Bank of America 2012 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

86 Bank of America 2012

Countrywide Purchased Credit-impaired Loan Portfolio

Loans acquired with evidence of credit quality deterioration since

origination and for which it is probable at purchase that we will be

unable to collect all contractually required payments are accounted

for under the accounting guidance for PCI loans, which addresses

accounting for differences between contractual and expected cash

flows to be collected from the purchaser’s initial investment in

loans if those differences are attributable, at least in part, to credit

quality. Evidence of credit quality deterioration as of the acquisition

date may include statistics such as past due status, refreshed

FICO scores and refreshed LTVs. PCI loans are recorded at fair

value upon acquisition and the applicable accounting guidance

prohibits carrying over or recording a valuation allowance in the

initial accounting.

PCI loans that have similar risk characteristics, primarily credit

risk, collateral type and interest rate risk, are pooled and accounted

for as a single asset with a single composite interest rate and an

aggregate expectation of cash flows. Once a pool is assembled,

it is considered as if it were one loan for purposes of applying the

accounting guidance for PCI loans. An individual loan is removed

from a PCI loan pool if it is sold, foreclosed, forgiven or the

expectation of any future proceeds is remote. When a loan is

removed from a PCI loan pool and the foreclosure or recovery value

of the loan is less than the loan’s carrying value, the difference is

first applied against the PCI pool’s nonaccretable difference. If the

nonaccretable difference has been fully utilized, only then is the

PCI pool’s basis applicable to that loan written-off against its

valuation reserve; however, the integrity of the pool is maintained

and it continues to be accounted for as if it were one loan.

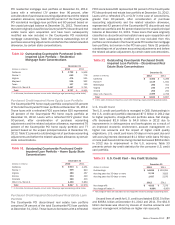

Table 29 presents the unpaid principal balance, carrying value,

related valuation allowance and the net carrying value as a

percentage of the unpaid principal balance for the Countrywide

PCI loan portfolio.

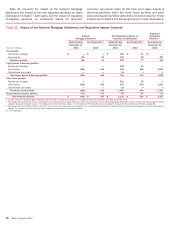

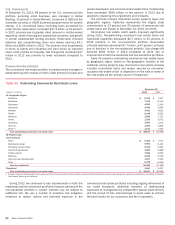

Table 29 Countrywide Purchased Credit-impaired Loan Portfolio

December 31, 2012

(Dollars in millions)

Unpaid

Principal

Balance

Carrying

Value

Related

Valuation

Allowance

Carrying

Value Net of

Valuation

Allowance

Percent of

Unpaid

Principal

Balance

Residential mortgage $ 8,898 $ 8,737 $ 1,061 $ 7,676 86.27%

Home equity 8,324 8,547 2,428 6,119 73.51

Discontinued real estate 9,281 8,834 2,047 6,787 73.13

Total Countrywide purchased credit-impaired loan portfolio $ 26,503 $ 26,118 $ 5,536 $ 20,582 77.66

December 31, 2011

Residential mortgage $ 10,426 $ 9,966 $ 1,111 $ 8,855 84.93%

Home equity 12,516 11,978 5,129 6,849 54.72

Discontinued real estate 11,891 9,857 2,219 7,638 64.23

Total Countrywide purchased credit-impaired loan portfolio $ 34,833 $ 31,801 $ 8,459 $ 23,342 67.01

The total Countrywide PCI unpaid principal balance decreased

$8.3 billion, or 24 percent, in 2012 to $26.5 billion at

December 31, 2012 primarily driven by liquidations, paydowns and

payoffs. In addition, the decline includes loans with an unpaid

principal balance of $2.9 billion within the home equity portfolio

that were forgiven in connection with the National Mortgage

Settlement of which 92 percent were 180 days or more past due.

For more information on the National Mortgage Settlement, see

Consumer Portfolio Credit Risk Management on page 76.

Of the unpaid principal balance of $26.5 billion at

December 31, 2012, $7.3 billion was 180 days or more past due,

including $6.5 billion of first-lien and $795 million of home equity

loans. Of the $19.2 billion that was less than 180 days past due,

$17.1 billion, or 89 percent of the total unpaid principal balance,

was current based on the contractual terms while $1.3 billion, or

seven percent, was in early stage delinquency. The home equity

180 days or more past due balances declined $2.9 billion, or 79

percent, during 2012, due primarily to the loans forgiven as

discussed above.

During 2012, we recorded a provision benefit of $103 million

for the Countrywide PCI loan portfolio including a benefit of $88

million for discontinued real estate, a benefit of $27 million for

residential mortgage loans and a provision expense of $12 million

for home equity. This compared to a total provision of $2.1 billion

in 2011. The decline in provision in 2012 was primarily driven by

an improvement in our home price outlook.

The Countrywide PCI allowance declined $2.9 billion during

2012 driven by a $2.7 billion reduction in the Countrywide PCI

home equity allowance primarily as a result of liquidations including

the forgiveness of $2.5 billion of fully reserved home equity loans

in connection with the National Mortgage Settlement. For further

information on the Countrywide PCI loan portfolio, see Note 5 –

Outstanding Loans and Leases to the Consolidated Financial

Statements.

In January 2013, in connection with the FNMA Settlement, we

repurchased for $6.6 billion certain residential mortgage loans

that had previously been sold to FNMA, which we have valued at

less than the purchase price. The majority of these loans were

classified as PCI loans when they were recorded in January 2013.

For additional information, see Off-Balance Sheet Arrangements

and Contractual Obligations – Representations and Warranties on

page 50.

Additional information on the Countrywide PCI residential

mortgage, home equity and discontinued real estate loan

portfolios is provided in the following sections.

Purchased Credit-impaired Residential Mortgage Loan

Portfolio

The Countrywide PCI residential mortgage loan portfolio comprised

33 percent of the total Countrywide PCI loan portfolio at

December 31, 2012. Those loans to borrowers with a refreshed

FICO score below 620 represented 37 percent of the Countrywide