Bank of America 2010 Annual Report Download - page 197

Download and view the complete annual report

Please find page 197 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

based on the rates in effect at December 31, 2009, were 3.62 percent,

4.93 percent and 0.80 percent, respectively, at December 31, 2009. The

Corporation’s ALM activities maintain an overall interest rate risk manage-

ment strategy that incorporates the use of interest rate contracts to manage

fluctuations in earnings that are caused by interest rate volatility. The

Corporation’s goal is to manage interest rate sensitivity so that movements

in interest rates do not significantly adversely affect net interest income. The

above weighted-average rates are the contractual interest rates on the debt,

and do not reflect the impacts of derivative transactions.

The weighted-average interest rate for debt, excluding senior structured

notes, issued by Merrill Lynch & Co., Inc. and subsidiaries was 4.11 percent

and 3.73 percent at December 31, 2010 and 2009. At December 31, 2010,

the Corporation has not assumed or guaranteed the $120.9 billion of long-

term debt that was issued or guaranteed by Merrill Lynch & Co., Inc. or its

subsidiaries prior to the acquisition of Merrill Lynch by the Corporation.

Beginning late in the third quarter of 2009, in connection with the update

or renewal of certain Merrill Lynch non-U.S. securities offering programs, the

Corporation agreed to guarantee debt securities, warrants and/or certificates

issued by certain subsidiaries of Merrill Lynch & Co., Inc. on a going-forward

basis. All existing Merrill Lynch & Co., Inc. guarantees of securities issued by

those same Merrill Lynch subsidiaries under various non-U.S. securities

offering programs will remain in full force and effect as long as those secu-

rities are outstanding, and the Corporation has not assumed any of those prior

Merrill Lynch & Co., Inc. guarantees or otherwise guaranteed such securities.

Certain senior structured notes issued by Merrill Lynch are accounted for

under the fair value option. For more information on these senior structured

notes, see Note 23 – Fair Value Option.

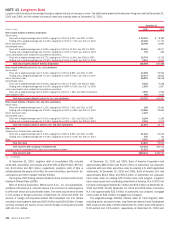

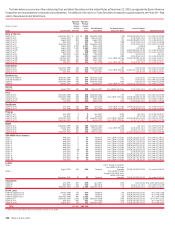

The table below represents the book value for aggregate annual maturities

of long-term debt at December 31, 2010.

(Dollars in millions)

2011 2012 2013 2014 2015 Thereafter Total

Bank of America Corporation $16,419 $40,432 $ 8,731 $21,890 $13,236 $ 85,888

$186,596

Merrill Lynch & Co., Inc. and subsidiaries 26,554 18,611 18,053 16,650 4,515 41,370

125,753

Bank of America, N.A. and other subsidiaries 4,382 5,796 86 503 1,015 9,485

21,267

Other debt 22,760 12,549 5,031 1,293 105 2,064

43,802

Total long-term debt excluding consolidated VIEs

70,115 77,388 31,901 40,336 18,871 138,807

377,418

Long-term debt of consolidated VIEs under new consolidation guidance 19,136 11,800 17,514 9,103 1,229 12,231

71,013

Total long-term debt $89,251 $89,188 $49,415 $49,439 $20,100 $151,038 $448,431

Included in the above table are certain structured notes that contain

provisions whereby the borrowings are redeemable at the option of the holder

(put options) at specified dates prior to maturity. Other structured notes have

coupon or repayment terms linked to the performance of debt or equity

securities, indices, currencies or commodities and the maturity may be

accelerated based on the value of a referenced index or security. In both

cases, the Corporation or a subsidiary may be required to settle the obligation

for cash or other securities prior to the contractual maturity date. These

borrowings are reflected in the above table as maturing at their earliest put or

redemption date.

Trust Preferred and Hybrid Securities

Trust preferred securities (Trust Securities) are issued by trust companies

(the Trusts) that are not consolidated. These Trust Securities are mandatorily

redeemable preferred security obligations of the Trusts. The sole assets of

the Trusts generally are junior subordinated deferrable interest notes of the

Corporation or its subsidiaries (the Notes). The Trusts generally are 100 per-

cent owned finance subsidiaries of the Corporation. Obligations associated

with the Notes are included in the long-term debt table on page 194.

Certain of the Trust Securities were issued at a discount and may be

redeemed prior to maturity at the option of the Corporation. The Trusts

generally have invested the proceeds of such Trust Securities in the Notes.

Each issue of the Notes has an interest rate equal to the corresponding

Trust Securities distribution rate. The Corporation has the right to defer

payment of interest on the Notes at any time or from time to time for a

period not exceeding five years provided that no extension period may extend

beyond the stated maturity of the relevant Notes. During any such extension

period, distributions on the Trust Securities will also be deferred and the

Corporation’s ability to pay dividends on its common and preferred stock will

be restricted.

The Trust Securities generally are subject to mandatory redemption upon

repayment of the related Notes at their stated maturity dates or their earlier

redemption at a redemption price equal to their liquidation amount plus

accrued distributions to the date fixed for redemption and the premium, if

any, paid by the Corporation upon concurrent repayment of the related Notes.

Periodic cash payments and payments upon liquidation or redemption with

respect to Trust Securities are guaranteed by the Corporation or its subsid-

iaries to the extent of funds held by the Trusts (the Preferred Securities

Guarantee). The Preferred Securities Guarantee, when taken together with

the Corporation’s other obligations including its obligations under the Notes,

generally will constitute a full and unconditional guarantee, on a subordinated

basis, by the Corporation of payments due on the Trust Securities.

Hybrid Income Term Securities (HITS) totaling $1.6 billion were also issued

by the Trusts to institutional investors in 2007. The BAC Capital Trust XIII

Floating-Rate Preferred HITS have a distribution rate of three-month LIBOR

plus 40 bps and the BAC Capital Trust XIV Fixed-to-Floating-Rate Preferred

HITS have an initial distribution rate of 5.63 percent. Both series of HITS

represent beneficial interests in the assets of the respective capital trust,

which consist of a series of the Corporation’s junior subordinated notes and a

stock purchase contract for a specified series of the Corporation’s preferred

stock. The Corporation will remarket the junior subordinated notes underlying

each series of HITS on or about the five-year anniversary of the issuance to

obtain sufficient funds for the capital trusts to buy the Corporation’s preferred

stock under the stock purchase contracts.

In connection with the HITS, the Corporation entered into two replacement

capital covenants for the benefit of investors in certain series of the Corpo-

ration’s long-term indebtedness (Covered Debt). As of December 31, 2010,

the Corporation’s 6.625% Junior Subordinated Notes due 2036 constitute

the Covered Debt under the covenant corresponding to the Floating-Rate

Preferred HITS and the Corporation’s 5.625% Junior Subordinated Notes due

2035 constitute the Covered Debt under the covenant corresponding to the

Fixed-to-Floating-Rate Preferred HITS. These covenants generally restrict the

ability of the Corporation and its subsidiaries to redeem or purchase the HITS

and related securities unless the Corporation has obtained the prior approval

of the Federal Reserve if required under the Federal Reserve’s capital

guidelines, the redemption or purchase price of the HITS does not exceed

the amount received by the Corporation from the sale of certain qualifying

securities, and such replacement securities qualify as Tier 1 Capital and are

not “restricted core capital elements” under the Federal Reserve’s

guidelines.

Bank of America 2010 195