Bank of America 2010 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

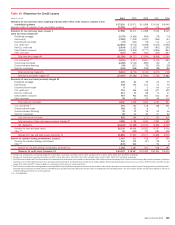

|

|

discount rate, terminal value, expected loss rates and expected new account

growth. We also updated our estimated cash flow valuation to reflect the

current strategic plan and other portfolio assumptions. Based on the results

of step one of the impairment test, we determined that the carrying amount of

Global Card Services, including goodwill, exceeded the fair value. The carrying

amount, fair value and goodwill of the reporting unit were $39.2 billion,

$25.9 billion and $22.3 billion, respectively. Accordingly, we performed step

two of the goodwill impairment test for this reporting unit. In step two, we

compared the implied fair value of the reporting unit’s goodwill with the

carrying amount of that goodwill. Under step two of the impairment test,

significant assumptions in measuring the fair value of the assets and liabil-

ities including discount rates, loss rates and interest rates were updated to

reflect the current economic conditions. Based on the results of this third-

quarter goodwill impairment test for Global Card Services, the carrying value

of the goodwill assigned to the reporting unit exceeded the implied fair value

by $10.4 billion. Accordingly, we recorded a non-cash, non-tax deductible

goodwill impairment charge of $10.4 billion to reduce the carrying value of

goodwill in Global Card Services from $22.3 billion to $11.9 billion. The

goodwill impairment test included limited mitigation actions to recapture lost

revenue. Although we have identified other potential mitigation actions within

Global Card Services, the impact of these actions going forward did not

reduce the goodwill impairment charge because these actions are in the early

stages of development and, additionally, certain of them may impact seg-

ments other than Global Card Services (e.g., Deposits). The impairment

charge had no impact on the Corporation’s reported Tier 1 and tangible equity

ratios.

Due to the continued stress on Global Card Services as a result of the

Financial Reform Act, we concluded that an additional impairment analysis

should be performed for this reporting unit during the three months ended

December 31, 2010. In step one of the goodwill impairment test, the fair

value of Global Card Services was estimated under the income approach. The

significant assumptions under the income approach included the discount

rate, terminal value, expected loss rates and expected new account growth.

The carrying amount, fair value and goodwill for the Global Card Services

reporting unit were $27.5 billion, $27.6 billion and $11.9 billion, respectively.

The estimated fair value as a percent of the carrying amount at December 31,

2010 was 100 percent. Although fair value exceeded the carrying amount in

step one of the Global Card Services goodwill impairment test, to further

substantiate the value of goodwill, we also performed the step two test for

this reporting unit. Under step two of the goodwill impairment test for this

reporting unit, significant assumptions in measuring the fair value of the

assets and liabilities of the reporting unit including discount rates, loss rates

and interest rates were updated to reflect the current economic conditions.

The results of step two of the goodwill impairment test indicated that remain-

ing balance of goodwill of $11.9 billion was not impaired as of December 31,

2010.

On December 16, 2010, the Federal Reserve released proposed regula-

tions to implement the Durbin Amendment of the Financial Reform Act, which

are scheduled to be effective July 21, 2011. The proposed rule includes two

alternative interchange fee standards that would apply to all covered issuers:

one based on each issuer’s costs, with a safe harbor initially set at $0.07 per

transaction and a cap initially set at $0.12 per transaction; and the other a

stand-alone cap initially set at $0.12 per transaction. See Regulatory Matters

beginning on page 60 for additional information. Although the range of

revenue loss estimate based on the proposed rule was slightly higher than

our original estimate of $2.0 billion, given the uncertainty around the potential

outcome, we did not change the revenue loss estimate used in the goodwill

impairment test during the three months ended December 31, 2010. If the

final Federal Reserve rule sets interchange fee standards that are significantly

lower than the interchange fee assumptions we used in this goodwill impair-

ment test, we will be required to perform an additional goodwill impairment

test which may result in additional impairment of goodwill in Global Card

Services. In view of the uncertainty with model inputs including the final ruling,

changes in the economic outlook and the corresponding impact to revenues

and asset quality, and the impacts of mitigation actions, it is not possible to

estimate the amount or range of amounts of additional goodwill impairment, if

any.

Home Loans & Insurance Impairment

During the three months ended December 31, 2010, we performed an

impairment test for the Home Loans & Insurance reporting unit as it was

likely that there was a decline in its fair value as a result of increased

uncertainties, including existing and potential litigation exposure and other

related risks, higher current servicing costs including loss mitigation efforts,

foreclosure related issues and the redeployment of centralized sales re-

sources to address servicing needs. In step one of the goodwill impairment

test, the fair value of Home Loans & Insurance was estimated based on a

combination of the market approach and the income approach. Under the

market approach valuation, significant assumptions included market multi-

ples and a control premium. The significant assumptions for the valuation of

Home Loans & Insurance under the income approach included cash flow

estimates, the discount rate and the terminal value. These assumptions were

updated to reflect the current strategic plan forecast and to address the

increased uncertainties referenced above. Based on the results of step one of

the impairment test,we determined that the carrying amount of Home

Loans & Insurance, including goodwill, exceeded the fair value. The carrying

amount, fair value and goodwill for the Home Loans & Insurance reporting unit

were $24.7 billion, $15.1 billion and $4.8 billion, respectively. Accordingly, we

performed step two of the goodwill impairment test for this reporting unit. In

step two, we compared the implied fair value of the reporting unit’s goodwill

with the carrying amount of that goodwill. Under step two of the goodwill

impairment test, significant assumptions in measuring the fair value of the

assets and liabilities of the reporting unit including discount rates, loss rates

and interest rates were updated to reflect the current economic conditions.

Based on the results of step two of the impairment test, the carrying value of

the goodwill assigned to Home Loans & Insurance exceeded the implied fair

value by $2.0 billion. Accordingly, we recorded a non-cash, non-tax deductible

goodwill impairment charge of $2.0 billion as of December 31, 2010 to

reduce the carrying value of goodwill in the Home Loans & Insurance reporting

unit. The impairment charge had no impact on the Corporation’s Tier 1 and

tangible equity ratios.

As we obtain additional information relative to our litigation exposure,

representations and warranties repurchase obligations, servicing costs and

foreclosure related issues, it is possible that such information, if significantly

different than the assumptions used in this goodwill impairment test, may

result in additional impairment in the Home Loans & Insurance reporting unit.

Annual Impairment Test for 2010

We perform our annual goodwill impairment test for all reporting units as of

June 30 each year. In performing the first step of the June 30, 2010 annual

impairment test, we compared the fair value of each reporting unit to its

current carrying amount, including goodwill. To determine fair value, we

utilized a combination of a market approach and an income approach. Under

the market approach, we compared earnings and equity multiples of the

individual reporting units to multiples of publicly traded companies compa-

rable to the individual reporting units. The control premiums used in the

June 30, 2010 annual impairment test ranged from 25 to 35 percent. Under

the income approach, we updated our assumptions to reflect the current

market environment. The discount rates used in the June 30, 2010 annual

impairment test ranged from 11 to 15 percent depending on the relative risk

of a reporting unit. Because growth rates developed by management for

Bank of America 2010 115