Bank of America 2010 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

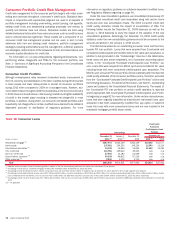

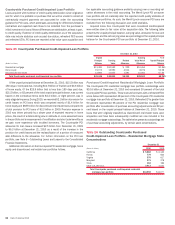

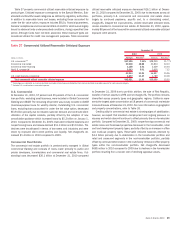

The table below presents certain state concentrations for the U.S. credit card portfolio on a held basis for 2010 and managed basis for December 31, 2009.

Table 30 U.S. Credit Card State Concentrations

(Dollars in millions)

2010 2009 2010 2009 2010 2009

Outstandings

Accruing Past Due

90 Days or More Net Charge-offs

December 31

Year Ended

December 31

California

$17,028

$20,048

$612

$1,097

$2,752

$3,558

Florida

9,121

10,858

376

676

1,611

2,178

Texas

7,581

8,653

207

345

784

960

New York

6,862

7,839

192

295

694

855

New Jersey

4,579

5,168

132

189

452

559

Other U.S.

68,614

77,076

1,801

2,806

6,734

8,852

Total U.S. credit card portfolio

$113,785

$129,642

$3,320

$5,408

$13,027

$16,962

Unused lines of credit for U.S. credit card totaled $399.7 billion at

December 31, 2010 compared to $438.5 billion at December 31, 2009

on a managed basis. The $38.8 billion decrease was driven by a combination

of account management initiatives on higher risk or inactive accounts and

tighter underwriting standards for new originations.

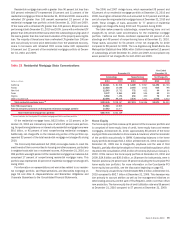

Non-U.S. Credit Card

Prior to the adoption of new consolidation guidance, the non-U.S. credit card

portfolio was reported on both a held and managed basis. Under the new

consolidation guidance effective January 1, 2010, we consolidated the credit

card securitization trusts and the new held basis is comparable to the

previously reported managed basis. For more information on the adoption

of the new consolidation guidance, see Note 8 – Securitizations and Other

Variable Interest Entities to the Consolidated Financial Statements.

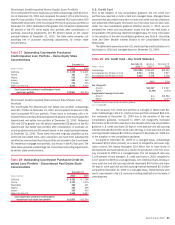

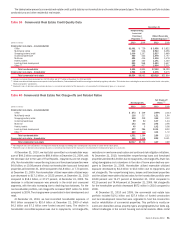

The table below presents certain non-U.S. credit card key credit statistics

on a held basis for 2010 and managed basis for December 31, 2009.

Table 31 Non-U.S. Credit Card – Key Credit Statistics

(Dollars in millions)

December 31

2010

(1)

January 1

2010

(1)

December 31

2009

Outstandings

$27,465

$31,182 $21,656

Accruing past due 30 days or more

1,354

1,744 1,104

Accruing past due 90 days or more

599

814 515

2010 2009

Net charge-offs

Amount

$2,207

$1,239

Ratio

7.88%

6.30%

Supplemental managed basis data

Amount

n/a

$2,223

Ratio

n/a

7.43%

(1)

Balances reflect the impact of new consolidation guidance.

n/a = not applicable

The consumer non-U.S. credit card portfolio is managed in Global Card

Services. Outstandings in the non-U.S. credit card portfolio increased $5.8 bil-

lion compared to December 31, 2009 due to the adoption of the new

consolidation guidance. Additionally, net charge-off levels and ratios for

2010, when compared to 2009, were impacted by the adoption of the new

consolidation guidance. Net charge-offs increased $1.0 billion to $2.2 billion

in 2010.

Outstandings declined $3.7 billion compared to December 31, 2009 on a

managed basis primarily due to charge-offs, lower origination volume and the

strengthening of the U.S. dollar against certain foreign currencies. Net losses

were substantially flat for 2010, decreasing $16 million from managed losses

in 2009. The net loss ratio increased to 7.88 percent of total average

non-U.S. credit card compared to 7.43 percent in 2009, due to the decrease

in outstandings.

Unused lines of credit for non-U.S. credit card totaled $60.3 billion at

December 31, 2010 compared to $69.6 billion at December 31, 2009 on a

managed basis. The $9.3 billion decrease was driven by the combination of

account management initiatives on inactive accounts, tighter underwriting

standards for new originations and the strengthening of the U.S. dollar against

certain foreign currencies, particularly the British Pound and the Euro.

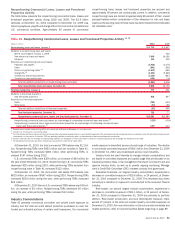

Direct/Indirect Consumer

At December 31, 2010, approximately 48 percent of the direct/indirect

portfolio was included in Global Commercial Banking (dealer financial serv-

ices – automotive, marine and recreational vehicle loans), 29 percent was

included in GWIM (principally other non-real estate-secured, unsecured per-

sonal loans and securities-based lending margin loans), 15 percent was

included in Global Card Services (consumer personal loans and other non-real

estate-secured loans) and the remainder was in All Other (student loans).

Outstanding loans and leases decreased $6.9 billion to $90.3 billion at

December 31, 2010 compared to December 31, 2009 as lower outstandings

in the Global Card Services unsecured consumer lending por tfolio and the

sale of a portion of the student loan portfolio were partially offset by the

adoption of new consolidation guidance, growth in securities-based lending

and the purchase of auto receivables within the dealer financial services

portfolio. Direct/indirect loans that were past due 30 days or more and still

accruing interest declined $1.1 billion compared to December 31, 2009, to

$2.6 billion due to a combination of reduced outstandings and improvement

in the unsecured consumer lending portfolio. Net charge-offs decreased

$2.1 billion to $3.3 billion in 2010, or 3.45 percent of total average di-

rect/indirect loans compared to 5.46 percent in 2009. This decrease was

primarily driven by reduced outstandings from changes in underwriting criteria

and lower levels of delinquencies and bankruptcies in the unsecured con-

sumer lending portfolio as a result of improvement in the U.S. economy

including stabilization in the levels of unemployment. An additional driver was

lower net charge-offs in the dealer financial services portfolio due to the

impact of higher credit quality originations and higher resale values. Net

charge-offs for the unsecured consumer lending portfolio decreased $1.6 bil-

lion to $2.7 billion and the net charge-off ratio decreased to 16.74 percent in

2010 compared to 17.75 percent in 2009. Net charge-offs for the dealer

financial services portfolio decreased $404 million to $487 million and the

loss rate decreased to 1.08 percent in 2010 compared to 2.16 percent in

2009.

84 Bank of America 2010