Bank of America 2010 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

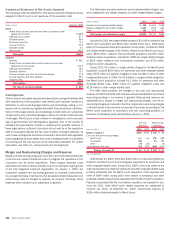

derivatives that serve as economic hedges of mortgage servicing rights

(MSRs), interest rate lock commitments (IRLCs) and first mortgage loans

held-for-sale (LHFS) that are originated by the Corporation are recorded in

mortgage banking income. Changes in the fair value of derivatives that serve

as asset and liability management (ALM) economic hedges are recorded in

other income (loss). Credit derivatives used by the Corporation as economic

hedges do not qualify as accounting hedges despite being effective economic

hedges, and changes in the fair value of these derivatives are included in

other income (loss).

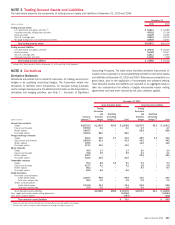

Derivatives Used For Hedge Accounting Purposes

(Accounting Hedges)

For accounting hedges, the Corporation formally documents at inception all

relationships between hedging instruments and hedged items, as well as the

risk management objectives and strategies for undertaking various account-

ing hedges. Additionally, the Corporation primarily uses regression analysis at

the inception of a hedge and for each reporting period thereafter to assess

whether the derivative used in a hedging transaction is expected to be and has

been highly effective in offsetting changes in the fair value or cash flows of a

hedged item. The Corporation discontinues hedge accounting when it is

determined that a derivative is not expected to be or has ceased to be highly

effective as a hedge, and then reflects changes in fair value of the derivative in

earnings after termination of the hedge relationship.

The Corporation uses its accounting hedges as either fair value hedges,

cash flow hedges or hedges of net investments in foreign operations. The

Corporation manages interest rate and foreign currency exchange rate sen-

sitivity predominantly through the use of derivatives. Fair value hedges are

used to protect against changes in the fair value of the Corporation’s assets

and liabilities that are attributable to interest rate or foreign exchange vola-

tility. Cash flow hedges are used primarily to minimize the variability in cash

flows of assets or liabilities, or forecasted transactions caused by interest

rate or foreign exchange fluctuations. For terminated cash flow hedges, the

maximum length of time over which forecasted transactions are hedged is

26 years, with a substantial portion of the hedged transactions being less

than 10 years. For open or future cash flow hedges, the maximum length of

time over which forecasted transactions are or will be hedged is less than

seven years.

Changes in the fair value of derivatives designated as fair value hedges

are recorded in earnings, together and in the same income statement line

item with changes in the fair value of the related hedged item. Changes in the

fair value of derivatives designated as cash flow hedges are recorded in

accumulated OCI and are reclassified into the line item in the income state-

ment in which the hedged item is recorded and in the same period the hedged

item affects earnings. Hedge ineffectiveness and gains and losses on the

excluded component of a derivative in assessing hedge effectiveness are

recorded in earnings in the same income statement line item. The Corporation

records changes in the fair value of derivatives used as hedges of the net

investment in foreign operations, to the extent effective, as a component of

accumulated OCI.

If a derivative instrument in a fair value hedge is terminated or the hedge

designation removed, the previous adjustments to the carrying amount of the

hedged asset or liability are subsequently accounted for in the same manner

as other components of the carrying amount of that asset or liability. For

interest-earning assets and interest-bearing liabilities, such adjustments are

amortized to earnings over the remaining life of the respective asset or

liability. If a derivative instrument in a cash flow hedge is terminated or the

hedge designation is removed, related amounts in accumulated OCI are

reclassified into earnings in the same period or periods during which the

hedged forecasted transaction affects earnings. If it is probable that a

forecasted transaction will not occur, any related amounts in accumulated

OCI are reclassified into earnings in that period.

Interest Rate Lock Commitments

The Corporation enters into IRLCs in connection with its mortgage banking

activities to fund residential mortgage loans at specified times in the future.

IRLCs that relate to the origination of mortgage loans that will be held for sale

are considered derivative instruments under applicable accounting guidance.

As such, these IRLCs are recorded at fair value with changes in fair value

recorded in mortgage banking income.

In estimating the fair value of an IRLC, the Corporation assigns a prob-

ability to the loan commitment based on an expectation that it will be exer-

cised and the loan will be funded. The fair value of the commitments is derived

from the fair value of related mortgage loans which is based on observable

market data and includes the expected net future cash flows related to

servicing of the loans. Changes to the fair value of IRLCs are recognized

based on interest rate changes, changes in the probability that the commit-

ment will be exercised and the passage of time. Changes from the expected

future cash flows related to the customer relationship are excluded from the

valuation of IRLCs.

Outstanding IRLCs expose the Corporation to the risk that the price of the

loans underlying the commitments might decline from inception of the rate

lock to funding of the loan. To protect against this risk, the Corporation utilizes

forward loan sales commitments and other derivative instruments, including

interest rate swaps and options, to economically hedge the risk of potential

changes in the value of the loans that would result from the commitments. The

changes in the fair value of these derivatives are recorded in mortgage

banking income.

Securities

Debt securities are recorded on the Consolidated Balance Sheet as of the

trade date and classified based on management’s intention on the date of

purchase. Debt securities which management has the intent and ability to

hold to maturity are classified as held-to-maturity (HTM) and reported at

amortized cost. Debt securities that are bought and held principally for the

purpose of resale in the near term are classified as trading and are carried at

fair value with unrealized gains and losses included in trading account profits

(losses). Other debt securities are classified as AFS and carried at fair value

with net unrealized gains and losses included in accumulated OCI on an after-

tax basis. In addition, credit-related notes, which include investments in

securities issued by CDOs, collateralized loan obligations (CLOs) and

credit-linked note vehicles, are classified as trading securities.

The Corporation regularly evaluates each AFS and HTM debt security

where the value has declined below amortized cost to assess whether the

decline in fair value is other-than-temporary. In determining whether an im-

pairment is other-than-temporary, the Corporation considers the severity and

duration of the decline in fair value, the length of time expected for recovery,

the financial condition of the issuer, and other qualitative factors, as well as

whether the Corporation either plans to sell the security or it is more-likely-

than-not that it will be required to sell the security before recovery of its

amortized cost. Beginning in 2009, under new accounting guidance for

impairments of debt securities that are deemed to be other-than-temporary,

the credit component of an other-than-temporary impairment (OTTI) loss is

recognized in earnings and the non-credit component is recognized in accu-

mulated OCI in situations where the Corporation does not intend to sell the

security and it is not more-likely-than-not that the Corporation will be required

to sell the security prior to recovery. Prior to January 1, 2009, unrealized

losses, both the credit and non-credit components, on AFS debt securities

that were deemed to be other-than-temporary were included in current-period

earnings. If there is an OTTI on any individual security classified as HTM, the

148 Bank of America 2010