Bank of America 2010 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

$81 million primarily driven by a decrease in securities in South Africa, offset by

increases in loans in the United Arab Emirates and South Africa, and securities

in Bahrain. At December 31, 2010 and 2009, three percent and five percent of

the emerging markets exposure was in Central and Eastern Europe.

Certain European countries, including Greece, Ireland, Italy, Portugal and

Spain, are currently experiencing varying degrees of financial stress. These

countries have had certain credit ratings lowered by ratings services during

2010. Risks from the debt crisis in Europe could result in a disruption of the

financial markets which could have a detrimental impact on the global eco-

nomic recovery and sovereign and non-sovereign debt in these countries. The

table below shows our direct sovereign and non-sovereign exposures, exclud-

ing consumer credit card exposure, in these countries at December 31, 2010.

The total exposure to these countries was $15.8 billion at December 31,

2010 compared to $25.5 billion at December 31, 2009. The $9.7 billion

decrease since December 31, 2009 was driven primarily by the sale or

maturity of sovereign and non-sovereign securities in all countries.

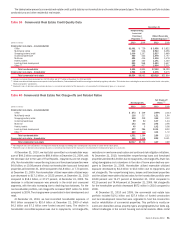

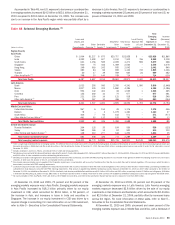

Table 49 Selected European Countries

(Dollars in millions)

Loans and

Leases, and

Loan

Commitments

Other

Financing

(1)

Derivative

Assets

(2)

Securities/

Other

Investments

(3)

Total Cross-

border

Exposure

(4)

Local

Country

Exposure Net

of Local

Liabilities

(5)

Total Non-

U.S.

Exposure at

December 31,

2010

Credit Default

Protection

(6)

Greece

Sovereign $ – $ – $ – $ 103 $ 103 $ –

$103

$(23)

Non-sovereign 260 2 43 69 374 –

374

–

Total Greece

$ 260 $ 2 $ 43 $ 172 $ 477 $ –

$477

$(23)

Ireland

Sovereign $ 7 $ 326 $ 22 $ 52 $ 407 $ –

$407

$–

Non-sovereign 1,641 524 152 267 2,584 –

2,584

(15)

Total Ireland

$1,648 $ 850 $ 174 $ 319 $ 2,991 $ –

$2,991

$(15)

Italy

Sovereign $ – $ – $1,247 $ 21 $ 1,268 $ 1

$1,269

$(1,136)

Non-sovereign 967 639 560 1,310 3,476 1,792

5,268

(67)

Total Italy

$ 967 $ 639 $1,807 $1,331 $ 4,744 $1,793

$6,537

$(1,203)

Portugal

Sovereign $ – $ – $ 36 $ – $ 36 $ –

$36

$(19)

Non-sovereign 65 55 26 344 490 –

490

–

Total Portugal

$ 65 $ 55 $ 62 $ 344 $ 526 $ –

$526

$(19)

Spain

Sovereign $ 25 $ – $ 36 $ – $ 61 $ 40

$101

$(57)

Non-sovereign 1,028 40 382 1,872 3,322 1,835

5,157

(7)

Total Spain

$1,053 $ 40 $ 418 $1,872 $ 3,383 $1,875

$5,258

$(64)

Total

Sovereign $ 32 $ 326 $1,341 $ 176 $ 1,875 $ 41

$1,916

$(1,235)

Non-sovereign 3,961 1,260 1,163 3,862 10,246 3,627

13,873

(89)

Total selected European exposure

$3,993 $1,586 $2,504 $4,038 $12,121 $3,668

$15,789

$(1,324)

(1)

Includes acceptances, due froms, SBLCs, commercial letters of credit and formal guarantees.

(2)

Derivative assets are carried at fair value and have been reduced by the amount of cash collateral applied of $2.9 billion at December 31, 2010. At December 31, 2010, there was $41 million of other marketable securities

collateralizing derivative assets.

(3)

Generally, cross-border resale agreements are presented based on the domicile of the counterparty, consistent with FFIEC reporting requirements. Cross-border resale agreements where the underlying securities are U.S. Treasury

securities, in which case the domicile is the U.S., are excluded from this presentation.

(4)

Cross-border exposure includes amounts payable to the Corporation by borrowers or counterparties with a country of residence other than the one in which the credit is booked, regardless of the currency in which the claim is

denominated, consistent with FFIEC reporting requirements.

(5)

Local country exposure includes amounts payable to the Corporation by borrowers with a country of residence in which the credit is booked regardless of the currency in which the claim is denominated. Local funding or liabilities are

subtracted from local exposures consistent with FFIEC reporting requirements. Of the $838 million applied for exposure reduction, $459 million was in Italy, $208 million in Ireland, $137 million in Spain and $34 million in Greece.

(6)

Represents net notional credit default protection purchased to hedge counterparty risk.

Provision for Credit Losses

The provision for credit losses decreased $20.1 billion to $28.4 billion for 2010

compared to 2009. The provision for credit losses for the consumer portfolio

decreased $11.4 billion to $25.4 billion for 2010 compared to 2009 reflecting

lower delinquencies and decreasing bankruptcies in the consumer credit card

and unsecured consumer lending portfolios resulting from an improving eco-

nomic outlook. Also contributing to the improvement were lower reserve ad-

ditions in consumer real estate due to improving portfolio trends. The addition

to reserves in the consumer PCI loan portfolios reflected further reductions in

expected principal cash flows of $2.2 billion for 2010 compared to $3.5 billion

a year earlier. Consumer net charge-offs of $29.4 billion for 2010 were

$4.2 billion higher than the prior year due to the impact of the adoption of new

consolidation guidance resulting in the consolidation of certain securitized

loan balances in our consumer credit card and home equity portfolios, offset

by benefits from economic improvement during the year which impacted all

consumer portfolios.

The provision for credit losses for the commercial portfolio, including the

provision for unfunded lending commitments, decreased $8.7 billion to

$3.0 billion for 2010 compared to 2009 due to improved borrower credit

profiles, stabilization of appraisal values in the commercial real estate port-

folio and lower delinquencies and bankruptcies in the small business port-

folio. These same factors resulted in a decrease in commercial net charge-

offs of $3.5 billion to $5.0 billion in 2010 compared to 2009.

100 Bank of America 2010