Bank of America 2010 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

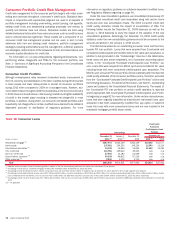

Credit Risk Management

Credit quality continued to show improvement during 2010; although, net

charge-offs, and nonperforming loans, leases and foreclosed properties re-

mained elevated. Signs of economic stability and our proactive credit risk

management initiatives positively impacted the credit portfolio as charge-offs

and delinquencies continued to improve across almost all portfolios along with

risk rating improvements in the commercial portfolio. Global and national

economic uncertainty, regulatory initiatives and reform, however, continued

to weigh on the credit portfolios through December 31, 2010. For more

information, see 2010 Economic and Business Environment on page 29. Credit

metrics were also impacted by loans added to the balance sheet on January 1,

2010 in connection with the adoption of new consolidation guidance.

Credit risk is the risk of loss arising from the inability of a borrower or

counterparty to meet its obligations. Credit risk can also arise from opera-

tional failures that result in an erroneous advance, commitment or investment

of funds. We define the credit exposure to a borrower or counterparty as the

loss potential arising from all product classifications including loans and

leases, deposit overdrafts, derivatives, assets held-for-sale and unfunded

lending commitments which include loan commitments, letters of credit and

financial guarantees. Derivative positions are recorded at fair value and

assets held-for-sale are recorded at fair value or the lower of cost or fair

value. Certain loans and unfunded commitments are accounted for under the

fair value option. Credit risk for these categories of assets is not accounted

for as part of the allowance for credit losses but as part of the fair value

adjustments recorded in earnings. For derivative positions, our credit risk is

measured as the net replacement cost in the event the counterparties with

contracts in which we are in a gain position fail to perform under the terms of

those contracts. We use the current mark-to-market value to represent credit

exposure without giving consideration to future mark-to-market changes. The

credit risk amounts take into consideration the effects of legally enforceable

master netting agreements and cash collateral. Our consumer and commer-

cial credit extension and review procedures take into account funded and

unfunded credit exposures. For additional information on derivative and credit

extension commitments, see Note 4 – Derivatives and Note 14 – Commit-

ments and Contingencies to the Consolidated Financial Statements.

We manage credit risk based on the risk profile of the borrower or

counterparty, repayment sources, the nature of underlying collateral, and

other support given current events, conditions and expectations. We classify

our portfolios as either consumer or commercial and monitor credit risk in

each as discussed below.

We proactively refine our underwriting and credit management practices,

as well as credit standards, to meet the changing economic environment. To

actively mitigate losses and enhance customer support in our consumer

businesses, we have expanded collections, loan modification and customer

assistance infrastructures. We also have implemented a number of actions to

mitigate losses in the commercial businesses including increasing the fre-

quency and intensity of portfolio monitoring, hedging activity and our practice

of transferring management of deteriorating commercial exposures to inde-

pendent special asset officers as credits approach criticized levels.

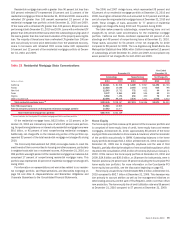

Since January 2008, and through 2010, Bank of America and Countrywide

have completed nearly 775,000 loan modifications with customers. During

2010, we completed nearly 285,000 customer loan modifications with a total

unpaid principal balance of approximately $65.7 billion, which included

109,000 customers who converted from trial period to permanent modifica-

tions under the government’s MHA program. Of the loan modifications

completed in 2010, in terms of both the volume of modifications and the

unpaid principal balance associated with the underlying loans, most were in

the portfolio serviced for investors and were not on our balance sheet. The

most common types of modifications during the year include a combination of

rate reduction and capitalization of past due amounts which represent 68 per-

cent of the volume of modifications completed in 2010, while principal

forbearance represented 15 percent and capitalization of past due amounts

represented nine percent. We also provide rate reductions, rate and payment

extensions, principal forgiveness and other actions. These modification types

are generally considered troubled debt restructurings (TDRs). For more infor-

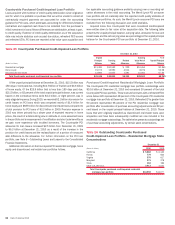

mation on TDRs and portfolio impacts, see Nonperforming Consumer Loans

and Foreclosed Properties Activity beginning on page 85 and Note 6 – Out-

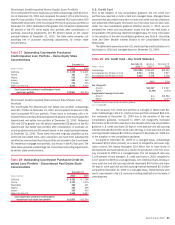

standing Loans and Leases to the Consolidated Financial Statements.

On October 1, 2010, we voluntarily stopped taking residential mortgage

foreclosure proceedings to judgment in judicial states. On October 8, 2010,

we stopped foreclosure sales in all states in order to complete an assess-

ment of the related business processes. As a result of that assessment, we

identified and began implementing process and control enhancements and

we intend to monitor ongoing quality results of each process. After these

enhancements were put in place, we resumed foreclosure sales in most non-

judicial states during the fourth quarter of 2010, and expect sales to resume

in the remaining non-judicial states in the first quarter of 2011. The process of

preparing affidavits in pending proceedings in judicial states is expected to

continue into the first quarter of 2011 and could result in prolonged adversary

proceedings that delay certain foreclosure sales. We took these precaution-

ary steps in order to ensure our processes for handling foreclosures include

the appropriate controls and quality assurance. These initiatives further

support our credit risk management and mitigation efforts. For more infor-

mation, see Recent Events beginning on page 37.

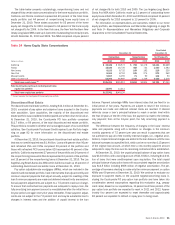

Certain European countries, including Greece, Ireland, Italy, Portugal and

Spain, continue to experience varying degrees of financial stress. Risks and

ongoing concerns about the debt crisis in Europe could result in a disruption of

the financial markets which could have a detrimental impact on the global

economic recovery, including the impact of non-sovereign debt in these

countries. For more information on our direct sovereign and non-sovereign

exposures in these countries, see Non-U.S. Portfolio beginning on page 98.

The Financial Accounting Standards Board (FASB) issued new disclosure

guidance, effective on a prospective basis for the Corporation’s 2010 year-

end reporting, that addresses disclosure of loans and other financing receiv-

ables and the related allowance. The new disclosure guidance defines a

portfolio segment as the level at which an entity develops and documents a

systematic methodology to determine the allowance for credit losses, and a

class of financing receivables as the level of disaggregation of portfolio

segments based on the initial measurement attribute, risk characteristics

and methods for assessing risk. The Corporation’s portfolio segments are

home loans, credit card and other consumer, and commercial. The classes

within the home loans portfolio segment are residential mortgage, home

equity and discontinued real estate. The classes within the credit card and

other consumer portfolio segment are U.S. credit card, non-U.S. credit card,

direct/indirect consumer and other consumer. The classes within the com-

mercial portfolio segment are U.S. commercial, commercial real estate,

commercial lease financing, non-U.S. commercial and U.S. small business

commercial. Under this new disclosure guidance, the allowance is presented

by portfolio segment.

Bank of America 2010 75