Bank of America 2012 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 105

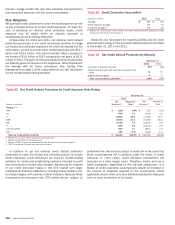

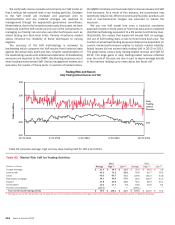

Provision for Credit Losses

The provision for credit losses decreased $5.2 billion to $8.2

billion for 2012 compared to 2011. The provision for credit losses

was $6.7 billion lower than net charge-offs for 2012, resulting in

a reduction in the allowance for credit losses due to improved

portfolio trends and increasing home prices in the consumer real

estate portfolios, lower bankruptcy filings and delinquencies

affecting the Card Services portfolio, and improvement in overall

credit quality within the core commercial portfolio (total

commercial products excluding U.S. small business). Absent

unexpected deterioration in the economy, we expect reductions in

the allowance for credit losses, excluding the valuation allowance

for PCI loans, to continue in the near term, though at a slower pace

than in 2012.

The provision for credit losses for the consumer portfolio

decreased $6.4 billion to $8.0 billion for 2012 compared to 2011.

The improvement was primarily in the consumer real estate loan

portfolios due to improved portfolio trends and an improved home

price outlook in our PCI portfolios. The provision for credit losses

related to the PCI loan portfolios was a provision benefit of $103

million in 2012 as the home price outlook improved, compared to

a provision expense of $2.2 billion in 2011.

The provision for credit losses for the commercial portfolio,

including the unfunded lending commitments, increased $1.1

billion to $197 million in 2012 compared to 2011 due to

stabilization of credit quality, loan growth and a higher volume of

loan resolutions in the prior year, all within the core commercial

portfolio.

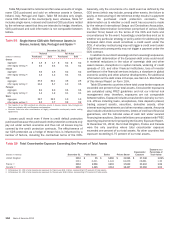

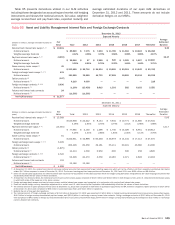

Allowance for Credit Losses

Allowance for Loan and Lease Losses

The allowance for loan and lease losses is comprised of two

components. The first component covers nonperforming

commercial loans and TDRs. The second component covers loans

and leases on which there are incurred losses that are not yet

individually identifiable, as well as incurred losses that may not

be represented in the loss forecast models. We evaluate the

adequacy of the allowance for loan and lease losses based on the

total of these two components, each of which is described in more

detail below. The allowance for loan and lease losses excludes

LHFS and loans accounted for under the fair value option as the

fair value reflects a credit risk component.

The first component of the allowance for loan and lease losses

covers both the nonperforming commercial loans and all TDRs

within the consumer and commercial portfolios. These loans are

subject to impairment measurement based on the present value

of projected future cash flows discounted at the loan’s original

effective interest rate, or in certain circumstances, impairment

may also be based upon the collateral value or the loan’s

observable market price if available. Impairment measurement for

the renegotiated credit card, unsecured consumer and small

business TDR portfolios is based on the present value of projected

cash flows discounted using the average portfolio contractual

interest rate, excluding promotionally priced loans, in effect prior

to restructuring. For purposes of computing this specific loss

component of the allowance, larger impaired loans are evaluated

individually and smaller impaired loans are evaluated as a pool

using historical loss experience for the respective product types

and risk ratings of the loans.

The second component of the allowance for loan and lease

losses covers the remaining consumer and commercial loans and

leases that have incurred losses which are not yet individually

identifiable. The allowance for consumer and certain

homogeneous commercial loan and lease products is based on

aggregated portfolio evaluations, generally by product type. Loss

forecast models are utilized that consider a variety of factors

including, but not limited to, historical loss experience, estimated

defaults or foreclosures based on portfolio trends, delinquencies,

economic trends and credit scores. Our consumer real estate loss

forecast model estimates the portion of loans that will default

based on individual loan attributes, the most significant of which

are refreshed LTV or CLTV, and borrower credit score as well as

vintage and geography, all of which are further broken down into

current delinquency status. Additionally, we incorporate the

delinquency status of underlying first-lien loans on our junior-lien

home equity portfolio in our allowance process. Incorporating

refreshed LTV and CLTV into our probability of default allows us to

factor the impact of changes in home prices into our allowance

for loan and lease losses. These loss forecast models are updated

on a quarterly basis to incorporate information reflecting the

current economic environment. As of December 31, 2012, the loss

forecast process resulted in reductions in the allowance for all

major consumer portfolios.

The allowance for commercial loan and lease losses is

established by product type after analyzing historical loss

experience by internal risk rating, current economic conditions,

industry performance trends, geographic and obligor

concentrations within each portfolio and any other pertinent

information. The statistical models for commercial loans are

generally updated annually and utilize our historical database of

actual defaults and other data. The loan risk ratings and

composition of the commercial portfolios used to calculate the

allowance are updated at least quarterly to incorporate the most

recent data reflecting the current economic environment. For risk-

rated commercial loans, we estimate the probability of default and

the LGD based on our historical experience of defaults and credit

losses. Factors considered when assessing the internal risk rating

include the value of the underlying collateral, if applicable, the

industry in which the obligor operates, the obligor’s liquidity and

other financial indicators, and other quantitative and qualitative

factors relevant to the obligor’s credit risk. As of December 31,

2012, updates to the loan risk ratings and portfolio composition

resulted in reductions in the allowance for the commercial real

estate, U.S. commercial and commercial lease financing

portfolios.

Also included within the second component of the allowance

for loan and lease losses are reserves to cover losses that are

incurred but, in our assessment, may not be adequately

represented in the historical loss data used in the loss forecast

models. For example, factors that we consider include, among

others, changes in lending policies and procedures, changes in

economic and business conditions, changes in the nature and size

of the portfolio, changes in the volume and severity of past due

loans and nonaccrual loans and the effect of external factors such

as competition, and legal and regulatory requirements. We also

consider factors that are applicable to unique portfolio segments.

For example, we consider the risk of uncertainty in our loss

forecasting models related to junior-lien home equity loans that

are current, but have first-lien loans that we do not service that

are 30 days or more past due. In addition, we consider the inherent

uncertainty in mathematical models that are built upon historical

data.