Bank of America 2012 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 187

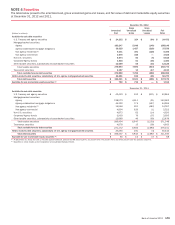

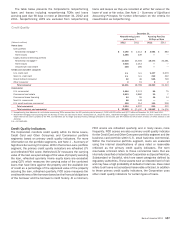

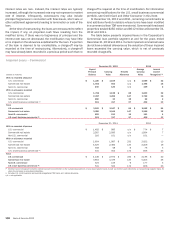

The table below presents the Corporation’s nonperforming

loans and leases including nonperforming TDRs and loans

accruing past due 90 days or more at December 31, 2012 and

2011. Nonperforming LHFS are excluded from nonperforming

loans and leases as they are recorded at either fair value or the

lower of cost or fair value. See Note 1 – Summary of Significant

Accounting Principles for further information on the criteria for

classification as nonperforming.

Credit Quality

December 31

Nonperforming Loans

and Leases (1)

Accruing Past Due

90 Days or More

(Dollars in millions) 2012 2011 2012 2011

Home loans

Core portfolio

Residential mortgage (2) $ 3,190 $ 2,414 $ 3,984 $ 883

Home equity 1,265 439 ——

Legacy Assets & Servicing portfolio

Residential mortgage (2) 11,618 13,556 18,173 20,281

Home equity 3,016 2,014 ——

Discontinued real estate 248 290 ——

Credit card and other consumer

U.S. credit card n/a n/a 1,437 2,070

Non-U.S. credit card n/a n/a 212 342

Direct/Indirect consumer 92 40 545 746

Other consumer 215 22

Total consumer 19,431 18,768 24,353 24,324

Commercial

U.S. commercial 1,484 2,174 65 75

Commercial real estate 1,513 3,880 29 7

Commercial lease financing 44 26 15 14

Non-U.S. commercial 68 143 ——

U.S. small business commercial 115 114 120 216

Total commercial 3,224 6,337 229 312

Total consumer and commercial $ 22,655 $ 25,105 $24,582 $ 24,636

(1) Nonperforming loan balances do not include nonaccruing TDRs removed from the PCI portfolio prior to January 1, 2010 of $521 million and $477 million at December 31, 2012 and 2011.

(2) Residential mortgage loans accruing past due 90 days or more are fully-insured loans. At December 31, 2012 and 2011, residential mortgage includes $17.8 billion and $17.0 billion of loans on

which interest has been curtailed by the FHA, and therefore are no longer accruing interest, although principal is still insured, and $4.4 billion and $4.2 billion of loans on which interest is still

accruing.

n/a = not applicable

Credit Quality Indicators

The Corporation monitors credit quality within its Home Loans,

Credit Card and Other Consumer, and Commercial portfolio

segments based on primary credit quality indicators. For more

information on the portfolio segments, see Note 1 – Summary of

Significant Accounting Principles. Within the Home Loans portfolio

segment, the primary credit quality indicators are refreshed LTV

and refreshed FICO score. Refreshed LTV measures the carrying

value of the loan as a percentage of the value of property securing

the loan, refreshed quarterly. Home equity loans are evaluated

using CLTV which measures the carrying value of the combined

loans that have liens against the property and the available line

of credit as a percentage of the appraised value of the property

securing the loan, refreshed quarterly. FICO score measures the

creditworthiness of the borrower based on the financial obligations

of the borrower and the borrower’s credit history. At a minimum,

FICO scores are refreshed quarterly, and in many cases, more

frequently. FICO scores are also a primary credit quality indicator

for the Credit Card and Other Consumer portfolio segment and the

business card portfolio within U.S. small business commercial.

Within the Commercial portfolio segment, loans are evaluated

using the internal classifications of pass rated or reservable

criticized as the primary credit quality indicators. The term

reservable criticized refers to those commercial loans that are

internally classified or listed by the Corporation as Special Mention,

Substandard or Doubtful, which are asset categories defined by

regulatory authorities. These assets have an elevated level of risk

and may have a high probability of default or total loss. Pass rated

refers to all loans not considered reservable criticized. In addition

to these primary credit quality indicators, the Corporation uses

other credit quality indicators for certain types of loans.