Bank of America 2010 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

Market Risk Management

Market risk is the risk that values of assets and liabilities or revenues will be

adversely affected by changes in market conditions such as market move-

ments. This risk is inherent in the financial instruments associated with our

operations and/or activities including loans, deposits, securities, short-term

borrowings, long-term debt, trading account assets and liabilities, and deriv-

atives. Market-sensitive assets and liabilities are generated through loans

and deposits associated with our traditional banking business, customer and

other trading operations, the ALM process, credit risk mitigation activities and

mortgage banking activities. In the event of market volatility, factors such as

underlying market movements and liquidity have an impact on the results of

the Corporation.

Our traditional banking loan and deposit products are nontrading positions

and are generally reported at amortized cost for assets or the amount owed

for liabilities (historical cost). However, these positions are still subject to

changes in economic value based on varying market conditions, primarily

changes in the levels of interest rates. The risk of adverse changes in the

economic value of our nontrading positions is managed through our ALM

activities. We have elected to account for certain assets and liabilities under

the fair value option. For further information on the fair value of certain

financial assets and liabilities, see Note 22 – Fair Value Measurements to the

Consolidated Financial Statements.

Our trading positions are reported at fair value with changes currently

reflected in income. Trading positions are subject to various risk factors, which

include exposures to interest rates and foreign exchange rates, as well as

mortgage, equity, commodity, issuer and market liquidity risk factors. We seek

to mitigate these risk exposures by using techniques that encompass a

variety of financial instruments in both the cash and derivatives markets.

The following discusses the key risk components along with respective risk

mitigation techniques.

Interest Rate Risk

Interest rate risk represents exposures to instruments whose values vary with

the level or volatility of interest rates. These instruments include, but are not

limited to, loans, debt securities, certain trading-related assets and liabilities,

deposits, borrowings and derivative instruments. Hedging instruments used

to mitigate these risks include derivatives such as options, futures, forwards

and swaps.

Foreign Exchange Risk

Foreign exchange risk represents exposures to changes in the values of

current holdings and future cash flows denominated in other currencies. The

types of instruments exposed to this risk include investments in non-U.S. sub-

sidiaries, foreign currency-denominated loans and securities, future cash

flows in foreign currencies arising from foreign exchange transactions, foreign

currency-denominated debt and various foreign exchange derivative instru-

ments whose values fluctuate with changes in the level or volatility of currency

exchange rates or non-U.S. interest rates. Hedging instruments used to

mitigate this risk include foreign exchange options, currency swaps, futures,

forwards, foreign currency-denominated debt and deposits.

Mortgage Risk

Mortgage risk represents exposures to changes in the value of mortgage-

related instruments. The values of these instruments are sensitive to pre-

payment rates, mortgage rates, agency debt ratings, default, market liquidity,

other interest rates, government participation and interest rate volatility. Our

exposure to these instruments takes several forms. First, we trade and

engage in market-making activities in a variety of mortgage securities includ-

ing whole loans, pass-through certificates, commercial mortgages, and col-

lateralized mortgage obligations (CMOs) including CDOs using mortgages as

underlying collateral. Second, we originate a variety of MBS which involves the

accumulation of mortgage-related loans in anticipation of eventual securiti-

zation. Third, we may hold positions in mortgage securities and residential

mortgage loans as part of the ALM portfolio. Fourth, we create MSRs as part

of our mortgage origination activities. See Note 1 – Summary of Significant

Accounting Principles and Note 25 – Mortgage Servicing Rights to the Con-

solidated Financial Statements for additional information on MSRs. Hedging

instruments used to mitigate this risk include foreign exchange options,

currency swaps, futures, forwards and foreign currency-denominated debt.

Equity Market Risk

Equity market risk represents exposures to securities that represent an

ownership interest in a corporation in the form of domestic and foreign

common stock or other equity-linked instruments. Instruments that would

lead to this exposure include, but are not limited to, the following: common

stock, exchange-traded funds, American Depositary Receipts, convertible

bonds, listed equity options (puts and calls), over-the-counter equity options,

equity total return swaps, equity index futures and other equity derivative

products. Hedging instruments used to mitigate this risk include options,

futures, swaps, convertible bonds and cash positions.

Commodity Risk

Commodity risk represents exposures to instruments traded in the petroleum,

natural gas, power and metals markets. These instruments consist primarily

of futures, forwards, swaps and options. Hedging instruments used to mit-

igate this risk include options, futures and swaps in the same or similar

commodity product, as well as cash positions.

Issuer Credit Risk

Issuer credit risk represents exposures to changes in the creditworthiness of

individual issuers or groups of issuers. Our portfolio is exposed to issuer

credit risk where the value of an asset may be adversely impacted by changes

in the levels of credit spreads, by credit migration or by defaults. Hedging

instruments used to mitigate this risk include bonds, credit default swaps and

other credit fixed-income instruments.

Market Liquidity Risk

Market liquidity risk represents the risk that the level of expected market

activity changes dramatically and, in certain cases, may even cease to exist.

This exposes us to the risk that we will not be able to transact business and

execute trades in an orderly manner which may impact our results. This

impact could further be exacerbated if expected hedging or pricing correla-

tions are compromised by the disproportionate demand or lack of demand for

certain instruments. We utilize various risk mitigating techniques as dis-

cussed in more detail below.

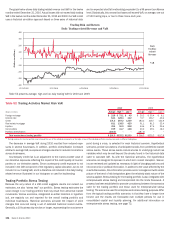

Trading Risk Management

Trading-related revenues represent the amount earned from trading positions,

including market-based net interest income, in a diverse range of financial

instruments and markets. Trading account assets and liabilities and deriva-

tive positions are reported at fair value. For more information on fair value,

see Note 22 – Fair Value Measurements to the Consolidated Financial State-

ments. Trading-related revenues can be volatile and are largely driven by

general market conditions and customer demand. Trading-related revenues

are dependent on the volume and type of transactions, the level of risk

assumed, and the volatility of price and rate movements at any given time

within the ever-changing market environment.

The Global Markets Risk Committee (GRC), chaired by the Global Markets

Risk Executive, has been designated by ALMRC as the primary governance

104 Bank of America 2010