Bank of America 2010 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

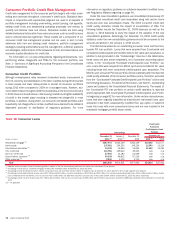

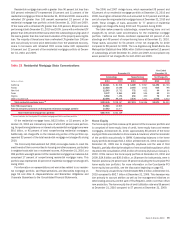

|

|

decrease in adjusted quarterly average total assets. The reduction in risk-

weighted assets and adjusted quarterly average total assets is consistent

with our continued efforts to reduce non-core assets and legacy loan

portfolios.

The FIA Card Services, N.A. Tier 1 capital ratio increased 9 bps to

15.30 percent and Total capital ratio decreased 7 bps to 16.94 percent

compared to December 31, 2009. The increase in Tier 1 capital ratio was due

to a decrease in risk-weighted assets of $22.3 billion. The decrease in the

Total capital ratio was due to a reduction in Tier 2 capital resulting from a

$390 million decrease in qualifying term subordinated debt combined with a

net increase in the allowance for credit losses limitation of $269 million. The

Tier 1 leverage ratio decreased to 13.21 percent at December 31, 2010 from

23.09 percent at December 31, 2009 due to a $68.9 billion increase in

adjusted quarterly average total assets. The increase in adjusted quarterly

average total assets was the result of the adoption of new consolidation

guidance.

Broker/Dealer Regulatory Capital

Bank of America’s principal U.S. broker/dealer subsidiaries are Merrill Lynch,

Pierce, Fenner & Smith (MLPF&S) and Merrill Lynch Professional Clearing Corp

(MLPCC). MLPCC is a subsidiary of MLPF&S and provides clearing and

settlement services. Both entities are subject to the net capital requirements

of SEC Rule 15c3-1. Both entities are also registered as futures commission

merchants and subject to the Commodity Futures Trading Commission (CFTC)

Regulation 1.17.

MLPF&S has elected to compute the minimum capital requirement in

accordance with the “Alternative Net Capital Requirement” as permitted by

SEC Rule 15c3-1. At December 31, 2010, MLPF&S’s regulatory net capital as

defined by Rule 15c3-1 was $9.8 billion and exceeded the minimum require-

ment of $736 million by $9.1 billion. MLPCC’s net capital of $2.3 billion

exceeded the minimum requirement by $2.1 billion.

In accordance with the Alternative Net Capital Requirements, MLPF&S is

required to maintain tentative net capital in excess of $1 billion and notify the

SEC in the event its tentative net capital is less than $5 billion. At Decem-

ber 31, 2010, MLPF&S had tentative net capital in excess of the minimum and

notification requirements.

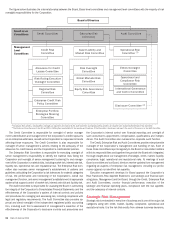

Economic Capital

Our economic capital measurement process provides a risk-based measure-

ment of the capital required for unexpected credit, market and operational

losses over a one-year time horizon at a 99.97 percent confidence level,

consistent with a “AA” credit rating. Economic capital is allocated to each

business unit based upon its risk positions and contribution to enterprise risk,

and is used for capital adequacy, performance measurement and risk man-

agement purposes. The strategic planning process utilizes economic capital

with the goal of allocating risk appropriately and measuring returns consis-

tently across all businesses and activities.

Credit Risk Capital

Economic capital for credit risk captures two types of risks: default risk, which

represents the loss of principal due to outright default or the borrower’s

inability to repay an obligation in full, and migration risk, which represents

potential loss in market value due to credit deterioration over the one-year

capital time horizon. Credit risk is assessed and modeled for all on- and off-

balance sheet credit exposures within sub-categories for commercial, retail,

counterparty and investment securities. The economic capital methodology

captures dimensions such as concentration and country risk and originated

securitizations. The economic capital methodology is based on the probability

of default, loss given default, exposure at default and maturity for each credit

exposure, and the portfolio correlations across exposures. See page 75 for

more information on Credit Risk Management.

Market Risk Capital

Market risk reflects the potential loss in the value of financial instruments or

portfolios due to movements in foreign exchange and interest rates, credit

spreads, and security and commodity prices. Bank of America’s primary

market risk exposures are in its trading portfolio, equity investments, MSRs

and the interest rate exposure of its core balance sheet. Economic capital is

determined by utilizing the same models the Corporation used to manage

these risks including, for example, Value-at-Risk, simulation, stress testing

and scenario analysis. See page 104 for additional information on Market

Risk Management.

Operational Risk Capital

We calculate operational risk capital at the business unit level using actuarial-

based models and historical loss data. We supplement the calculations with

scenario analysis and risk control assessments. See Operational Risk Man-

agement beginning on page 110 for more information.

Capital Actions

The Corporation held a special meeting of stockholders on February 23, 2010

at which we obtained stockholder approval of an amendment to our amended

and restated certificate of incorporation to increase the number of authorized

shares of our common stock from 10.0 billion to 11.3 billion. On February 24,

2010, approximately 1.3 billion shares of common stock were issued through

the conversion of CES into common stock. For more information regarding this

conversion, see Preferred Stock Issuances and Exchanges on page 71.

In January 2009, we issued approximately 1.4 billion shares of common

stock in connection with the acquisition of Merrill Lynch. For additional

information regarding the Merrill Lynch acquisition, see Note 2 – Merger

and Restructuring Activity to the Consolidated Financial Statements. In addi-

tion, in 2009, we issued warrants to purchase approximately 199.1 million

shares of common stock in connection with preferred stock issuances to the

U.S. government. For more information, see Preferred Stock Issuances and

Exchanges on page 71. In 2009, we issued 1.3 billion shares of common

stock at an average price of $10.77 per share through an at-the-market

issuance program resulting in gross proceeds of approximately $13.5 billion.

In addition, during 2010 and 2009, we issued approximately 98.6 million and

7.4 million shares under employee stock plans.

Troubled Asset Relief Program – Related Asset Sales

We received notification from the Federal Reserve confirming that we fulfilled

our commitment to increase equity by $3.0 billion through asset sales to be

completed by December 31, 2010. The commitment was made in connection

with the approval we received in December 2009 to repurchase the preferred

stock that we issued as a result of our participation in the Troubled Asset

Relief Program (TARP).

There were no common shares repurchased in 2010 except for shares

acquired under equity incentive plans, as discussed in Item 5. Market for

Registrant’s Common Equity, Related Stockholder Matters and Issuer Pur-

chases of Equity Securities of this Annual Report on Form 10-K. Currently,

there is no existing Board authorized share repurchase program. For more

information regarding our common share issuances, see Note 15 – Share-

holders’ Equity to the Consolidated Financial Statements.

We currently intend to modestly increase the common stock dividends in

the second half of 2011 subject to approval by the Federal Reserve.

70 Bank of America 2010