Bank of America 2010 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

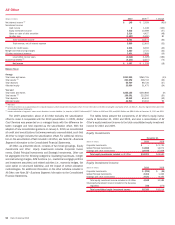

FDIC Deposit Insurance Assessments

Since the financial crisis began several years ago, an increasing number of bank

failures has imposed significant costs on the FDIC in resolving those failures,

and the regulator’s deposit insurance fund has been depleted. In order to

maintain a strong funding position and restore reserve ratios of the deposit

insurance fund, the FDIC has increased, and may increase in the future,

assessment rates of insured institutions, including Bank of America.

Deposits placed at the U.S. Banks are insured by the FDIC, subject to

limits and conditions of applicable law and the FDIC’s regulations. Pursuant to

the Financial Reform Act, FDIC insurance coverage limits were permanently

increased to $250,000 per customer. The Financial Reform Act also provides

for unlimited FDIC insurance coverage for non-interest bearing demand de-

posit accounts for a two-year period beginning on December 31, 2010 and

ending on January 1, 2013. The FDIC administers the Deposit Insurance

Fund, and all insured depository institutions are required to pay assessments

to the FDIC that fund the Deposit Insurance Fund. The Financial Reform Act

changed the methodology for calculating deposit insurance assessments

from the amount of an insured depository institution’s domestic deposits to

its total assets minus tangible capital. On February 7, 2011 the FDIC issued a

new regulation implementing revisions to the assessment system mandated

by the Financial Reform Act. The new regulation will be effective April 1, 2011

and will be reflected in the June 30, 2011 FDIC fund balance and the invoices

for assessments due September 30, 2011. As a result of the new regula-

tions, we expect to incur higher annual deposit insurance assessments. We

have identified potential mitigation actions, but they are in the early stages of

development and we are not able to directly control the basis or the amount of

premiums that we are required to pay for FDIC insurance or for other fees or

assessment obligations imposed on financial institutions. Any future in-

creases in required deposit insurance premiums or other bank industry fees

could have a significant adverse impact on our financial condition and results

of operations.

CARD Act

On May 22, 2009, the CARD Act was signed into law. The majority of the CARD

Act provisions became effective in February 2010. The CARD Act legislation

contains comprehensive credit card reform related to credit card industry

practices including significantly restricting banks’ ability to change interest

rates and assess fees to reflect individual consumer risk, changing the way

payments are applied and requiring changes to consumer credit card disclo-

sures. The provisions of the CARD Act negatively impacted net interest income

and card income during 2010, and are expected to negatively impact future

net interest income due to the restrictions on our ability to reprice credit cards

based on risk, and card income due to restrictions imposed on certain fees.

The 2010 full-year decrease in revenue was approximately $1.5 billion.

Regulation E

On November 12, 2009, the Federal Reserve issued amendments to Regula-

tion E which implements the Electronic Fund Transfer Act. The rules became

effective on July 1, 2010 for new customers and August 16, 2010 for existing

customers. These amendments limit the way we and other banks charge an

overdraft fee for non-recurring debit card transactions that overdraw a consum-

er’s account unless the consumer affirmatively consents to the bank’s payment

of overdrafts for those transactions. Under previously announced plans, we do

not offer customers the opportunity to opt-in to overdraft services related to non-

recurring debit card transactions. However, customers are able to opt-in on a

withdrawal-by-withdrawal basis to access cash through the Bank of America ATM

network where the bank is able to alert customers that the transaction may

overdraw their account and result in a fee if they choose to proceed. The impact

of Regulation E, which was in effect beginning in the third quarter and fully in

effect in the fourth quarter of 2010, and our overdraft policy changes, which

were in effect for the full year of 2010, was a reduction in service charges during

2010 of approximately $1.7 billion. In 2011, the incremental reduction to

service charges related to Regulation E and overdraft policy changes is expected

to be approximately $1.1 billion, or a full-year impact of approximately $2.8 bil-

lion, net of identified mitigation action.

U.K. Corporate Income Tax Rate

On July 27, 2010, the U.K. government enacted a law change reducing the

corporate income tax rate by one percent effective for the 2011 U.K. tax

financial year beginning on April 1, 2011. While this rate reduction favorably

affects income tax expense on future U.K. earnings, it also required us to

remeasure our U.K. net deferred tax assets using the lower tax rate, which

resulted in a charge to income tax expense of $392 million in 2010. A future

rate reduction of one percent per year is generally expected to be enacted in

each of 2011, 2012 and 2013, which would result in a similar charge to

income tax expense of nearly $400 million during each of the three years. The

U.K. Treasury has asked for taxpayer views on whether the U.K. government

should alternatively enact the full remaining three-percent reduction entirely

during 2011, which would accelerate the possible charges into 2011 for a

total of approximately $1.1 billion.

Final Regulatory Guidance on Consolidation

On January 21, 2010, the Federal Reserve, Office of the Comptroller of the

Currency, FDIC and Office of Thrift Supervision (collectively, joint agencies)

issued a final rule regarding risk-based capital requirements related to the

impact of the adoption of new consolidation guidance. The impact on the

Corporation on January 1, 2010 due to the new consolidation guidance and

the final rule was an increase in risk-weighted assets of $21.3 billion and a

reduction in capital of $9.7 billion. The overall impact of the new consolidation

guidance and the final rule was a decrease in Tier 1 capital and Tier 1 common

ratios of 76 bps and 73 bps. For more information, see Balance Sheet

Overview – Impact of Adopting New Consolidation Guidance on page 33,

Capital Management beginning on page 67 and Liquidity Risk beginning on

page 71.

Payment Protection Insurance

In the U.K., the Corporation sells PPI through its Global Card Services busi-

ness to credit card customers and has previously sold this insurance to

consumer loan customers. In response to an elevated level of customer

complaints of misleading sales tactics across the industry, heightened media

coverage and pressure from consumer advocacy groups, the U.K. Financial

Services Authority (FSA) has investigated and raised concerns about the way

some companies have handled complaints relating to the sale of these

insurance policies. In August 2010, the FSA issued a policy statement on

the assessment and remediation of PPI claims which is applicable to the

Corporation’s U.K. consumer businesses and is intended to address con-

cerns among consumers and regulators regarding the handling of PPI com-

plaints across the industry. The policy statement sets standards for the sale

of PPI that apply to current and prior sales, and in the event a company does

not or did not comply with the standards, it is alleged that the insurance was

incorrectly sold, giving the customer rights to remedies. Given the new

regulatory guidance, in 2010, the Corporation had a liability of $630 million

based on its current claims history and an estimate of future claims that have

yet to be asserted against the Corporation. For additional information on PPI,

see Note 14 – Commitments and Contingencies to the Consolidated Financial

Statements – Payment Protection Insurance Claims Matter on page 200.

U.K. Bank Levy

On June 22, 2010, the U.K. government announced that it intended to

introduce an annual bank levy. Beginning in 2011, the bank levy will be payable

62 Bank of America 2010