Bank of America 2010 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

ineffective or inappropriate business plans, or failure to respond to changes in

the competitive environment, business cycles, customer preferences, product

obsolescence, regulatory environment, business strategy execution and/or

other inherent risks of the business including reputational risk. In the financial

services industry, strategic risk is high due to changing customer, competitive

and regulatory environments. Our appetite for strategic risk is assessed within

the context of the strategic plan, with strategic risks selectively and carefully

considered in the context of the evolving marketplace. Strategic risk is man-

aged in the context of our overall financial condition and assessed, managed

and acted on by the Chief Executive Officer and executive management team.

Significant strategic actions, such as material acquisitions or capital actions,

are reviewed and approved by the Board.

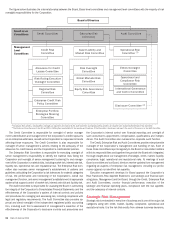

Executive management and the Board approve a strategic plan every two

to three years. Annually, executive management develops a financial operat-

ing plan and the Board reviews and approves the plan. With oversight by the

Board, executive management ensures that the plans are consistent with the

Corporation’s strategic plan, core operating tenets and risk appetite. The

following are assessed in their reviews: forecasted earnings and returns on

capital, the current risk profile, current capital and liquidity requirements,

staffing levels and changes required to support the plan, stress testing

results, and other qualitative factors such as market growth rates and peer

analysis. With oversight by the Board, executive management performs

similar analyses throughout the year, and defines changes to the financial

forecast or the risk, capital or liquidity positions as deemed appropriate to

balance and optimize between achieving the targeted risk appetite and

shareholder returns and maintaining the targeted financial strength.

We use proprietary models to measure the capital requirements for credit,

country, market, operational and strategic risks. The economic capital as-

signed to each line of business is based on its unique risk exposures. With

oversight by the Board, executive management assesses the risk-adjusted

returns of each business in approving strategic and financial operating plans.

The businesses use economic capital to define business strategies, price

products and transactions, and evaluate client profitability.

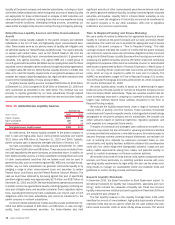

Capital Management

Bank of America manages its capital position to maintain a strong and flexible

financial position in order to perform through economic cycles, take advan-

tage of organic growth opportunities, maintain ready access to financial

markets, remain a source of financial strength for its subsidiaries, and return

capital to its shareholders as appropriate.

To determine the appropriate level of capital, we assess the results of our

Internal Capital Adequacy Assessment Process (ICAAP), the current economic

and market environment, and feedback from investors, ratings agencies and

regulators. Based upon this analysis we set capital guidelines for Tier 1

common capital and Tier 1 capital to ensure we can maintain an adequate

capital position in a severe adverse economic scenario. We also target to

maintain capital in excess of the capital required per our economic capital

measurement process (see Economic Capital on page 70). Management and

the Board annually approve a comprehensive Capital Plan which documents

the ICAAP and related results, analysis and support for the capital guidelines,

and planned capital actions and capital adequacy assessment.

The ICAAP incorporates capital forecasts, stress test results, economic

capital, qualitative risk assessments and assessment of regulatory changes.

We generate monthly regulatory capital and economic capital forecasts that are

aligned to the most recent earnings, balance sheet and risk forecasts. We utilize

quarterly stress tests to assess the potential impacts to earnings, capital and

liquidity for a variety of economic stress scenarios. We perform qualitative risk

assessments to identify and assess material risks not fully captured in the

forecasts, stress tests or economic capital. Given the significant proposed

regulatory capital changes, we also regularly assess the potential capital

impacts and monitor associated mitigation actions. Management continuously

assesses ICAAP results and provides documented quarterly assessments of

the adequacy of the capital guidelines and capital position to the Board.

Capital management is integrated into the risk and governance pro-

cesses, as capital is a key consideration in development of the strategic

plan, risk appetite and risk limits. Economic capital is allocated to each

business unit and used to perform risk-adjusted return analysis at the busi-

ness unit, client relationship and transaction level.

Regulatory Capital

As a financial services holding company, we are subject to the risk-based capital

guidelines (Basel I) issued by the Federal Reserve. At December 31, 2010, we

operated banking activities primarily under two charters: Bank of America, N.A.

and FIA Card Services, N.A. which are subject to the risk-based capital guide-

lines issued by the Office of the Comptroller of the Currency (OCC). Under these

guidelines, the Corporation and its affiliated banking entities measure capital

adequacy based on Tier 1 common capital, Tier 1 capital and Total capital (Tier 1

plus Tier 2 capital). Capital ratios are calculated by dividing each capital amount

by risk-weighted assets. Additionally, Tier 1 capital is divided by adjusted

quarterly average total assets to derive the Tier 1 leverage ratio.

Tier 1 capital is calculated as the sum of “core capital elements.” The

predominate components of core capital elements are qualifying common

stockholders’ equity, any CES and qualifying noncumulative perpetual preferred

stock. Also included in Tier 1 capital are qualifying trust preferred capital debt

securities (Trust Securities), hybrid securities and qualifying non-controlling

interest in subsidiaries which are subject to the rules governing “restricted

core capital elements.” Goodwill, other disallowed intangible assets, disallowed

deferred tax assets and the cumulative changes in fair value of all financial

liabilities accounted for under a fair value option that are included in retained

earnings and are attributable to changes in the company’s own creditworthiness

are deducted from the sum of the core capital elements. Total capital is Tier 1

plus supplementary Tier 2 capital elements such as qualifying subordinated

debt, a limited portion of the allowance for loan and lease losses, and a portion

of net unrealized gains on AFS marketable equity securities. Tier 1 common

capital is not an official regulatory ratio, but was introduced by the Federal

Reserve during the Supervisory Capital Assessment Program in 2009. Tier 1

common capital is Tier 1 capital less preferred stock, Trust Securities, hybrid

securities and qualifying non-controlling interest in subsidiaries.

Risk-weighted assets are calculated for credit risk for all on- and off-balance

sheet credit exposures and for market risk on trading assets and liabilities,

including derivative exposures. Credit risk risk-weighted assets are calculated by

assigning a prescribed risk-weight to all on-balance sheet assets and to the

credit equivalent amount of certain off-balance sheet exposures. The risk-weight

is defined in the regulatory rules based upon the obligor or guarantor type and

collateral if applicable. Off-balance sheet exposures include financial guaran-

tees, unfunded lending commitments, letters of credit and derivatives. Market

risk risk-weighted assets are calculated using risk models for the trading

account positions, including all foreign exchange and commodity positions

regardless of the applicable accounting guidance. Under Basel I there are no

risk-weighted assets calculated for operational risk. Any assets that are a direct

deduction from the computation of capital are excluded from risk-weighted

assets and adjusted average total assets consistent with regulatory guidance.

For additional information on these and other regulatory requirements,

see Note 18 – Regulatory Requirements and Restrictions to the Consolidated

Financial Statements.

Capital Composition and Ratios

On January 21, 2010, the joint agencies issued a final rule regarding the

impact of the new consolidation guidance on risk-based capital. The incre-

mental impact on January 1, 2010 was an increase in assets of $100.4 billion

and risk-weighted assets of $21.3 billion and a reduction in Tier 1 common

Bank of America 2010 67