Bank of America 2012 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

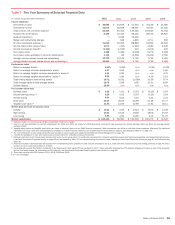

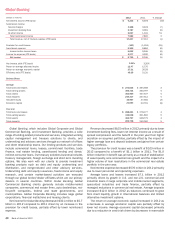

Bank of America 2012 35

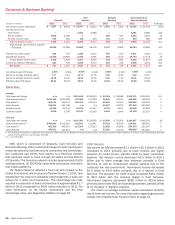

Deposits

Deposits includes the results of consumer deposit activities which

consist of a comprehensive range of products provided to

consumers and small businesses. Our deposit products include

traditional savings accounts, money market savings accounts, CDs

and IRAs, noninterest- and interest-bearing checking accounts, as

well as investment accounts and products. Deposit products

provide a relatively stable source of funding and liquidity for the

Corporation. We earn net interest spread revenue from investing

this liquidity in earning assets through client-facing lending and

ALM activities. The revenue is allocated to the deposit products

using our funds transfer pricing process that matches assets and

liabilities with similar interest rate sensitivity and maturity

characteristics.

Deposits also generates fees such as account service fees,

non-sufficient funds fees, overdraft charges and ATM fees, as well

as investment and brokerage fees from Merrill Edge accounts.

Merrill Edge is an integrated investing and banking service targeted

at clients with less than $250,000 in investable assets. Merrill

Edge provides investment advice and guidance, brokerage

services, a self-directed online investing platform and key banking

capabilities including access to the Corporation’s network of

banking centers and ATMs. Deposits includes the net impact of

migrating customers and their related deposit balances between

Deposits and GWIM as well as other client-managed businesses.

For more information on the migration of customer balances to or

from GWIM, see GWIM on page 46.

Net income for Deposits decreased $300 million to $917

million in 2012 primarily driven by lower net interest income,

partially offset by lower noninterest expense. Net interest income

declined $615 million to $7.9 billion driven by compressed deposit

spreads due to the continued low rate environment, partially offset

by growth in deposit balances, a customer shift to higher spread

liquid products and continued pricing discipline. Noninterest

income of $4.2 billion remained relatively unchanged. Noninterest

expense decreased $191 million to $10.4 billion as lower FDIC

expense was partially offset by higher operating and litigation

expenses.

Average deposits increased $13.2 billion to $434.3 billion in

2012 driven by a customer shift to more liquid products in a low

rate environment as checking, traditional savings and money

market savings grew $23.9 billion. Growth in liquid products was

partially offset by a decline in average time deposits of $10.7

billion. As a result of the shift in the mix of deposits and our

continued pricing discipline, the rate paid on average deposits

declined by seven bps to 20 bps.

Key Statistics

2012 2011

Total deposit spreads (excludes noninterest costs) (1) 1.81% 2.12%

Year end

Client brokerage assets (in millions) $75,946 $66,576

Online banking active accounts (units in thousands) 29,638 29,870

Mobile banking active accounts (units in thousands) 12,013 9,166

Banking centers 5,478 5,702

ATMs 16,347 17,756

(1) Total deposit spreads include the Deposits and Business Banking businesses.

Mobile banking customers increased 2.8 million in 2012

reflecting a change in our customers’ banking preferences. The

number of banking centers declined 224 and ATMs declined 1,409

as we continue to improve our cost-to-serve and optimize our

consumer banking network.

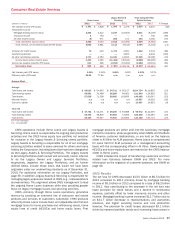

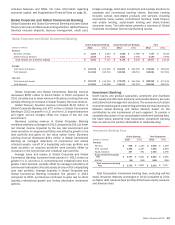

Card Services

Card Services is one of the leading issuers of credit and debit

cards to consumers and small businesses in the U.S. In addition

to earning net interest spread revenue on its lending activities,

Card Services generates interchange revenue from credit and debit

card transactions as well as annual credit card fees and other

miscellaneous fees.

Net income for Card Services decreased $1.8 billion to $4.1

billion in 2012 primarily driven by a decrease in revenue and an

increase in the provision for credit losses, partially offset by lower

noninterest expense. Net interest income decreased $1.5 billion

to $10.0 billion driven by lower average loan balances and yields.

The net interest yield decreased 11 bps to 8.93 percent due to

charge-offs and paydowns of higher interest rate products.

Noninterest income decreased $1.4 billion to $5.2 billion primarily

due to lower interchange fees as a result of implementing the

Durbin Amendment, lower gains on sales of portfolios and the

impact of charges related to our consumer protection products.

The provision for credit losses increased $380 million to $3.5

billion in 2012 as portfolio trends stabilized during 2012. For more

information, see Provision for Credit Losses on page 105.

Noninterest expense decreased $465 million to $5.5 billion

primarily due to lower personnel and operating expenses.

Average loans decreased $14.4 billion to $111.6 billion in

2012 driven by the impact of portfolio sales, charge-offs and

continued run-off of non-core portfolios.

Key Statistics

(Dollars in millions) 2012 2011

U.S. credit card

Gross interest yield 10.02% 10.25%

Risk-adjusted margin 7.54 5.81

New accounts (in thousands) 3,258 3,035

Purchase volumes $ 193,500 $192,358

Debit card purchase volumes 258,363 250,545

During 2012, the U.S. credit card risk-adjusted margin

increased 173 bps due to a decrease in net charge-offs driven by

an improvement in credit quality. U.S. credit card new accounts

grew by approximately 223,000 accounts to 3.3 million. During

2012, U.S. credit card purchase volumes increased $1.1 billion

to $193.5 billion reflecting higher levels of consumer spending,

partially offset by the impact of portfolio sales. Debit card purchase

volumes increased $7.8 billion to $258.4 billion reflecting higher

levels of consumer spending.