Bank of America 2010 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

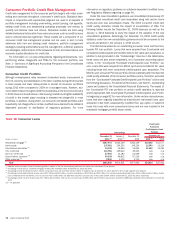

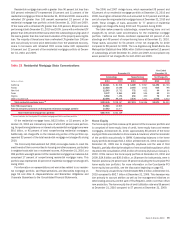

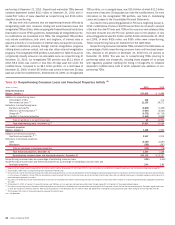

Countrywide Purchased Credit-impaired Loan Portfolio

Loans acquired with evidence of credit quality deterioration since origination

and for which it is probable at purchase that we will be unable to collect all

contractually required payments are accounted for under the accounting

guidance for PCI loans, which addresses accounting for differences between

contractual and expected cash flows to be collected from the purchaser’s

initial investment in loans if those differences are attributable, at least in part,

to credit quality. Evidence of credit quality deterioration as of the acquisition

date may include statistics such as past due status, refreshed FICO scores

and refreshed LTVs. PCI loans are recorded at fair value upon acquisition and

the applicable accounting guidance prohibits carrying over or recording val-

uation allowances in the initial accounting. The Merrill Lynch PCI consumer

loan portfolio did not materially alter the reported credit quality statistics of

the consumer portfolios. As such, the Merrill Lynch consumer PCI loans are

excluded from the following discussion and credit statistics.

Acquired loans from Countrywide that were considered credit-impaired

were written down to fair value at the acquisition date. The following table

presents the unpaid principal balance, carrying value, allowance for loan and

lease losses and the net carrying value as a percentage of the unpaid principal

balance for the Countrywide PCI loan portfolio at December 31, 2010.

Table 25 Countrywide Purchased Credit-impaired Loan Portfolio

(Dollars in millions)

Unpaid

Principal

Balance

Carrying

Value

Related

Allowance

Carrying

Value Net of

Allowance

%of

Unpaid Principal

Balance

December 31, 2010

Residential mortgage $11,481 $10,592 $ 229 $10,363 90.26%

Home equity 15,072 12,590 4,514 8,076 53.58

Discontinued real estate 14,893 11,652 1,591 10,061 67.56

Total Countrywide purchased credit-impaired loan portfolio $41,446 $34,834 $6,334 $28,500 68.76%

Of the unpaid principal balance at December 31, 2010, $15.5 billion was

180 days or more past due, including $10.9 billion of first-lien and $4.6 billion

of home equity. Of the $25.9 billion that is less than 180 days past due,

$21.5 billion, or 83 percent of the total unpaid principal balance, was current

based on the contractual terms while $2.2 billion, or eight percent, was in

early stage delinquency. During 2010, we recorded $2.3 billion of provision for

credit losses on PCI loans which was comprised mainly of $1.4 billion for

home equity and $689 million for discontinued real estate loans compared to

a total provision for PCI loans of $3.3 billion in 2009. Provision expense in

2010 was driven primarily by a slower pace of expected recovery in home

prices, the result of a deteriorating view on defaults on more seasoned loans

in the portfolio and a reassessment of modification and short sale benefits as

we gain more experience with troubled borrowers. The Countrywide PCI

allowance for loan losses increased $2.5 billion from December 31, 2009

to $6.3 billion at December 31, 2010 as a result of the increase in the

provision for credit losses and the reclassification of a portion of nonaccret-

able difference to the allowance. For further information on the PCI loan

portfolio, see Note 6 – Outstanding Loans and Leases to the Consolidated

Financial Statements.

Additional information on the Countrywide PCI residential mortgage, home

equity and discontinued real estate loan portfolios follows.

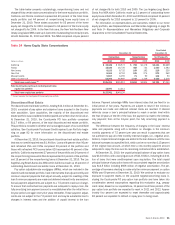

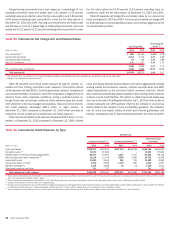

Purchased Credit-impaired Residential Mortgage Loan Portfolio

The Countrywide PCI residential mortgage loan portfolio outstandings were

$10.6 billion at December 31, 2010 and comprised 30 percent of the total

Countrywide PCI loan portfolio. Those loans to borrowers with a refreshed FICO

score below 620 represented 38 percent of the Countrywide PCI residential

mortgage loan portfolio at December 31, 2010. Refreshed LTVs greater than

90 percent represented 68 percent of the PCI residential mortgage loan

portfolio after consideration of purchase accounting adjustments and 82 per-

cent based on the unpaid principal balance at December 31, 2010. Those

loans that were originally classified as discontinued real estate loans upon

acquisition and have been subsequently modified are now included in the

residential mortgage outstandings. The table below presents outstandings net

of purchase accounting adjustments, by certain state concentrations.

Table 26 Outstanding Countrywide Purchased

Credit-impaired Loan Portfolio – Residential Mortgage State

Concentrations

(Dollars in millions)

2010 2009

December 31

California

$5,882

$6,142

Florida

779

843

Virginia

579

617

Maryland

271

278

Texas

164

166

Other U.S./Non-U.S.

2,917

3,031

Total Countrywide purchased credit-impaired residential

mortgage loan portfolio

$10,592

$11,077

82 Bank of America 2010