Bank of America 2010 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

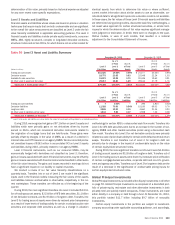

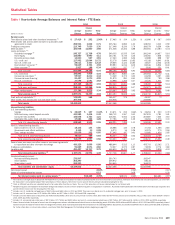

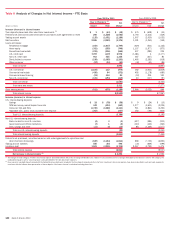

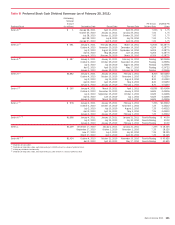

Business Segment Operations

Deposits

Net income decreased $3.0 billion to $2.6 billion driven by lower net revenue

partially offset by an increase in noninterest expense. Net interest income

decreased $3.8 billion driven by lower net interest income allocation from

ALM activities and spread compression as interest rates declined. Noninter-

est income was essentially flat at $6.8 billion. Noninterest expense increased

$908 million to $9.5 billion primarily due to higher FDIC insurance including a

special FDIC assessment, partially offset by lower operating costs related to

lower transaction volume due to the economy and productivity initiatives.

Global Card Services

Net income decreased $6.8 billion to a net loss of $5.3 billion due to higher

provision for credit losses. Net interest income grew $667 million to $20.0 bil-

lion driven by increased loan spreads. Noninterest income decreased $2.6 bil-

lion to $9.1 billion driven by decreases in card income and all other income.

The decrease in card income resulted from lower cash advances, credit card

interchange and fee income. All other income in 2008 included the gain

associated with the Visa initial public offering (IPO). Provision for credit losses

increased $10.0 billion to $29.6 billion primarily driven by higher losses in the

consumer card and consumer lending portfolios from impact of the economic

conditions. Noninterest expense decreased $1.2 billion to $7.7 billion pri-

marily due to lower operating and marketing costs, and the impact of certain

benefits associated with the Visa IPO transactions.

Home Loans & Insurance

Home Loans & Insurance net loss increased $1.3 billion to a net loss of

$3.9 billion as growth in noninterest income and net interest income was

more than offset by higher provision for credit losses and an increase in

noninterest expense. Net interest income grew $1.7 billion driven primarily by

an increase in average LHFS and home equity loans. The growth in average

LHFS was a result of higher mortgage loan volume driven by the lower interest

rate environment. The growth in average home equity loans was attributable to

the migration of certain loans from GWIM to Home Loans & Insurance as well

as the Countrywide acquisition. Noninterest income increased $5.9 billion to

$11.9 billion driven by higher mortgage banking income which benefited from

the Countrywide acquisition and higher production income, partially offset by

higher representations and warranties provision. Provision for credit losses

increased $5.0 billion to $11.2 billion driven primarily by higher losses in the

home equity portfolio and reserve increases in the Countrywide home equity

PCI portfolio. Noninterest expense increased $4.7 billion to $11.7 billion

primarily driven by the Countrywide acquisition as well as increased costs

related to higher production volume.

Global Commercial Banking

Net income decreased $2.9 billion to a net loss of $290 million in 2009 as an

increase in revenue was more than offset by increased credit costs. Net

interest income was essentially flat at $8.1 billion. Noninterest income

increased $552 million to $3.1 billion largely driven by our agreement to

purchase certain retail automotive loans. The provision for credit losses

increased $4.5 billion to $7.8 billion, driven by reserve additions primarily

in the commercial real estate portfolio and higher net charge-offs across all

portfolios. Noninterest expense increased $501 million primarily attributable

to higher FDIC insurance, including a special FDIC assessment.

Global Banking & Markets

Global Banking & Markets recognized net income of $10.1 billion in 2009

compared to a net loss of $3.2 billion in 2008 as increased noninterest

income driven by trading account profits was partially offset by higher non-

interest expense. Sales and trading revenue was $17.6 billion in 2009

compared to a loss of $6.9 billion in 2008 primarily due to the addition of

Merrill Lynch. Noninterest income also included a $3.8 billion pre-tax gain

related to the contribution of the merchant processing business into a joint

venture. Noninterest expense increased $8.6 billion, largely attributable to

the Merrill Lynch acquisition.

Global Wealth & Investment Management

Net income increased $702 million to $1.7 billion in 2009 as higher total

revenue was partially offset by increases in noninterest expense and provi-

sion for credit losses. Net interest income increased $1.2 billion to $6.0 billion

primarily due to the acquisition of Merrill Lynch. Noninterest income increased

$8.6 billion to $10.1 billion primarily due to higher investment and brokerage

services income and the lower level of support provided to certain cash funds,

partially offset by the impact of lower average equity market levels and net

outflows primarily in the cash complex. Provision for credit losses increased

$397 million to $1.1 billion, reflecting the weak economy during 2009 which

drove higher net charge-offs in the consumer real estate and commercial

portfolios. Noninterest expense increased $8.3 billion to $12.4 billion driven

by the addition of Merrill Lynch and higher FDIC insurance, including a special

FDIC assessment, partially offset by lower revenue-related expenses.

All Other

Net income in All Other was $1.3 billion in 2009 compared to a net loss of

$1.1 billion in 2008 as higher total revenue driven by increases in noninterest

income, net interest income and an income tax benefit were partially offset by

increased provision for credit losses, merger and restructuring charges and all

other noninterest expense. Net interest income increased $1.5 billion prima-

rily due to unallocated net interest income related to increased liquidity driven

in part by capital raises during 2009. Noninterest income increased $8.2 bil-

lion to $10.6 billion driven by higher equity investment income including a

$7.3 billion gain on the sale of a portion of our CCB investment and gains on

sales of debt securities. These were partially offset by a $4.9 billion negative

valuation adjustment on certain structured liabilities. Provision for credit

losses was $8.0 billion in 2009 compared to $2.8 billion in 2008 primarily

due to higher credit costs related to our ALM residential mortgage portfolio.

Merger and restructuring charges increased $1.8 billion to $2.7 billion due to

the integration costs associated with the Merrill Lynch and Countrywide

acquisitions.

118 Bank of America 2010