Bank of America 2010 Annual Report Download - page 174

Download and view the complete annual report

Please find page 174 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

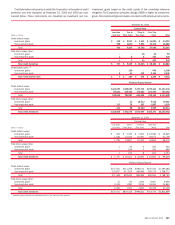

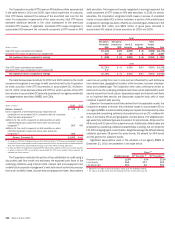

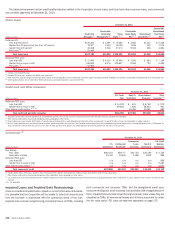

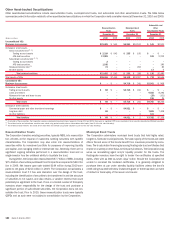

The tables below present certain credit quality indicators related to the Corporation’s home loans, credit card and other consumer loans, and commercial

loan portfolio segments at December 31, 2010.

Home Loans

(Dollars in millions)

Residential

Mortgage

(1)

Countrywide

Residential

Mortgage PCI

(2)

Home

Equity

(1, 3)

Countrywide

Home Equity

PCI

(2, 3)

Discontinued

Real Estate

(1)

Countrywide

Discontinued

Real Estate

PCI

(2)

December 31, 2010

Refreshed LTV

Less than 90 percent $130,260 $ 3,390 $ 73,680 $ 1,883 $1,033 $ 5,248

Greater than 90 percent but less than 100 percent 19,907 1,654 14,038 1,186 155 1,578

Greater than 100 percent 43,268 5,548 37,673 9,521 268 4,826

FHA Loans

(4)

53,946 – – – – –

Total home loans $247,381 $10,592 $125,391 $12,590 $1,456 $11,652

Refreshed FICO score

Less than 620 $ 27,483 $ 4,016 $ 15,494 $ 3,206 $ 663 $ 7,168

Greater than or equal to 620 165,952 6,576 109,897 9,384 793 4,484

FHA Loans

(4)

53,946 – – – – –

Total home loans $247,381 $10,592 $125,391 $12,590 $1,456 $11,652

(1)

Excludes Countrywide PCI loans.

(2)

Excludes PCI home loans related to the Merrill Lynch acquisition.

(3)

Refreshed LTV is reported using a combined LTV, which measures the carrying value of the combined loans with liens against the property and the available line of credit as a percentage of the appraised value securing the loan.

(4)

Credit quality indicators are not reported for FHA insured loans as principal repayment is insured by the FHA.

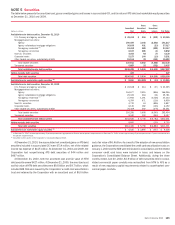

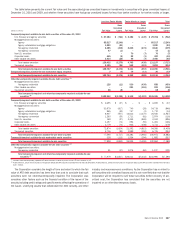

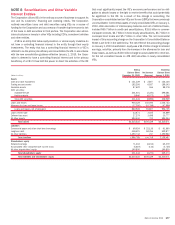

Credit Card and Other Consumer

(Dollars in millions)

U.S. Credit

Card

Non-U.S.

Credit Card

Direct/Indirect

Consumer

Other

Consumer

(1)

December 31, 2010

Refreshed FICO score

Less than 620 $ 14,159 $ 631 $ 6,748 $ 979

Greater than or equal to 620 99,626 7,528 48,209 961

Other internal credit metrics

(2, 3, 4)

– 19,306 35,351 890

Total credit card and other consumer $113,785 $27,465 $90,308 $2,830

(1)

96 percent of the other consumer portfolio was associated with portfolios from certain consumer finance businesses that have been previously exited by the Corporation.

(2)

Other internal credit metrics may include delinquency status, geography or other factors.

(3)

Direct/indirect consumer includes $24.0 billion of securities-based lending which is overcollateralized and therefore offers minimal credit risk and $7.4 billion of loans the Corporation no longer originates.

(4)

Non-U.S. credit card represents the select European countries’ credit card portfolio and a portion of the Canadian credit card portfolio which is evaluated using internal credit metrics, including delinquency status. At December 31,

2010, 95 percent of this portfolio was current or less than 30 days past due, three percent was 30-89 days past due and two percent was 90 days or more past due.

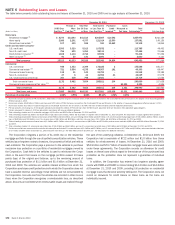

Commercial

(1)

(Dollars in millions)

U.S.

Commercial

Commercial

Real Estate

Commercial

Lease

Financing

Non-U.S.

Commercial

U.S. Small

Business

Commercial

December 31, 2010

Risk Ratings

Pass rated $160,154 $29,757 $20,754 $30,180 $ 3,139

Reservable criticized 15,432 19,636 1,188 1,849 988

Refreshed FICO score

Less than 620 n/a n/a n/a n/a 888

Greater than or equal to 620 n/a n/a n/a n/a 5,083

Other internal credit metrics

(2, 3)

n/a n/a n/a n/a 4,621

Total commercial credit $175,586 $49,393 $21,942 $32,029 $14,719

(1)

Includes $204 million of PCI loans related to the commercial portfolio segment and excludes $3.3 billion of loans accounted for under the fair value option.

(2)

Other internal credit metrics may include delinquency status, application scores, geography or other factors.

(3)

U.S. small business commercial includes business card and small business loans which are evaluated using internal credit metrics, including delinquency status. At December 31, 2010, 95 percent was current or less than 30 days

past due.

n/a = not applicable

Impaired Loans and Troubled Debt Restructurings

A loan is considered impaired when, based on current information and events,

it is probable that the Corporation will be unable to collect all amounts due

from the borrower in accordance with the contractual terms of the loan.

Impaired loans include nonper forming commercial loans, all TDRs, including

both commercial and consumer TDRs, and the renegotiated credit card,

consumer lending and small business loan portfolios (the renegotiated port-

folio). Impaired loans exclude nonperforming consumer loans unless they are

classified as TDRs, all commercial leases and all loans accounted for under

the fair value option. PCI loans are reported separately on page 175.

172 Bank of America 2010