Bank of America 2010 Annual Report Download - page 182

Download and view the complete annual report

Please find page 182 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

Home Equity Mortgages

The Corporation maintains interests in home equity securitization trusts to

which the Corporation transferred home equity loans. These retained inter-

ests include senior and subordinate securities and residual interests. In

addition, the Corporation may be obligated to provide subordinate funding to

the trusts during a rapid amortization event. The Corporation also services the

loans in the trusts. Except as described below and in Note 9 – Representa-

tions and Warranties Obligations and Corporate Guarantees, the Corporation

does not provide guarantees or recourse to the securitization trusts other

than standard representations and warranties. There were no securitizations

of home equity loans during 2010 and 2009. Collections reinvested in

revolving period securitizations were $21 million and $177 million during

2010 and 2009. Cash flows received on residual interests were $12 million

and $35 million in 2010 and 2009.

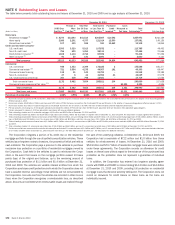

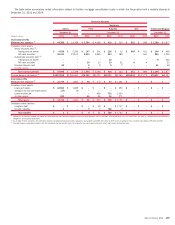

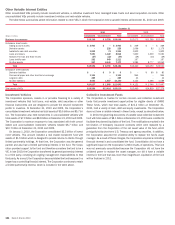

The table below summarizes select information related to home equity

loan securitization trusts in which the Corporation held a variable interest at

December 31, 2010 and 2009.

(Dollars in millions)

Consolidated

VIEs

Retained

Interests in

Unconsolidated

VIEs Total

Retained

Interests in

Unconsolidated

VIEs

2010 2009

December 31

Maximum loss exposure

(1)

$3,192 $ 9,132 $12,324

$13,947

On-balance sheet assets

Trading account assets

(2, 3)

$ – $209$209

$16

Available-for-sale debt securities

(3, 4)

–3535

147

Loans and leases

3,529 – 3,529

–

Allowance for loan and lease losses

(337) – (337)

–

Total

$3,192 $ 244 $ 3,436

$163

On-balance sheet liabilities

Long-term debt

$3,635 $ – $ 3,635

$–

All other liabilities

23 – 23

–

Total

$3,658 $ – $ 3,658

$–

Principal balance outstanding

$3,529 $20,095 $23,624

$31,869

(1)

For unconsolidated VIEs, the maximum loss exposure includes outstanding trust certificates issued by trusts in rapid amortization, net of recorded reserves, and excludes the liability for representations and warranties and corporate

guarantees.

(2)

At December 31, 2010 and 2009, $204 million and $15 million of the debt securities classified as trading account assets were senior securities and $5 million and $1 million were subordinate securities.

(3)

As a holder of these securities, the Corporation receives scheduled principal and interest payments. During 2010 and 2009, there were no OTTI losses recorded on those securities classified as AFS debt securities.

(4)

At December 31, 2010 and 2009, $35 million and $47 million represent subordinate debt securities held. At December 31, 2009, $100 million are residual interests classified as AFS debt securities.

Under the terms of the Corporation’s home equity loan securitizations,

advances are made to borrowers when they draw on their lines of credit and

the Corporation is reimbursed for those advances from the cash flows in the

securitization. During the revolving period of the securitization, this reimburse-

ment normally occurs within a short period after the advance. However, when

certain securitization transactions have begun a rapid amortization period,

reimbursement of the Corporation’s advance occurs only after other parties in

the securitization have received all of the cash flows to which they are entitled.

This has the effect of extending the time period for which the Corporation’s

advances are outstanding. In addition, if loan losses requiring draws on

monoline insurers’ policies, which protect the bondholders in the securitiza-

tion, exceed a specified threshold or duration, the Corporation may not receive

reimbursement for all of the funds advanced to borrowers, as the senior

bondholders and the monoline insurers have priority for repayment.

Substantially all of the home equity loan securitizations for which the

Corporation has an obligation to provide subordinate advances have entered

rapid amortization. The Corporation evaluates each of these securitizations

for potential losses due to non-recoverable advances by estimating the

amount and timing of future losses on the underlying loans, the excess

spread available to cover such losses and potential cash flow shortfalls during

rapid amortization. A maximum funding obligation attributable to rapid

amortization cannot be calculated as a home equity borrower has the ability

to pay down and re-draw balances. At December 31, 2010 and 2009, home

equity loan securitization transactions in rapid amortization, including both

consolidated and unconsolidated trusts, had $12.5 billion and $14.1 billion

of trust certificates outstanding. This amount is significantly greater than the

amount the Corporation expects to fund. At December 31, 2010, the remain-

ing $93 million of trust certificates outstanding related to these types of

securitization transactions are expected to enter rapid amortization during the

next 12 months. The charges that will ultimately be recorded as a result of the

rapid amortization events depend on the performance of the loans, the

amount of subsequent draws and the timing of related cash flows. At De-

cember 31, 2010 and 2009, the reserve for losses on expected future draw

obligations on the home equity loan securitizations in or expected to be in

rapid amortization was $131 million and $178 million.

The Corporation has consumer MSRs from the sale or securitization of

home equity loans. The Corporation recorded $79 million and $128 million of

servicing fee income related to home equity securitizations during 2010 and

2009. The Corporation repurchased $17 million and $31 million of loans from

home equity securitization trusts in order to perform modifications or pursu-

ant to clean up calls during 2010 and 2009.

180 Bank of America 2010