Bank of America 2010 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

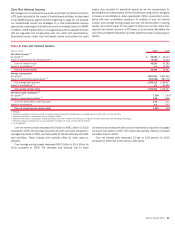

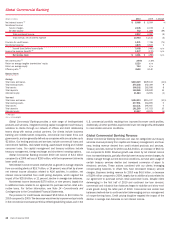

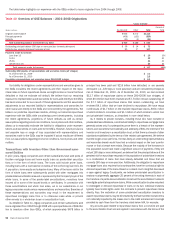

Global Commercial Banking

(Dollars in millions)

2010 2009 % Change

Net interest income

(1)

$8,086

$8,054 –%

Noninterest income:

Service charges

2,105

2,078 1

All other income

712

1,009 (29)

Total noninterest income

2,817

3,087 (9)

Total revenue, net of interest expense

10,903

11,141 (2)

Provision for credit losses

1,971

7,768 (75)

Noninterest expense

3,874

3,833 1

Income (loss) before income taxes

5,058

(460) n/m

Income tax expense (benefit)

(1)

1,877

(170) n/m

Net income (loss)

$3,181

$ (290) n/m

Net interest yield

(1)

2.94%

3.19%

Return on average tangible shareholders’ equity

15.20

n/m

Return on average equity

7.64

n/m

Efficiency ratio

(1)

35.52

34.40

Balance Sheet

Average

Total loans and leases

$203,339

$229,102 (11)%

Total earning assets

275,356

252,309 9

Total assets

306,302

283,936 8

Total dep osits

148,565

129,832 14

Allocated equity

41,624

41,931 (1)

Year end

Total loans and leases

$193,573

$215,237 (10)%

Total earning assets

277,551

264,855 5

Total assets

310,131

295,947 5

Total dep osits

161,260

147,023 10

Allocated equity

40,607

42,975 (6)

(1)

FTE basis

n/m = not meaningful

Global Commercial Banking provides a wide range of lending-related

products and services, integrated working capital management and treasury

solutions to clients through our network of offices and client relationship

teams along with various product partners. Our clients include business

banking and middle-market companies, commercial real estate firms and

governments, and are generally defined as companies with annual sales up to

$2 billion. Our lending products and services include commercial loans and

commitment facilities, real estate lending, asset-based lending and indirect

consumer loans. Our capital management and treasury solutions include

treasury management, foreign exchange and short-term investing options.

Global Commercial Banking recorded 2010 net income of $3.2 billion

compared to a 2009 net loss of $290 million, with the improvement driven by

lower credit costs.

Net interest income remained relatively flat as growth in average deposits

from our existing clients of $18.7 billion, or 14 percent, was offset by a lower

net interest income allocation related to ALM activities. In addition, net

interest income benefited from credit pricing discipline, which negated the

impact of the $25.8 billion, or 11 percent, decline in average loan balances.

Noninterest income decreased $270 million, or nine percent, largely due

to additional costs related to our agreement to purchase certain retail auto-

motive loans. For further information, see Note 14 – Commitments and

Contingencies to the Consolidated Financial Statements.

The provision for credit losses decreased $5.8 billion to $2.0 billion for

2010 compared to 2009. The decrease was driven by improvements primarily

in the commercial real estate portfolios reflecting stabilizing values and in the

U.S. commercial portfolio resulting from improved borrower credit profiles.

Additionally, all other portfolios experienced lower net charge-offs attributable

to more stable economic conditions.

Global Commercial Banking Revenue

Global Commercial Banking revenues can also be categorized as treasury

services revenue primarily from capital and treasury management, and busi-

ness lending revenue derived from credit related products and services.

Treasury services revenue for 2010 was $4.3 billion, an increase of $62 mil-

lion compared to 2009. Revenue growth was driven by net interest income

from increased deposits, partially offset by lower treasury service charges. As

clients manage through current economic conditions, we have seen usage of

certain treasury services decline and increased conversion of paper to

electronic services. These actions combined with our clients leveraging

compensating balances to offset fees have decreased treasury service

charges. Business lending revenue for 2010 was $6.6 billion, a decrease

of $299 million compared to 2009, largely due to additional costs related to

our agreement to purchase certain retail automotive loans. Despite client

deleveraging in the first half of 2010 and continued low loan demand,

commercial and industrial loan balances began to stabilize and show mod-

erate growth during the latter part of 2010. Commercial real estate loan

balances declined due to continued client deleveraging and our management

of nonperforming loans. Credit pricing discipline negated the impact of the

decline in average loan balances on net interest income.

48 Bank of America 2010