Bank of America 2010 Annual Report Download - page 238

Download and view the complete annual report

Please find page 238 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

-

250

-

251

-

252

|

|

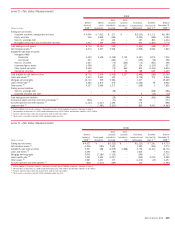

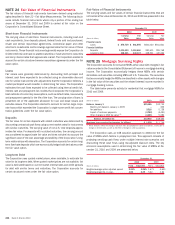

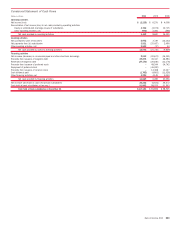

NOTE 24 Fair Value of Financial Instruments

The fair values of financial instruments have been derived using methodol-

ogies described in Note 22 – Fair Value Measurements. The following disclo-

sures include financial instruments where only a portion of the ending bal-

ances at December 31, 2010 and 2009 is carried at fair value on the

Corporation’s Consolidated Balance Sheet.

Short-term Financial Instruments

The carrying value of short-term financial instruments, including cash and

cash equivalents, time deposits placed, federal funds sold and purchased,

resale and certain repurchase agreements, commercial paper and other

short-term investments and borrowings approximates the fair value of these

instruments. These financial instruments generally expose the Corporation to

limited credit risk and have no stated maturities or have short-term maturities

and carry interest rates that approximate market. The Corporation elected to

account for certain structured reverse repurchase agreements under the fair

value option.

Loans

Fair values were generally determined by discounting both principal and

interest cash flows expected to be collected using an observable discount

rate for similar instruments with adjustments that the Corporation believes a

market participant would consider in determining fair value. The Corporation

estimates the cash flows expected to be collected using internal credit risk,

interest rate and prepayment risk models that incorporate the Corporation’s

best estimate of current key assumptions, such as default rates, loss severity

and prepayment speeds for the life of the loan. The carrying value of loans is

presented net of the applicable allowance for loan and lease losses and

excludes leases. The Corporation elected to account for certain large corpo-

rate loans which exceeded the Corporation’s single name credit risk concen-

tration guidelines under the fair value option.

Deposits

The fair value for certain deposits with stated maturities was determined by

discounting contractual cash flows using current market rates for instruments

with similar maturities. The carrying value of non-U.S. time deposits approx-

imates fair value. For deposits with no stated maturities, the carrying amount

was considered to approximate fair value and does not take into account the

significant value of the cost advantage and stability of the Corporation’s long-

term relationships with depositors. The Corporation accounts for certain long-

term fixed-rate deposits which are economically hedged with derivatives under

the fair value option.

Long-term Debt

The Corporation uses quoted market prices, when available, to estimate fair

value for its long-term debt. When quoted market prices are not available, fair

value is estimated based on current market interest rates and credit spreads

for debt with similar terms and maturities. The Corporation accounts for

certain structured notes under the fair value option.

Fair Value of Financial Instruments

The carrying values and fair values of certain financial instruments that are

not carried at fair value at December 31, 2010 and 2009 are presented in the

table below.

(Dollars in millions)

Carrying

Value

Fair

Value

Carrying

Value

Fair

Value

2010 2009

December 31

Financial assets

Loans

$ 876,739 $ 861,695

$841,020 $811,831

Financial liabilities

Deposits

1,010,430 1,010,460

991,611 991,768

Long-term debt

448,431 433,107

438,521 440,246

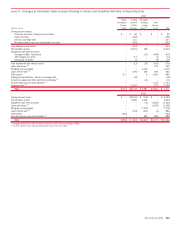

NOTE 25 Mortgage Servicing Rights

The Corporation accounts for consumer MSRs at fair value with changes in fair

value recorded in the Consolidated Statement of Income in mortgage banking

income. The Corporation economically hedges these MSRs with certain

derivatives and securities including MBS and U.S. Treasuries. The securities

that economically hedge the MSRs are classified in other assets with changes

in the fair value of the securities and the related interest income recorded in

mortgage banking income.

The table below presents activity for residential first mortgage MSRs for

2010 and 2009.

(Dollars in millions)

2010 2009

Balance, January 1

$19,465

$12,733

Merrill Lynch balance, January 1, 2009

–

209

Net additions

3,516

5,728

Impact of customer payments

(3,760)

(4,491)

Other changes in MSR fair value

(1)

(4,321)

5,286

Balance, December 31

$14,900

$19,465

Mortgage loans serviced for investors (in billions)

$1,628

$1,716

(1)

These amounts reflect the change in discount rates and prepayment speed assumptions, mostly due to

changes in interest rates, as well as the effect of changes in other assumptions.

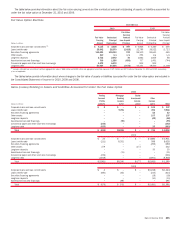

The Corporation uses an OAS valuation approach to determine the fair

value of MSRs which factors in prepayment risk. This approach consists of

projecting servicing cash flows under multiple interest rate scenarios and

discounting these cash flows using risk-adjusted discount rates. The key

economic assumptions used in determining the fair value of MSRs at De-

cember 31, 2010 and 2009 are presented below.

(Dollars in millions)

Fixed Adjustable Fixed Adjustable

2010 2009

December 31

Weighted-average option adjusted spread

2.21% 3.25%

1.67% 4.64%

Weighted-average life, in years

4.85 2.29

5.62 3.26

236 Bank of America 2010