Bank of America 2010 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

Reform Act and the U.S. banking regulators’ subsequent Notice of Proposed

Rulemaking published by the Federal Reserve on December 14, 2010 pro-

pose however that the current three-year transitional floors under Basel II be

replaced with a permanent risk based capital floor as defined under Basel I.

On December 16, 2010, U.S. regulators issued a Notice of Proposed

Rulemaking on the Risk-Based Capital Guidelines for Market Risk (Market

Risk Rules), reflecting partial adoption of the Basel Committee’s July 2009

consultative document on the topic. We anticipate U.S. regulators will adopt

the Market Risk Rules in mid-2011. This change is expected to significantly

increase the capital requirements for our trading assets and liabilities,

including derivatives exposures which meet the definition established by

the regulatory agencies. We continue to evaluate the capital impact of the

proposed rules and currently anticipate being fully compliant with any final

rules by the projected implementation date of year-end 2011.

On December 16, 2010, the Basel Committee issued “Basel III: A global

regulatory framework for more resilient banks and banking systems” (Basel

III), proposing a January 2013 implementation date for Basel III. If imple-

mented by U.S. regulators as proposed, Basel III could significantly increase

our capital requirements. Basel III and the Financial Reform Act propose the

disqualification of trust preferred securities from Tier 1 capital, with the

Financial Reform Act proposing the disqualification be phased in from

2013 to 2015. Basel III also proposes the deduction of certain assets from

capital (deferred tax assets, MSRs, investments in financial firms and pen-

sion assets, among others, within prescribed limitations), the inclusion of

other comprehensive income in capital, increased capital for counterparty

credit risk, and new minimum capital and buffer requirements. The phase-in

period for the capital deductions is proposed to occur in 20 percent incre-

ments from 2014 through 2018 with full implementation by December 31,

2018. The increase in capital requirements for counterparty credit risk is

proposed to be effective January 2013. The phase-in period for the new

minimum capital requirements and related buffers is proposed to occur

between 2013 and 2019. U.S. regulators are expected to begin the final

rulemaking processes for Basel III in early 2011 and have indicated a goal to

adopt final rules by year-end 2011 or early 2012. For additional information on

our MSRs, refer to Note 25 – Mortgage Servicing Rights to the Consolidated

Financial Statements. For additional information on deferred tax assets, refer

to Note 21 – Income Taxes to the Consolidated Financial Statements.

If Basel III is implemented in the U.S. consistent with Basel Committee

rules, beginning in January 2013, we would be required to maintain minimum

capital ratio requirements of 6.0 percent for Tier 1 capital and 8.0 percent for

Total capital. Basel III also includes a proposed minimum requirement for

common equity Tier 1 capital of 3.5 percent beginning in 2013 which would

increase to 4.5 percent in 2015. Basel III also includes three capital buffers

which would be phased in over time and impact all three capital ratios. These

buffers include a capital conservation buffer that would start at 0.63 percent

in 2016 and increase to 2.5 percent in 2019. Thus, the minimum capital ratio

requirements including the capital conservation buffer in 2019 would be

7.0 percent for common equity Tier 1 capital, 8.5 percent for Tier 1 capital and

10.5 percent for Total capital. If ratios fall below the minimum requirement

plus the capital conservation buffer, such as 10.5 percent for Total capital, an

institution would be required to restrict dividends, share repurchases and

discretionary bonuses. Additionally, Basel III also includes a countercyclical

buffer of up to 2.5 percent that regulators could require in periods of excess

credit growth. The countercyclical buffer is to be comprised of loss-absorbing

capital, such as common equity, and is meant to retain additional capital

during periods of excess credit growth providing incremental protection in the

event of a material market downturn. The ratios presented above do not

include the third buffer requirement for systemically important financial

institutions, which the Basel Committee continues to assess and has not

yet quantified. The countercyclical and systemic buffers are scheduled to be

phased in from 2013 through 2019. U.S. regulators are expected to begin the

rulemaking processes for Basel III in early 2011 and have indicated a goal to

adopt final rules by the end of 2011 or early 2012.

These regulatory changes also require approval by the agencies of ana-

lytical models used as part of our capital measurement and assessment,

especially in the case of more complex models. If these more complex models

are not approved, it could require financial institutions to hold additional

capital, which in some cases could be significant.

We expect to maintain a Tier 1 common capital ratio in excess of eight per-

cent as the regulatory rule changes are implemented without needing to raise

new equity capital. We have made the implementation and mitigation of these

regulatory changes a strategic priority. We also note there remains significant

uncertainty on the final impacts as the U.S. has issued final rules only for

Basel II and a Notice of Proposal Rulemaking for the Market Risk Rules at this

time. Impacts may change as the U.S. finalizes rules and the regulatory

agencies interpret the final rules for Basel III during the implementation

process.

Bank of America, N.A. and FIA Card Services, N.A.

Regulatory Capital

The table below presents regulatory capital information for Bank of America

N.A. and FIA Card Services, N.A. at December 31, 2010 and 2009. The

goodwill impairment charges recognized in 2010 did not impact the regulatory

capital ratios.

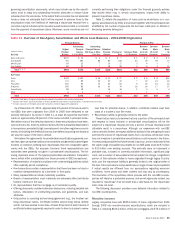

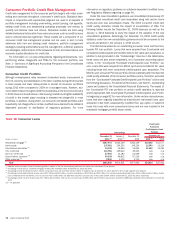

Table 14 Bank of America, N.A. and FIA Card Services, N.A. Regulatory Capital

(Dollars in millions)

Ratio Amount Ratio Amount

2010 2009

December 31

Tier 1

Bank of America, N.A.

10.78% $114,345

10.30% $111,916

FIA Card Services, N.A.

15.30 25,589

15.21 28,831

Total

Bank of America, N.A.

14.26 151,255

13.76 149,528

FIA Card Services, N.A.

16.94 28,343

17.01 32,244

Tier 1 leverage

Bank of America, N.A.

7.83 114,345

7.38 111,916

FIA Card Services, N.A.

13.21 25,589

23.09 28,831

The Bank of America, N.A. Tier 1 and Total capital ratio increased 48 bps to

10.78 percent and 50 bps to 14.26 percent at December 31, 2010 compared

to December 31, 2009. The increase in the ratios was driven by $11.1 billion

in earnings generated in 2010 combined with a $26.4 billion decline in risk-

weighted assets. The Tier 1 leverage ratio increased 45 bps to 7.83 percent

benefiting from the improvement in Tier 1 capital combined with a $56.0 billion

Bank of America 2010 69