Bank of America 2010 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2010 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

Consumer Portfolio Credit Risk Management

Credit risk management for the consumer portfolio begins with initial under-

writing and continues throughout a borrower’s credit cycle. Statistical tech-

niques in conjunction with experiential judgment are used in all aspects of

portfolio management including underwriting, product pricing, risk appetite,

setting credit limits and establishing operating processes and metrics to

quantify and balance risks and returns. Statistical models are built using

detailed behavioral information from external sources such as credit bureaus

and/or internal historical experience. These models are a component of our

consumer credit risk management process and are used, in part, to help

determine both new and existing credit decisions, portfolio management

strategies including authorizations and line management, collection practices

and strategies, determination of the allowance for loan and lease losses, and

economic capital allocations for credit risk.

For information on our accounting policies regarding delinquencies, non-

performing status, charge-offs and TDRs for the consumer portfolio, see

Note 1 – Summary of Significant Accounting Principles to the Consolidated

Financial Statements.

Consumer Credit Portfolio

Although unemployment rates remained at elevated levels, improvement in

the U.S. economy and stabilization in the labor markets during 2010 resulted

in lower losses and lower delinquencies in almost all consumer portfolios

during 2010 when compared to 2009 on a managed basis. However, eco-

nomic deterioration throughout 2009 and weakness in the economic recovery

in 2010 drove continued stress in the housing markets and tighter availability

of credit in the market place resulting in elevated net charge-offs in most

portfolios. In addition, during 2010, our consumer real estate portfolios were

impacted by net charge-offs on certain modified loans deemed to be collateral

dependent pursuant to clarification of regulatory guidance. For more

information on regulatory guidance on collateral dependent modified loans,

see Regulatory Matters beginning on page 60.

Under the new consolidation guidance, we consolidated all previously off-

balance sheet securitized credit card receivables along with certain home

equity and auto loan securitization trusts. The 2010 consumer credit card

credit quality statistics include the impact of consolidation of VIEs. The

following tables include the December 31, 2009 balances as well as the

January 1, 2010 balances to show the impact of the adoption of the new

consolidation guidance. Accordingly, the December 31, 2010 credit quality

statistics under the new consolidation guidance should be compared to the

amounts presented in the January 1, 2010 column.

The table below presents our outstanding consumer loans and the Coun-

trywide PCI loan portfolio. Loans that were acquired from Countrywide and

considered credit-impaired were written down to fair value upon acquisition. In

addition to being included in the “Outstandings” columns in the table below,

these loans are also shown separately, net of purchase accounting adjust-

ments, in the “Countrywide Purchased Credit-impaired Loan Portfolio” col-

umn. Loans that were acquired from Merrill Lynch were recorded at fair value

including those that were considered credit-impaired upon acquisition. The

Merrill Lynch consumer PCI loan portfolio did not materially alter the reported

credit quality statistics of the consumer portfolios and is, therefore, excluded

from the “Countrywide Purchased Credit-impaired Loan Portfolio” column and

the following discussion. For additional information, see Note 6 – Outstanding

Loans and Leases to the Consolidated Financial Statements. The impact of

the Countrywide PCI loan portfolio on certain credit statistics is reported

where appropriate. See Countrywide Purchased Credit-impaired Loan Portfo-

lio beginning on page 82 for more information. Under certain circumstances,

loans that were originally classified as discontinued real estate loans upon

acquisition have been subsequently modified from pay option or subprime

loans into loans with more conventional terms and are now included in the

residential mortgage portfolio shown below.

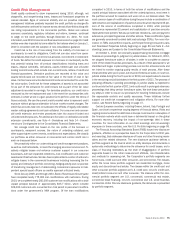

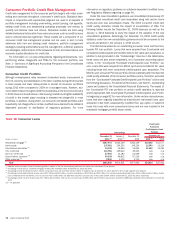

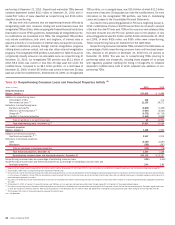

Table 18 Consumer Loans

(Dollars in millions)

December 31

2010

(1)

January 1

2010

(1)

December 31

2009 2010

(1)

2009

December 31

Outstandings

Countrywide

Purchased

Credit-impaired Loan

Portfolio

Residential mortgage

(2)

$257,973

$242,129 $242,129

$10,592

$11,077

Home equity

137,981

154,202 149,126

12,590

13,214

Discontinued real estate

(3)

13,108

14,854 14,854

11,652

13,250

U.S. credit card

113,785

129,642 49,453

n/a

n/a

Non-U.S. credit card

27,465

31,182 21,656

n/a

n/a

Direct/Indirect consumer

(4)

90,308

99,812 97,236

n/a

n/a

Other consumer

(5)

2,830

3,110 3,110

n/a

n/a

Total

$643,450

$674,931 $577,564

$34,834

$37,541

(1)

Balances reflect the impact of new consolidation guidance. Adoption of the new consolidation guidance did not impact the Countrywide PCI loan portfolio.

(2)

Outstandings include non-U.S. residential mortgages of $90 million and $552 million at December 31, 2010 and 2009.

(3)

Outstandings include $11.8 billion and $13.4 billion of pay option loans and $1.3 billion and $1.5 billion of subprime loans at December 31, 2010 and 2009. We no longer originate these products.

(4)

Outstandings include dealer financial services loans of $42.9 billion and $41.6 billion, consumer lending loans of $12.9 billion and $19.7 billion, U.S. securities-based lending margin loans of $16.6 billion and $12.9 billion, student

loans of $6.8 billion and $10.8 billion, non-U.S. consumer loans of $8.0 billion and $8.0 billion and other consumer loans of $3.1 billion and $4.2 billion at December 31, 2010 and 2009, respectively.

(5)

Outstandings include consumer finance loans of $1.9 billion and $2.3 billion, other non-U.S. consumer loans of $803 million and $709 million and consumer overdrafts of $88 million and $144 million at December 31, 2010 and

2009.

n/a = not applicable

76 Bank of America 2010