Bank of America 2012 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

68 Bank of America 2012

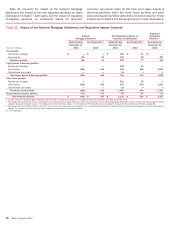

Table 14 presents the capital composition at December 31, 2012 and 2011.

Table 14 Capital Composition

December 31

(Dollars in millions) 2012 2011

Total common shareholders’ equity $ 218,188 $ 211,704

Goodwill (69,976) (69,967)

Nonqualifying intangible assets (includes core deposit intangibles, affinity relationships, customer relationships and other intangibles) (4,994)(5,848)

Net unrealized gains on AFS debt and marketable equity securities and net losses on derivatives recorded in accumulated OCI,

net-of-tax (2,036)682

Unamortized net periodic benefit costs recorded in accumulated OCI, net-of-tax 4,456 4,391

Fair value adjustment related to structured liabilities (1) 4,084 944

Disallowed deferred tax asset (17,940) (16,799)

Other 1,621 1,583

Total Tier 1 common capital 133,403 126,690

Qualifying preferred stock 15,851 15,479

Trust preferred securities 6,207 16,737

Noncontrolling interests —326

Total Tier 1 capital 155,461 159,232

Long-term debt qualifying as Tier 2 capital 24,287 38,165

Allowance for loan and lease losses 24,179 33,783

Reserve for unfunded lending commitments 513 714

Allowance for loan and lease losses exceeding 1.25 percent of risk-weighted assets (9,459)(18,159)

45 percent of the pre-tax net unrealized gains on AFS marketable equity securities 329 1

Other 1,370 1,365

Total capital $ 196,680 $ 215,101

(1) Represents loss on structured liabilities, net-of-tax, that is excluded from Tier 1 common capital, Tier 1 capital and Total capital for regulatory capital purposes.

Regulatory Capital Changes

At December 31, 2012, we measured and reported our capital

ratios and related information in accordance with Basel 1. We

manage regulatory capital to adhere to internal capital guidelines

and regulatory standards of capital adequacy based on our current

understanding of the rules and the application of such rules to

our business as currently conducted. See Capital Management on

page 66 for additional information.

In June 2012, U.S. banking regulators issued the Market Risk

Final Rule that amends the Basel 1 Market Risk rules (Market Risk

Final Rule) effective January 1, 2013. The Market Risk Final Rule

introduces new measures of market risk, a charge related to a

stressed Value-at-Risk (VaR), an incremental risk charge and a

comprehensive risk measure, as well as other technical

modifications. As of December 31, 2012, the estimated impact

of the Market Risk Final Rule would have been a 68 bps decrease

in the Tier 1 common capital ratio to 10.38 percent as a result of

a $78.8 billion increase in risk-weighted assets for market risk

exposures.

The regulatory capital rules continue to expand and evolve. In

December 2007, U.S. banking regulators published final Basel 2

rules (Basel 2). We measure and report our capital ratios and

related information under Basel 2 on a confidential basis to U.S.

banking regulators during the required parallel period, during which

we provide the U.S. banking regulators both Basel 1 and Basel 2

related information in parallel. The parallel period will continue

until we receive regulatory approval to exit parallel reporting and

subsequently begin publicly reporting our Basel 2 regulatory

capital results and related disclosures.

In June 2012, U.S. banking regulators issued three notices of

proposed rulemaking (collectively, the Basel 3 NPRs) which, if

adopted as proposed, would materially change Tier 1 common,

Tier 1 and Total capital calculations. The Basel 3 NPRs also

introduce new minimum capital ratios and buffer requirements,

expand and modify the calculation of risk-weighted assets for credit

and market risk (the Advanced Approach) and introduce a

Standardized Approach for the calculation of risk-weighted assets,

which would replace Basel 1 and provide a floor for minimum,

adequately capitalized regulatory capital requirements under the

Prompt Corrective Action framework. The Prompt Corrective Action

framework establishes categories of capitalization, including “well-

capitalized,” based on regulatory ratio requirements. U.S. banking

regulators are required to take certain mandatory actions

depending on the category of capitalization. No mandatory actions

are required under the Prompt Corrective Action framework for

“well-capitalized” banking entities.

Under the Basel 3 NPRs, Trust Securities will be phased out

of Tier 1 capital in equal annual installments over a three-year

transition period. Many of the changes to the composition of

regulatory capital are subject to a transition period where the

impact is recognized in 20 percent increments, phased in

incrementally each year over a five-year period. The phase-in period

for the new minimum capital requirements and related buffers is

proposed to occur from the effective date of the Basel 3 NPRs

through 2019. On November 9, 2012, U.S. banking regulators

announced that they did not expect any of the Basel 3 NPRs to

become effective January 1, 2013. Final rules for Basel 3 have

not yet been issued by U.S. banking regulators.

Under the Basel 3 NPRs we will be subject to the Advanced

Approach for measuring risk-weighted assets (Basel 3 Advanced

Approach) when finalized and implemented. The Basel 3 Advanced

Approach also requires approval by the U.S. regulatory agencies

of analytical models used as part of capital measurement. If these

models are not approved, it would likely lead to an increase in our

risk-weighted assets, which in some cases could be significant.

The Basel 3 Advanced Approach, if adopted as proposed, is

expected to substantially increase our capital requirements as

discussed below.