Bank of America 2010 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

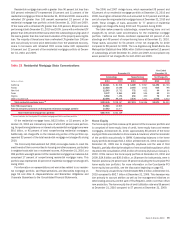

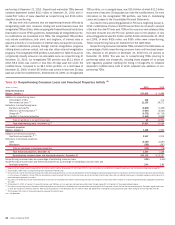

Residential mortgage loans with a greater than 90 percent but less than

100 percent refreshed LTV represented 10 percent and 11 percent of the

residential mortgage portfolio at December 31, 2010 and 2009. Loans with a

refreshed LTV greater than 100 percent represented 23 percent of the

residential mortgage loan portfolio at both December 31, 2010 and 2009.

Of the loans with a refreshed LTV greater than 100 percent, 88 percent were

performing at both December 31, 2010 and 2009. Loans with a refreshed LTV

greater than 100 percent reflect loans where the outstanding carrying value of

the loan is greater than the most recent valuation of the property securing the

loan. The majority of these loans have a refreshed LTV greater than 100 per-

cent due primarily to home price deterioration from the weakened economy.

Loans to borrowers with refreshed FICO scores below 620 represented

14 percent and 12 percent of the residential mortgage portfolio at Decem-

ber 31, 2010 and 2009.

The 2006 and 2007 vintage loans, which represented 38 percent and

42 percent of our residential mortgage portfolio at December 31, 2010 and

2009, have higher refreshed LTVs and accounted for 67 percent and 69 per-

cent of nonperforming residential mortgage loans at December 31, 2010 and

2009. These vintages of loans accounted for 77 percent of residential

mortgage net charge-offs during 2010 and 75 percent during 2009.

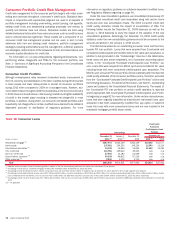

The table below presents outstandings, nonperforming loans and net

charge-offs by certain state concentrations for the residential mortgage

portfolio. California and Florida combined represented 42 percent of out-

standings and 48 percent of nonperforming loans at December 31, 2010.

These states accounted for 54 percent of the net charge-offs for 2010

compared to 58 percent for 2009. The Los Angeles-Long Beach-Santa Ana

Metropolitan Statistical Area (MSA) within California represented 13 percent

of outstandings at both December 31, 2010 and 2009, but comprised only

seven percent of net charge-offs for both 2010 and 2009.

Table 22 Residential Mortgage State Concentrations

(Dollars in millions)

2010 2009 2010 2009 2010 2009

Outstandings Nonperforming Net Charge-offs

December 31

Year Ended

December 31

California

$68,341

$81,508

$6,389

$5,967

$1,392

$1,726

Florida

13,616

15,088

2,054

1,912

604

796

New York

12,545

15,752

772

632

44

66

Texas

9,077

9,865

492

534

52

59

Virginia

6,960

7,496

450

450

72

89

Other U.S./Non-U.S.

82,896

88,438

7,534

7,101

1,506

1,614

Total residential mortgage loans

(1)

$193,435

$218,147

$17,691

$16,596

$3,670

$4,350

Total FHA insured loans

53,946

12,905

Total Countrywide purchased credit-impaired residential mortgage portfolio

10,592

11,077

Total residential mortgage loan portfolio

$257,973

$242,129

(1)

Amount excludes the Countrywide PCI residential mortgage and FHA insured loan portfolios.

Of the residential mortgage loans, $62.5 billion, or 32 percent, at De-

cember 31, 2010 are interest-only loans of which 87 percent were perform-

ing. Nonperforming balances on interest-only residential mortgage loans were

$8.0 billion, or 45 percent of total nonperforming residential mortgages.

Additionally, net charge-offs on the interest-only portion of the portfolio rep-

resented 53 percent of the total residential mortgage net charge-offs during

2010.

The Community Reinvestment Act (CRA) encourages banks to meet the

credit needs of their communities for housing and other purposes, particularly

in neighborhoods with low or moderate incomes. At December 31, 2010, our

CRA portfolio was eight percent of the residential mortgage loan balances but

comprised 17 percent of nonperforming residential mortgage loans. This

portfolio also represented 23 percent of residential mortgage net charge-offs

during 2010.

For information on representations and warranties related to our residen-

tial mortgage portfolio, see Representations and Warranties beginning on

page 56 and Note 9 – Representations and Warranties Obligations and

Corporate Guarantees to the Consolidated Financial Statements.

Home Equity

The home equity portfolio makes up 21 percent of the consumer portfolio and

is comprised of home equity lines of credit, home equity loans and reverse

mortgages. At December 31, 2010, approximately 88 percent of the home

equity portfolio was included in Home Loans & Insurance, while the remainder

of the portfolio was primarily in GWIM. Outstanding balances in the home

equity portfolio decreased $11.1 billion at December 31, 2010 compared to

December 31, 2009 due to charge-offs, paydowns and the sale of First

Republic, partially offset by the adoption of new consolidation guidance, which

resulted in the consolidation of $5.1 billion of home equity loans on January 1,

2010. Of the loans in the home equity portfolio at December 31, 2010 and

2009, $24.8 billion and $26.0 billion, or 18 percent for both periods, were in

first-lien positions (20 percent and 19 percent excluding the Countrywide PCI

home equity loan portfolio). For more information on the Countrywide PCI

home equity loan portfolio, see the discussion beginning on page 82.

Home equity unused lines of credit totaled $80.1 billion at December 31,

2010 compared to $92.7 billion at December 31, 2009. This decrease was

due primarily to account attrition as well as line management initiatives on

deteriorating accounts and the sale of First Republic, which more than offset

new production. The home equity line of credit utilization rate was 59 percent

at December 31, 2010 compared to 57 percent at December 31, 2009.

Bank of America 2010 79