Bank of America 2010 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

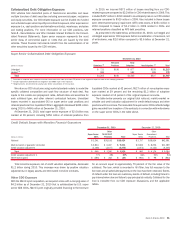

second-lien mortgages. Of these balances, $45.8 billion of the first-lien

mortgages and $48.5 billion of the second-lien mortgages have paid off

and $32.9 billion of the first-lien mortgages and $14.5 billion of the second-

lien mortgages have defaulted or are severely delinquent and are considered

principal at-risk at December 31, 2010. At least 25 payments have been

made on approximately 52 percent of the loans included in principal at-risk. Of

the first-lien mortgages sold, $41.0 billion, or 39 percent, were sold as whole

loans to other institutions which subsequently included these loans with

those of other originators in private-label securitization transactions in which

the monolines typically insured one or more securities. Through December 31,

2010, we have received $5.6 billion of representations and warranties claims

related to the monoline-insured transactions. Of these repurchase claims,

$799 million have been resolved, with losses of $631 million. The majority of

these resolved claims related to second-lien mortgages and $678 million of

these claims were resolved through repurchase or indemnification while

$121 million were rescinded by the investor or paid in full. At December 31,

2010, the unpaid principal balance of loans related to unresolved monoline

repurchase requests was $4.8 billion, including $3.0 billion that have been

reviewed where it is believed a valid defect has not been identified which would

constitute an actionable breach of representations and warranties and

$1.8 billion that are in the process of review. We have had limited experience

with most of the monoline insurers in the repurchase process, which has

constrained our ability to resolve the open claims with such counterparties.

Also, certain monoline insurers have instituted litigation against legacy Coun-

trywide and Bank of America, which limits our relationship with such monoline

insurers and ability to enter into constructive dialogue to resolve the open

claims. It is not possible at this time to reasonably estimate future repurchase

obligations with respect to those monolines with whom we have limited

repurchase experience and, therefore, no liability has been recorded in

connection with these monolines, other than a liability for repurchase re-

quests that are in the process of review and repurchase requests where we

have determined that there are valid loan defects. However, certain other

monoline insurers have engaged with us in a consistent repurchase process

and we have used that experience to record a liability related to existing and

projected future claims from such counterparties.

Whole Loan Sales and Private-label Securitizations

Legacy entities, and to a lesser extent Bank of America, sold loans in whole loan

sales or via private-label securitizations with a total principal balance of

$777.1 billion originated from 2004 through 2008, which are included in Table

11, of which $384.0 billion have been paid off and $169.0 billion have defaulted

or are severely delinquent and are considered principal at-risk at December 31,

2010. At least 25 payments have been made on approximately 60 percent of

the loans included in principal at-risk. We have received approximately $8.1 bil-

lion of representations and warranties claims from whole loan investors and

private-label securitization investors related to these vintages, including $5.6 bil-

lion from whole loan investors, $800 million from one private-label securitization

counterparty which were submitted prior to 2008 and $1.7 billion in recent

demands from private-label securitization investors. Private-label securitization

investors generally do not have the contractual right to demand repurchase of

loans directly. The inclusion of the $1.7 billion in recent demands from private-

label securitization investors does not mean that we believe these claims have

satisfied the contractual thresholds required for these investors to direct the

securitization trustee to take action or are otherwise procedurally or substan-

tively valid. Additionally, certain private-label securitizations are insured by the

monolines, which are not reflected in these figures regarding whole loan sales

and private-label securitizations.

We have resolved $5.2 billion of the claims received from whole loan

investors and private-label securitization investors with losses of $1.1 billion.

Approximately $2.1 billion of these claims were resolved through repurchase

or indemnification and $3.1 billion were rescinded by the investor. Claims

outstanding related to these vintages totaled $2.9 billion at December 31,

2010, $1.1 billion of which we have reviewed and declined to repurchase

based on an assessment of whether a material breach exists, $91 million of

which are in the process of review and $1.7 billion of which are demands from

private-label securitization investors received in the fourth quarter of 2010.

The majority of the claims that we have received so far are from whole loan

investors and until we have meaningful repurchase experiences with counter-

parties other than whole loan investors, it is not possible to determine

whether a loss related to our private-label securitizations has occurred or

is probable. However, certain whole loan investors have engaged with us in a

consistent repurchase process and we have used that experience to record a

liability related to existing and future claims from such counterparties.

On October 18, 2010, Countrywide Home Loans Servicing, LP (which

changed its name to BAC Home Loans Servicing, LP), a wholly-owned sub-

sidiary of the Corporation, received a letter, in its capacity as servicer on 115

private-label securitizations which was subsequently extended to 225 securi-

tizations. The letter asserted breaches of certain servicing obligations, in-

cluding an alleged failure to provide notice of breaches of representations and

warranties with respect to mortgage loans included in the transactions. See

Recent Events – Private-label Residential Mortgage-backed Securities Mat-

ters on page 39 for additional information.

See Complex Accounting Estimates – Representations and Warranties on

page 116 for information related to our estimated liability for representations

and warranties and corporate guarantees related to mortgage-related securi-

tizations. For additional information regarding representations and warranties

and disputes involving monolines, whole loan sales and private-label securi-

tizations, see Note 9 – Representations and Warranties Obligations and

Corporate Guarantees and Note 14 – Commitments and Contingencies to

the Consolidated Financial Statements.

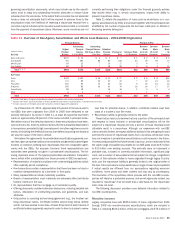

Regulatory Matters

Refer to Item 1A. Risk Factors of this Annual Report on Form 10-K for

additional information on recent or proposed legislative and regulatory initi-

atives as well as other risks to which we are exposed, including among others,

enhanced regulatory scrutiny or potential legal liability as a result of the recent

financial crisis.

Financial Reform Act

On July 21, 2010, the Financial Reform Act was signed into law. The Financial

Reform Act enacts sweeping financial regulatory reform and will alter the way

in which we conduct certain businesses, increase our costs and reduce our

revenues.

Background

The Financial Reform Act mandates that the Federal Reserve limit debit card

interchange fees. Provisions in the legislation also ban banking organizations

from engaging in proprietary trading and restrict their sponsorship of, or

investing in, hedge funds and private equity funds, subject to limited excep-

tions. The Financial Reform Act increases regulation of the derivative markets

through measures that broaden the derivative instruments subject to regu-

lation and requires clearing and exchange trading as well as imposing addi-

tional capital and margin requirements for derivative market participants. The

Financial Reform Act also changes the methodology for calculating deposit

insurance assessments from the amount of an insured depository institu-

tion’s domestic deposits to its total assets minus tangible capital; provides

for resolution authority to establish a process to unwind large systemically

important financial companies; creates a new regulatory body to set require-

ments regarding the terms and conditions of consumer financial products and

expands the role of state regulators in enforcing consumer protection

60 Bank of America 2010