includes U.S. government and agency mortgage-backed

debt securities, corporate debt securities, derivative

contracts, residential mortgage loans and certain LHFS.

Level 3 Unobservable inputs that are supported by little or no

market activity and that are significant to the overall fair

value of the assets or liabilities. Level 3 assets and

liabilities include financial instruments for which the

determination of fair value requires significant

management judgment or estimation. The fair value for