Bank of America 2010 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

2010 Economic and Business Environment

The banking environment and markets in which we conduct our businesses

will continue to be strongly influenced by developments in the U.S. and global

economies, as well as the continued implementation and rulemaking from

recent financial reforms. The global economy continued to recover in 2010,

but growth was very uneven across countries and regions. Emerging nations,

led by China, India and Brazil, expanded rapidly, while the U.S., U.K., Europe

and Japan continued to grow modestly.

United States

In the U.S., the economy began to recover early in 2010, fueled by moderate

growth in consumption and inventory rebuilding, but slowed in late spring,

coincident with the intensification of Europe’s financial crisis. A slowdown in

consumption and domestic demand growth contributed to weak employment

gains and an unemployment rate that drifted close to 10 percent.

Year-over-year inflation measures receded below one percent and stock

market indices declined. Concerns about high unemployment and fears that

the U.S. might incur deflation led the Federal Reserve to adopt a second round

of quantitative easing that involved purchases of $600 billion of U.S. Treasury

securities scheduled to occur through June 2011. The announcement of this

policy led to lower interest rates. Bond yields rebounded in the second half of

2010 as the U.S. economy reaccelerated, driven by stronger consumer

spending, rapid growth of exports and business investment in equipment

and software. The strong holiday retail season provided healthy economic

momentum toward year end. Despite only moderate economic growth in

2010, corporate profits rose sharply, benefiting from strong productivity gains

and constraints on hiring and operating costs. Cautious business financial

practices resulted in a record-breaking $1.5 trillion in free cash flows at non-

financial businesses.

The housing market remained weak throughout 2010. Home sales were

soft, despite lower home prices and low interest rates. There were delays in

the foreclosure process on the large number of distressed mortgages and the

supply of unsold homes remained high. Based on available Home Price Index

(HPI) information, the mild improvement in home prices that occurred in the

second half of 2009 continued into early 2010. However, housing prices

renewed a downward trend in the second half of 2010, due in part to the

expiration of tax incentives for home buyers.

Credit quality of bank loans to businesses and households improved

significantly in 2010 and the continued economic recovery improved the

environment for bank lending. Bank commercial and industrial loans to busi-

nesses increased in the last few months of 2010, following their steep

recession-related declines, reflecting increasing loan demand relating to

stronger production, inventory building and capital spending. Rising dispos-

able personal income, household deleveraging and improving household

finances contributed to improving consumer credit quality.

Europe

In Europe, a financial crisis emerged in mid-2010, triggered by high budget

deficits and rising direct and contingent sovereign debt in Greece, Ireland,

Italy, Portugal and Spain that created concerns about the ability of these

European Union (EU) “peripheral nations” to continue to service their debt

obligations. These conditions impacted financial markets and resulted in high

and volatile bond yields on the sovereign debt of many EU nations. The

financial crisis and efforts by the European Commission, European Central

Bank (ECB) and International Monetary Fund (IMF) to negotiate a financial

suppor t package to financially challenged EU nations unsettled global finan-

cial markets and contributed to Euro exchange rate and interest rate volatility.

Economic performance of certain EU “core nations,” led by Germany, re-

mained healthy throughout 2010, while the economies of Greece, Ireland,

Italy, Portugal and Spain experienced recessionary conditions and slowing

growth in response to the financial crisis and the implementation of fiscal

austerity programs. Additionally, Spain and Ireland’s economies declined as a

result of material deterioration in their housing sectors. Uncertainty over the

outcome of the EU governments’ financial support programs and worries

about sovereign finances continued through year end. For information on our

exposure in Europe, see Non-U.S. Portfolio beginning on page 98 and

Note 28 – Performance by Geographical Area to the Consolidated Financial

Statements.

Asia

Asia, excluding Japan, continued to outperform all other regions in 2010 with

strong growth across most countries. China and India continued to lead the

region in terms of growth and China became the second largest economy in

the world after the U.S., eclipsing Japan. Growth across the region became

broader based with consumer demand, investment activity and exports all

performing well. Asia remained well positioned to withstand global shocks

because of record international reserves, current account surpluses and

reduced external leverage. Many Asian nations, including China, Taiwan,

South Korea, Thailand and Malaysia, are net external creditors, with China

and Japan among the largest holders of U.S. Treasury bonds. Bank balance

sheets have improved across most of the region and asset quality issues have

remained manageable. Among the key challenges faced by the region were

large capital inflows that placed appreciation pressures on most currencies

against the U.S. Dollar (USD), complicating monetary policy and adding to

excess liquidity pressures. Most countries in the region, including China,

India, South Korea, Thailand and Indonesia, began to withdraw fiscal stimulus

and tighten monetary policy with hikes in interest rates as growth gathered

momentum and as food and broader price inflation pressures began to

increase. Japan performed well early in the year, but the economy weakened

at the end of the year due to weakening consumer demand, and appreciation

of the yen that hurt export competitiveness. For information on our exposure

in Asia, see Non-U.S. Portfolio beginning on page 98 and Note 28 – Perfor-

mance by Geographical Area to the Consolidated Financial Statements.

Emerging Nations

In the emerging nations, inflation pressures began to mount and their central

banks raised interest rates or took steps to tighten monetary policy and slow

bank lending. Strong growth in emerging nations and their favorable economic

outlooks attracted capital from the industrialized nations. The excess global

liquidity generated by the accommodative monetary policies of the Federal

Reserve, Bank of Japan and other central banks also flowed into emerging

nations. These capital inflows put upward pressure on many emerging nation

currencies. As a result, some emerging nations, such as Brazil, experienced

strong currency appreciation. However, in other nations, that peg their cur-

rencies to the U.S. dollar, currency appreciation was muted causing inflation-

ary pressures and rapid real estate price appreciation. Global economic

momentum, along with the generally weak U.S. dollar and easing monetary

policies in several industrialized nations, contributed to rising prices for

industrial commodities in these emerging nations. Through year end, inflation

pressures in key emerging nations continued to mount. For more information

on our emerging nations exposure, see Table 48 on page 99.

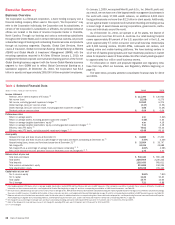

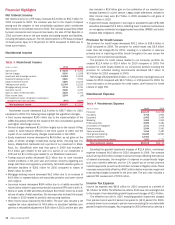

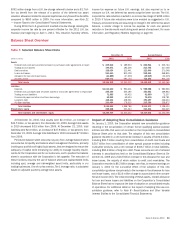

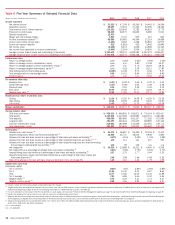

Performance Overview

In 2010, we reported a net loss of $2.2 billion compared to net income of

$6.3 billion in 2009. After preferred stock dividends and accretion of $1.4 bil-

lion in 2010 compared with $8.5 billion in 2009, net loss applicable to common

shareholders was $3.6 billion, or $0.37 per diluted common share, compared

to $2.2 billion, or $0.29 per diluted common share in 2009. Our 2010 results

reflected, among other things, $12.4 billion in goodwill impairment charges,

including non-cash, non-tax deductible goodwill impairment charges of

Bank of America 2010 29