Bank of America 2012 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 81

and transfers to foreclosed properties more than offset new

origination volume retained on our balance sheet.

At December 31, 2012 and 2011, the residential mortgage

portfolio included $90.9 billion and $93.9 billion of outstanding

fully-insured loans. On this portion of the residential mortgage

portfolio, we are protected against principal loss as a result of

either FHA insurance or long-term stand-by agreements with FNMA

and FHLMC. At December 31, 2012 and 2011, $66.6 billion and

$69.5 billion had FHA insurance and $24.3 billion and $24.4 billion

were protected by long-term stand-by agreements. All of these

loans are individually insured and therefore the Corporation does

not record an allowance for credit losses with respect to these

loans.

At December 31, 2012 and 2011, $25.5 billion and $24.0

billion of the FHA-insured loan population were delinquent FHA

loans repurchased pursuant to our servicing agreements with

GNMA.

In addition to the long-term stand-by agreements with FNMA

and FHLMC, we have mitigated a portion of our credit risk on the

residential mortgage portfolio through the use of synthetic

securitization vehicles as described in Note 5 – Outstanding Loans

and Leases to the Consolidated Financial Statements. At

December 31, 2012 and 2011, the synthetic securitization

vehicles referenced principal balances of $17.6 billion and $23.9

billion of residential mortgage loans and provided loss protection

up to $500 million and $783 million. At December 31, 2012 and

2011, the Corporation had a receivable of $305 million and $359

million from these vehicles for reimbursement of losses. The

Corporation records an allowance for credit losses on loans

referenced by the synthetic securitization vehicles. The reported

net charge-offs for the residential mortgage portfolio do not include

the benefit of amounts reimbursable from these vehicles.

Adjusting for the benefit of the credit protection from the synthetic

securitizations, the residential mortgage net charge-off ratio,

excluding the Countrywide PCI and fully-insured loan portfolios, for

2012 would have been reduced by nine bps, and 13 bps for 2011.

Synthetic securitizations and the long-term stand-by

agreements with FNMA and FHLMC together reduce our regulatory

risk-weighted assets due to the transfer of a portion of our credit

risk to unaffiliated parties. At December 31, 2012 and 2011, these

programs had the cumulative effect of reducing our risk-weighted

assets by $7.2 billion and $7.9 billion, increasing our Tier 1 capital

ratio by eight bps for both periods, and our Tier 1 common capital

ratio by seven bps and six bps.

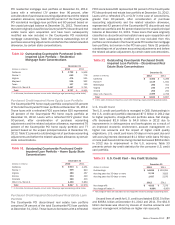

Table 25 presents certain residential mortgage key credit

statistics on both a reported basis excluding loans accounted for

under the fair value option, and excluding the Countrywide PCI loan

portfolio, fully-insured loan portfolio and loans accounted for under

the fair value option. We believe the presentation of information

adjusted to exclude these loan portfolios is more representative

of the credit risk in the residential mortgage loan portfolio. As

such, the following discussion presents the residential mortgage

portfolio excluding the Countrywide PCI loan portfolio, the fully-

insured loan portfolio and loans accounted for under the fair value

option. For more information on the Countrywide PCI loan portfolio,

see page 86.

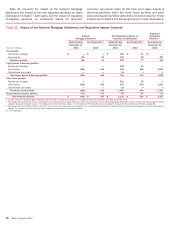

Table 25 Residential Mortgage – Key Credit Statistics

December 31

Reported Basis (1)

Excluding Countrywide

Purchased Credit-impaired

and Fully-insured Loans

(Dollars in millions) 2012 2011 2012 2011

Outstandings $ 243,181 $ 262,290 $ 143,590 $ 158,470

Accruing past due 30 days or more 28,780 28,688 3,082 3,950

Accruing past due 90 days or more 22,157 21,164 n/a n/a

Nonperforming loans (2) 14,808 15,970 14,808 15,970

Percent of portfolio

Refreshed LTV greater than 90 but less than 100 16% 15% 10%11%

Refreshed LTV greater than 100 28 33 20 26

Refreshed FICO below 620 22 21 14 15

2006 and 2007 vintages (3) 24 27 34 37

Net charge-off ratio (2, 4) 1.21 1.45 2.02 2.27

(1) Outstandings, accruing past due, nonperforming loans and percentages of portfolio exclude loans accounted for under the fair value option. There were $147 million and $906 million of residential

mortgage loans accounted for under the fair value option at December 31, 2012 and 2011. See Consumer Portfolio Credit Risk Management – Consumer Loans Accounted for Under the Fair Value

Option on page 89 and Note 22 – Fair Value Option to the Consolidated Financial Statements for additional information on the fair value option.

(2) Nonperforming loans at December 31, 2012 and net charge-off ratios for 2012 include the impact of new regulatory guidance on loans discharged in Chapter 7 bankruptcy. For more information,

see Consumer Portfolio Credit Risk Management on page 76 and Table 21.

(3) These vintages of loans account for 60 percent and 63 percent of nonperforming residential mortgage loans at December 31, 2012 and 2011, and 72 percent and 73 percent of residential mortgage

net charge-offs in 2012 and 2011.

(4) Net charge-off ratios are calculated as net charge-offs divided by average outstanding loans excluding loans accounted for under the fair value option.

n/a = not applicable

Nonperforming residential mortgage loans decreased $1.2

billion in 2012 as paydowns, charge-offs and returns to performing

status, outpaced new inflows. In addition, nonperforming

residential mortgage loan balances at December 31, 2012

included $572 million due to new regulatory guidance related to

loans less than 60 days past due that were discharged in Chapter

7 bankruptcy. At December 31, 2012, borrowers were current on

contractual payments with respect to $3.5 billion, or 24 percent

of nonperforming residential mortgage loans, and $8.7 billion, or

59 percent of nonperforming residential mortgage loans were

180 days or more past due and had been written down to the

estimated fair value of the collateral less estimated costs to sell.

Accruing loans past due 30 days or more decreased $868 million

in 2012.

Net charge-offs decreased $779 million to $3.1 billion in 2012,

or 2.02 percent of total average residential mortgage loans,

compared to $3.8 billion, or 2.27 percent, for 2011. This decrease

in net charge-offs for 2012 was primarily driven by decreased write-