Bank of America 2012 Annual Report Download - page 215

Download and view the complete annual report

Please find page 215 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 213

GSEs and the corresponding estimated range of possible loss is

primarily driven by the FNMA Settlement and also considers, and

is necessarily dependent on, and limited by, a number of factors,

including the Corporation’s experience related to actual defaults,

projected future defaults, historical loss experience, estimated

home prices and other economic conditions. The methodology also

considers such factors as the number of payments made by the

borrower prior to default as well as certain other assumptions and

judgmental factors. See the Estimated Range of Possible Loss

section below for a discussion of the representations and

warranties liability and the corresponding estimated range of

possible loss.

The Corporation’s estimate of the non-GSE representations and

warranties liability and the corresponding range of possible loss

considers, among other things, repurchase experience based on

the BNY Mellon Settlement, adjusted to reflect differences

between the Covered Trusts and the remainder of the population

of private-label securitizations, and assumes that the conditions

to the BNY Mellon Settlement will be met. Since the non-GSE

securitization trusts that were included in the BNY Mellon

Settlement differ from those that were not included in the BNY

Mellon Settlement, the Corporation adjusted the repurchase

experience implied in the settlement in order to determine the

estimated non-GSE representations and warranties liability and

the corresponding range of possible loss. The judgmental

adjustments made include consideration of the differences in the

mix of products in the subject securitizations, loan originator,

likelihood of claims expected, the differences in the number of

payments that the borrower has made prior to default and the

sponsor of the securitizations. Where relevant, the Corporation

also takes into account more recent experience, such as increased

claims and other facts and circumstances, such as bulk

settlements, as the Corporation believes appropriate.

Additional factors that impact the non-GSE representations and

warranties liability and the portion of the estimated range of

possible loss corresponding to non-GSE representations and

warranties exposures include: (1) contractual material adverse

effect requirements; (2) the representations and warranties

provided; and (3) the requirement to meet certain presentation

thresholds. The first factor is based on the Corporation’s belief

that a non-GSE contractual liability to repurchase a loan generally

arises only if the counterparties prove there is a breach of

representations and warranties that materially and adversely

affects the interest of the investor or all investors, or of the

monoline insurer or other financial guarantor (as applicable), in a

securitization trust and, accordingly, the Corporation believes that

the repurchase claimants must prove that the alleged

representations and warranties breach was the cause of the loss.

The second factor is based on the differences in the types of

representations and warranties given in non-GSE securitizations

from those provided to the GSEs. The Corporation believes the

non-GSE securitizations’ representations and warranties are less

rigorous and actionable than the explicit provisions of comparable

agreements with the GSEs without regard to any variations that

may have arisen as a result of dealings with the GSEs. The third

factor is related to certain presentation thresholds that need to

be met in order for any repurchase claim to be asserted on the

initiative of investors under the non-GSE agreements. A

securitization trustee may investigate or demand repurchase on

its own action, and most agreements contain a presentation

threshold, for example 25 percent of the voting rights per trust,

that allows investors to declare a servicing event of default under

certain circumstances or to request certain action, such as

requesting loan files, that the trustee may choose to accept and

follow, exempt from liability, provided the trustee is acting in good

faith. If there is an uncured servicing event of default and the

trustee fails to bring suit during a 60-day period, then, under most

agreements, investors may file suit. In addition to this, most

agreements also allow investors to direct the securitization trustee

to investigate loan files or demand the repurchase of loans if

security holders hold a specified percentage, for example, 25

percent, of the voting rights of each tranche of the outstanding

securities. Although the Corporation continues to believe that

presentation thresholds are a factor in the determination of

probable loss, given the BNY Mellon Settlement, the estimated

range of possible loss assumes that the presentation threshold

can be met for all of the non-GSE securitization transactions. The

population of private-label securitizations included in the BNY

Mellon Settlement encompasses almost all legacy Countrywide

first-lien private-label securitizations including loans originated

principally between 2004 and 2008. For the remainder of the

population of private-label securitizations, other claimants have

come forward and the Corporation believes it is probable that other

claimants in certain types of securitizations may continue to come

forward with claims that meet the requirements of the terms of

the securitizations.

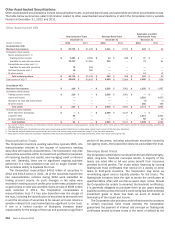

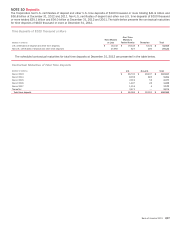

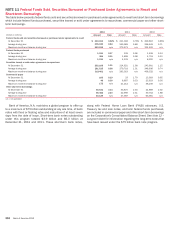

The table below presents a rollforward of the liability for

representations and warranties and corporate guarantees.

Representations and Warranties and Corporate

Guarantees

(Dollars in millions) 2012 2011

Liability for representations and warranties and

corporate guarantees, January 1 $ 15,858 $ 5,438

Additions for new sales 28 20

Charge-offs (804) (5,191)

Provision 3,939 15,591

Liability for representations and warranties and

corporate guarantees, December 31 $ 19,021 $ 15,858

For 2012, the provision for representations and warranties and

corporate guarantees was $3.9 billion compared to $15.6 billion

for 2011. The provision in 2012 included $2.5 billion in provision

related to the FNMA Settlement and $500 million for obligations

to FNMA related to MI rescissions. The provision in 2011 included

$8.6 billion in provision and other expenses related to the BNY

Mellon Settlement to resolve nearly all of the legacy Countrywide-

issued first-lien non-GSE repurchase exposures, and $7.0 billion

in provision related to other non-GSE, and to a lesser extent, GSE

exposures.

Estimated Range of Possible Loss

The representations and warranties liability represents the

Corporation’s best estimate of probable incurred losses as of

December 31, 2012. However, it is reasonably possible that future

representations and warranties losses may occur in excess of the

amounts recorded for these exposures. In addition, the

Corporation has not recorded any representations and warranties

liability for certain potential private-label securitization and whole-

loan exposures where it has little to no claim experience. The

Corporation currently estimates that the range of possible loss for

representations and warranties exposures could be up to $4 billion