Bank of America 2010 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

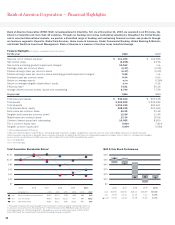

Financial Highlights

Net Interest Income

Net interest income on a FTE basis increased $4.3 billion to $52.7 billion for

2010 compared to 2009. The increase was due to the impact of deposit

pricing and the adoption of new consolidation guidance which contributed

$10.5 billion to net interest income in 2010. The increase was partially offset

by lower commercial and consumer loan levels, the sale of First Republic in

2010 and lower rates on the core assets and trading assets and liabilities,

including derivatives exposure. The net interest yield on a FTE basis increased

13 basis points (bps) to 2.78 percent for 2010 compared to 2009 due to

these same factors.

Noninterest Income

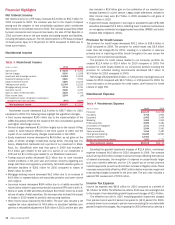

Table 3 Noninterest Income

(Dollars in millions)

2010 2009

Card income

$8,108

$8,353

Service charges

9,390

11,038

Investment and brokerage services

11,622

11,919

Investment banking income

5,520

5,551

Equity investment income

5,260

10,014

Trading account profits

10,054

12,235

Mortgage banking income

2,734

8,791

Insurance income

2,066

2,760

Gains on sales of debt securities

2,526

4,723

Other income (loss)

2,384

(14)

Net impairment losses recognized in earnings on

available-for-sale debt securities

(967)

(2,836)

Total noninterest income

$58,697

$72,534

Noninterest income decreased $13.8 billion to $58.7 billion for 2010

compared to 2009. The following items highlight the significant changes.

• Card income decreased $245 million due to the implementation of the

CARD Act partially offset by the impact of the new consolidation guidance

and higher interchange income.

• Service charges decreased $1.6 billion largely due to the impact of Reg-

ulation E, which became effective in the third quarter of 2010 and the

impact of our overdraft policy changes implemented in late 2009.

• Equity investment income decreased by $4.8 billion, as net gains on the

sales of certain strategic investments during 2010, including Itaú Uni-

banco, MasterCard, Santander and a portion of our investment in Black-

Rock, Inc. (BlackRock) were less than gains in 2009 that included a

$7.3 billion gain related to the sale of a portion of our investment in

CCB and the $1.1 billion gain related to our BlackRock investment.

• Trading account profits decreased $2.2 billion due to more favorable

market conditions in the prior year and investor concerns regarding sov-

ereign debt fears and regulatory uncertainty. Net credit valuation gains on

derivative liabilities of $262 million for 2010 compared to losses of

$662 million for 2009.

• Mortgage banking income decreased $6.1 billion due to an increase of

$4.9 billion in representations and warranties provision and lower volume

and margins.

• Insurance income decreased $694 million due to a liability recorded for

future claims related to payment protection insurance (PPI) sold in the U.K.

• Gains on sales of debt securities decreased $2.2 billion driven by a lower

volume of sales of debt securities. The decrease also included the impact

of losses in 2010 related to portfolio restructuring activities.

• Other income (loss) improved by $2.4 billion. The prior year included a net

negative fair value adjustment of $4.9 billion on structured liabilities com-

pared to a net positive adjustment of $18 million in 2010, and the prior year

also included a $3.8 billion gain on the contribution of our merchant pro-

cessing business to a joint venture. Legacy asset write-downs included in

other income (loss) were $1.7 billion in 2009 compared to net gains of

$256 million in 2010.

• Impairment losses recognized in earnings on available-for-sale (AFS) debt

securities decreased $1.9 billion reflecting lower impairment write-downs

on non-agency residential mortgage-backed securities (RMBS) and collat-

eralized debt obligations (CDOs).

Provision for Credit Losses

The provision for credit losses decreased $20.1 billion to $28.4 billion in

2010 compared to 2009. The provision for credit losses was $5.9 billion

lower than net charge-offs for 2010, resulting in a reduction in reserves

primarily due to improving portfolio trends throughout the year across the

consumer and commercial businesses.

The provision for credit losses related to our consumer portfolio de-

creased $11.4 billion to $25.4 billion for 2010 compared to 2009. The

provision for credit losses related to our commercial portfolio including the

provision for unfunded lending commitments decreased $8.7 billion to

$3.0 billion for 2010 compared to 2009.

Net charge-offs totaled $34.3 billion, or 3.60 percent of average loans and

leases for 2010 compared with $33.7 billion, or 3.58 percent for 2009. For

more information on the provision for credit losses, see Provision for Credit

Losses on page 100.

Noninterest Expense

Table 4 Noninterest Expense

(Dollars in millions)

2010 2009

Personnel

$35,149

$31,528

Occupancy

4,716

4,906

Equipment

2,452

2,455

Marketing

1,963

1,933

Professional fees

2,695

2,281

Amortization of intangibles

1,731

1,978

Data processing

2,544

2,500

Telecommunications

1,416

1,420

Other general operating

16,222

14,991

Goodwill impairment

12,400

–

Merger and restructuring charges

1,820

2,721

Total noninterest expense

$83,108

$66,713

Excluding the goodwill impairment charges of $12.4 billion, noninterest

expense increased $4.0 billion for 2010 compared to 2009. The increase

was driven by a $3.6 billion increase in personnel costs reflecting the build out

of several businesses, the recognition of expense on proportionally larger

prior year incentive deferrals and the U.K. payroll tax on certain year-end

incentive payments, as well as a $1.6 billion increase in litigation costs. These

increases were partially offset by a $901 million decline in pre-tax merger and

restructuring charges compared to the prior year. The prior year included a

special FDIC assessment of $724 million.

Income Tax Expense

Income tax expense was $915 million for 2010 compared to a benefit of

$1.9 billion for 2009. The effective tax rate for 2010 was not meaningful due

to the impact of non-deductible goodwill impairment charges of $12.4 billion.

The effective tax rate for 2010 excluding goodwill impairment charges

from pre-tax income was 8.3 percent compared to (44.0) percent for 2009,

primarily driven by an increase in pre-tax income excluding the non-deductible

goodwill impairment charges. Also impacting the 2010 effective tax rate was a

32 Bank of America 2010