Bank of America 2010 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

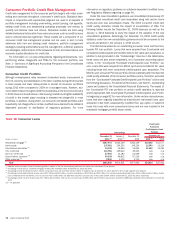

|

|

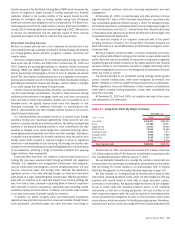

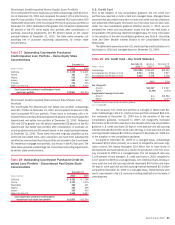

earliest put or redemption date. We had outstanding structured notes of

$61.1 billion and $57.0 billion at December 31, 2010 and 2009.

Substantially all of our senior and subordinated debt obligations contain

no provisions that could trigger a requirement for an early repayment, require

additional collateral support, result in changes to terms, accelerate maturity

or create additional financial obligations upon an adverse change in our credit

ratings, financial ratios, earnings, cash flows or stock price.

We participated in the FDIC’s Temporary Liquidity Guarantee Program (TLGP)

which allowed us to issue senior unsecured debt that the FDIC guaranteed in

return for a fee based on the amount and maturity of the debt. At December 31,

2010, we had $27.5 billion outstanding under the program. We no longer issue

debt under this program and all of our debt issued under TLGP will mature by

June 30, 2012. Under this program, our debt received the highest long-term

ratings from the major credit ratings agencies which resulted in a lower total cost

of issuance than if we had issued non-FDIC guaranteed long-term debt. The

associated FDIC fee for the 2009 issuances was $554 million and is being

amortized into expense over the stated term of the debt.

For additional information on debt funding, see Note 13 – Long-term Debt

to the Consolidated Financial Statements.

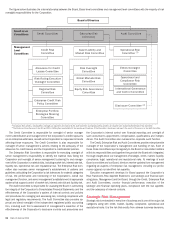

Contingency Planning

We maintain contingency funding plans that outline our potential responses to

liquidity stress events at various levels of severity. These policies and plans

are based on stress scenarios and include potential funding strategies, and

communication and notification procedures that we would implement in the

event we experienced stressed liquidity conditions. We periodically review and

test the contingency funding plans to validate efficacy and assess readiness.

Our U.S. bank subsidiaries can access contingency funding through the

Federal Reserve Discount Window. Certain non-U.S. subsidiaries have access

to central bank facilities in the jurisdictions in which they operate. While we do

not rely on these sources in our liquidity modeling, we maintain the policies,

procedures and governance processes that would enable us to access these

sources if necessary.

Credit Ratings

Our borrowing costs and ability to raise funds are directly impacted by our

credit ratings. In addition, credit ratings may be important to customers or

counterparties when we compete in certain markets and when we seek to

engage in certain transactions including OTC derivatives. Thus, it is our

objective to maintain high-quality credit ratings.

Credit ratings and outlooks are opinions on our creditworthiness and that

of our obligations or securities, including long-term debt, short-term borrow-

ings, preferred stock and other securities, including asset securitizations. Our

credit ratings are subject to ongoing review by the ratings agencies and thus

may change from time to time based on a number of factors, including our own

financial strength, performance, prospects and operations as well as factors

not under our control, such as ratings agency-specific criteria or frameworks

for our industry or certain security types, which are subject to revision from

time to time, and conditions affecting the financial services industry generally.

In light of the recent difficulties in the financial services industry and financial

markets, there can be no assurance that we will maintain our current ratings.

During 2009 and 2010, the ratings agencies took numerous actions,

many of which were negative, to adjust our credit ratings and the outlooks for

those ratings. Currently, Bank of America Corporation’s long-term senior debt

and outlook expressed by the ratings agencies are as follows: A2 (negative) by

Moody’s Investors Services, Inc. (Moody’s), A (negative) by Standard and

Poor’s Ratings Services, a division of The McGraw-Hill Companies, Inc. (S&P),

and A+ (Rating Watch Negative) by Fitch, Inc. (Fitch). Bank of America, N.A.’s

long-term debt and outlook currently are as follows: A+ (negative), Aa3

(negative) and A+ (Rating Watch Negative) by those same three credit ratings

agencies, respectively. The ratings agencies have indicated that, as a sys-

temically important financial institution, our credit ratings currently reflect

their expectation that, if necessary, we would receive significant support from

the U.S. government. All three ratings agencies, however, have indicated they

will reevaluate, and could reduce the uplift they include in our ratings for

government support for reasons arising from financial services regulatory

reform proposals or legislation. In February 2010, S&P affirmed our current

credit ratings but revised the outlook to negative from stable based on its

belief that it is less certain whether the U.S. government would be willing to

provide extraordinary support. On July 27, 2010, Moody’s affirmed our

current ratings but revised the outlook to negative from stable due to its

expectation for lower levels of government support over time as a result of the

passage of the Financial Reform Act. Also, on October 22, 2010, Fitch placed

our credit ratings on Rating Watch Negative from stable outlook due to

proposed rulemaking that could negatively impact its assessment of future

systemic government support. Other factors that influence our credit ratings

include changes to the ratings agencies’ methodologies, the ratings agencies’

assessment of the general operating environment, our relative positions in

the markets in which we compete, reputation, liquidity position, diversity of

funding sources, the level and volatility of earnings, corporate governance and

risk management policies, capital position, capital management practices

and current or future regulatory and legislative initiatives.

A reduction in certain of our credit ratings or the ratings of certain asset-

backed securitizations would likely have a material adverse effect on our

liquidity, access to credit markets, the related cost of funds, our businesses

and on certain trading revenues, particularly in those businesses where

counterparty creditworthiness is critical. Under the terms of certain OTC

derivatives contracts and other trading agreements, in the event of a credit

ratings downgrade, the counterparties to those agreements may require us to

provide additional collateral or to terminate these contracts or agreements.

Such collateral calls or terminations could cause us to sustain losses, impair

our liquidity, or both, by requiring us to provide the counterparties with

additional collateral in the form of cash or highly liquid securities. If Bank

of America Corporation’s or Bank of America, N.A.’s commercial paper or

short-term credit ratings (which currently have the following ratings: P-1 by

Moody’s, A-1 by S&P and F1+ by Fitch) were downgraded by one or more

levels, the potential loss of short-term funding sources such as commercial

paper or repo financing and effect on our incremental cost of funds would be

material. For information regarding the additional collateral and termination

payments that would be required in connection with certain OTC derivative

contracts and other trading agreements as a result of such a credit ratings

downgrade, see Note 4 – Derivatives to the Consolidated Financial State-

ments and Item 1A. Risk Factors of this Annual Report on Form 10-K.

The credit ratings of Merrill Lynch & Co., Inc. from the three major credit

ratings agencies are the same as those of Bank of America Corporation. The

major credit ratings agencies have indicated that the primary drivers of Merrill

Lynch’s credit ratings are Bank of America Corporation’s credit ratings.

74 Bank of America 2010