Bank of America 2012 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

72 Bank of America 2012

eligible assets was approximately $194 billion and $189 billion

at December 31, 2012 and 2011. We have established

operational procedures to enable us to borrow against these

assets, including regularly monitoring our total pool of eligible

loans and securities collateral. Eligibility is defined by guidelines

outlined by the FHLBs and the Federal Reserve and is subject to

change at their discretion. Due to regulatory restrictions, liquidity

generated by the bank subsidiaries can only be used to fund

obligations within the bank subsidiaries and can only be

transferred to the parent company or nonbank subsidiaries with

prior regulatory approval.

Global Excess Liquidity Sources available to our broker/dealer

subsidiaries totaled $22 billion and $31 billion at December 31,

2012 and 2011. Our broker/dealers also held other

unencumbered investment-grade securities and equities that we

believe could also be used to generate additional liquidity. Liquidity

held in a broker/dealer subsidiary is available to meet the

obligations of that entity and can only be transferred to the parent

company or to any other subsidiary with prior regulatory approval

due to regulatory restrictions and minimum requirements.

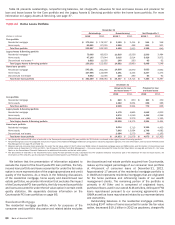

Table 18 presents the composition of Global Excess Liquidity

Sources at December 31, 2012 and 2011.

Table 18 Global Excess Liquidity Sources Composition

December 31

(Dollars in billions) 2012 2011

Cash on deposit $ 65 $ 79

U.S. treasuries 21 48

U.S. agency securities and mortgage-backed securities 271 228

Non-U.S. government and supranational securities 15 23

Total global excess liquidity sources $ 372 $ 378

Time to Required Funding and Stress Modeling

We use a variety of metrics to determine the appropriate amounts

of excess liquidity to maintain at the parent company and our bank

and broker/dealer subsidiaries. One metric we use to evaluate the

appropriate level of excess liquidity at the parent company is “Time

to Required Funding.” This debt coverage measure indicates the

number of months that the parent company can continue to meet

its unsecured contractual obligations as they come due using only

its Global Excess Liquidity Sources without issuing any new debt

or accessing any additional liquidity sources. We define unsecured

contractual obligations for purposes of this metric as maturities

of senior or subordinated debt issued or guaranteed by Bank of

America Corporation or Merrill Lynch. These include certain

unsecured debt instruments, primarily structured liabilities, which

we may be required to settle for cash prior to maturity. The

Corporation has established a target for Time to Required Funding

of 21 months. Our Time to Required Funding was 33 months at

December 31, 2012. For purposes of calculating Time to Required

Funding at December 31, 2012, we have also included in the

amount of unsecured contractual obligations the $8.6 billion

liability related to the BNY Mellon Settlement. The BNY Mellon

Settlement is subject to final court approval and certain other

conditions, and the timing of payment is not certain.

We utilize liquidity stress models to assist us in determining

the appropriate amounts of excess liquidity to maintain at the

parent company and our bank and broker/dealer subsidiaries.

These models are risk sensitive and have become increasingly

important in analyzing our potential contractual and contingent

cash outflows beyond those outflows considered in the Time to

Required Funding analysis. We evaluate the liquidity requirements

under a range of scenarios with varying levels of severity and time

horizons. The scenarios we consider and utilize incorporate

market-wide and Corporation-specific events, including potential

credit rating downgrades for the parent company and our

subsidiaries, and are based on historical experience, regulatory

guidance, and both expected and unexpected future events.

The types of potential contractual and contingent cash outflows

we consider in our scenarios may include, but are not limited to,

upcoming contractual maturities of unsecured debt and reductions

in new debt issuance; diminished access to secured financing

markets; potential deposit withdrawals and reduced rollover of

maturing term deposits by customers; increased draws on loan

commitments, liquidity facilities and letters of credit, including

Variable Rate Demand Notes; additional collateral that

counterparties could call if our credit ratings were downgraded

further; collateral, margin and subsidiary capital requirements

arising from losses; and potential liquidity required to maintain

businesses and finance customer activities. Changes in certain

market factors, including, but not limited to, credit rating

downgrades, could negatively impact potential contractual and

contingent outflows and the related financial instruments, and in

some cases these impacts could be material to our financial

results.

We consider all sources of funds that we could access during

each stress scenario and focus particularly on matching available

sources with corresponding liquidity requirements by legal entity.

We also use the stress modeling results to manage our asset-

liability profile and establish limits and guidelines on certain

funding sources and businesses.

Basel 3 Liquidity Standards

In December 2010, the Basel Committee proposed two measures

of liquidity risk which are considered part of Basel 3. The first

proposed liquidity measure is the Liquidity Coverage Ratio (LCR),

which is calculated as the amount of a financial institution’s

unencumbered, high-quality, liquid assets relative to the net cash

outflows the institution could encounter under a significant 30-day

stress scenario. The Basel Committee announced in January 2013

that an initial minimum LCR requirement of 60 percent will be

implemented in January 2015, and will thereafter increase in 10

percent annual increments through January 2019. The second

proposed liquidity measure is the Net Stable Funding Ratio (NSFR),

which measures the amount of longer-term, stable sources of

funding employed by a financial institution relative to the liquidity

profiles of the assets funded and the potential for contingent calls

on funding liquidity arising from off-balance sheet commitments

and obligations over a one-year period. The Basel Committee is

currently reviewing the NSFR requirement and intends for the

requirement to be implemented by January 2018, following an

observation period that is currently underway. We continue to

monitor the development and the potential impact of these

proposals and assuming adoption by U.S. banking regulators, we

expect to meet the final standards within the regulatory timelines.